Download

1 / 58

580 likes | 920 Vues

Product Costing Systems. JOIN KHALID AZIZ. ECONOMICS OF ICMAP, ICAP, MA-ECONOMICS, B.COM. FINANCIAL ACCOUNTING OF ICMAP STAGE 1,3,4 ICAP MODULE B, B.COM, BBA, MBA & PIPFA. COST ACCOUNTING OF ICMAP STAGE 2,3 ICAP MODULE D, BBA, MBA & PIPFA. CONTACT: 0322-3385752 0312-2302870

E N D

JOIN KHALID AZIZ • ECONOMICS OF ICMAP, ICAP, MA-ECONOMICS, B.COM. • FINANCIAL ACCOUNTING OF ICMAP STAGE 1,3,4 ICAP MODULE B, B.COM, BBA, MBA & PIPFA. • COST ACCOUNTING OF ICMAP STAGE 2,3 ICAP MODULE D, BBA, MBA & PIPFA. • CONTACT: • 0322-3385752 • 0312-2302870 • R-1173,ALNOOR SOCIETY, BLOCK 19,F.B.AREA, KARACHI, PAKISTAN.

JOIN KHALID AZIZ • FRESH CLASSES • ICMAP STAGE 3 • COST ACCOUNTING PERFORMANCE APPRAISAL • 22nd FEBRUARY 2010 • INDIVIDUAL & GROUPS

JOIN KHALID AZIZ • FRESH CLASSES • ICMAP STAGE 3 • FINANCIAL ACCOUNTING • 22nd FEBRUARY 2010 • INDIVIDUAL & GROUPS

JOIN KHALID AZIZ • FRESH CLASSES • ICMAP STAGE 2 • COST ACCOUNTING • 22nd FEBRUARY 2010 • INDIVIDUAL & GROUPS

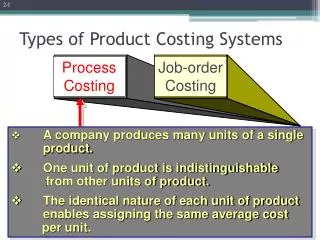

The two most common systems of product costing are: • Job-order costing and • Process costing

Job-Order Costing • Job-order costing (or simply job costing) allocates costs to products that are readily identified by individual units or batches, each of which requires varying degrees of attention and skill.

Process Costing • Process costing allocates costs to products by averaging costs over large numbers of nearly identical products.

Job-Order-Costing System • The basic records maintained in a job-costing system include: • Job-cost record, • Materials requisitions, and • Labor time tickets.

Job-Cost Record • The centerpiece of a job-costing system is the job-cost record (also called a job-cost sheet or job order). • All costs for a particular product, service, or batch of products are recorded on the job-cost record.

Materials Requisitions • Materials requisitions are records of materials used in particular jobs and are summarized in the job-cost record.

Labour Time Tickets • Labour time tickets (or time cards) record the time a particular direct labourer spends on each job and are summarized in the job-cost record.

Typical Journal Entries for a Job-Costing System • Transaction 1: Direct-Materials Inventory 1,900,000 Accounts Payable 1,900,000 To record purchase of materials to be used directly in the manufacturing process.

Typical Journal Entries for a Job-Costing System • Transaction 2: WIP Inventory 1,890,000 Direct-Materials Inventory 1,890,000 To record materials requisitioned into the manufacturing process.

Typical Journal Entries for a Job-Costing System • Transaction 3: WIP Inventory 390,000 Accrued Payroll 390,000 To record direct-labor cost incurred in the manufacturing process.

Typical Journal Entries for a Job-Costing System • Transaction 4a: Factory Depart. Overhead Control 392,000 Cash, Accounts Payable, and various other balance sheet accounts 392,000 To record factory overhead incurred. (Accounting for factory overhead will be covered later in greater detail.)

Typical Journal Entries for a Job-Costing System • Transaction 4b: WIP Inventory 375,000 Factory Depart. Overhead Control 375,000 To record factory overhead applied, Rs95,000 + Rs280,000 = Rs375,000. (Accounting for factory overhead will be covered later in greater detail.)

Typical Journal Entries for a Job-Costing System • Transaction 5: Finished Goods Inventory 2,500,000 WIP Inventory 2,500,000 To transfer cost of goods completed from work-in-process inventory to finished goods inventory.

Typical Journal Entries for a Job-Costing System • Transaction 6a: Accounts Receivable 4,000,000 Sales 4,000,000 To record sales of merchandise on account.

Typical Journal Entries for a Job-Costing System • Transaction 6b: Cost of Goods Sold 2,480,000 Finished Goods Inventory 2,480,000 To record (transfer) the cost of the merchandise sold from finished goods inventory to cost of goods sold (expense).

How Factory Overhead is Applied to Products • Managers need to know product costs in order to make ongoing decisions such as which products to emphasize or de-emphasize and the pricing of products.

How Factory Overhead is Applied to Products • Ideally, all costs, including overhead, are known when these decisions must be made. • Unfortunately, actual overhead costs are not available when managers need them. For this reason, budgeted overhead rates are used to apply overhead to jobs as they are completed.

Budgeted OverheadApplication Rates • The following steps summarize how to account for factory overhead: 1. Select one or more cost drivers to serve as a base for applying overhead costs. 2. Prepare a factory-overhead budget for the planning period, ordinarily a year. The two key items are (1) budgeted overhead and (2) budgeted volume of the cost driver.

Budgeted OverheadApplication Rates 3. Compute the budgeted factory-overhead rate(s) by dividing the budgeted total overhead for each cost pool by the budgeted cost-driver level. 4. Obtain actual cost-driver data (such as machine-hours) as jobs are produced. 5. Apply the budgeted overhead to the jobs by multiplying the budgeted rate(s) times the actual cost-driver data.

Budgeted OverheadApplication Rates 6. At the end of the year, account for any differences between the amount of overhead actually incurred and overhead applied to products.

Compute BudgetedFactory-Overhead Rate • A budgeted overhead rate is computed as follows: budgeted overhead application rate = total budgeted factory overhead total budgeted amount of cost driver

Choice of Cost Drivers • No one cost driver is right for all situations. • The accountant’s goal is to find the driver that best links cause and effect.

Choice of Cost Drivers • Look for the activity that causes the most overhead cost and then keep track of that activity. • For example, if use of machines causes the most overhead with depreciation and repairs, then keep track of machine-hours used for each job.

Normalized Overhead Rates • A normalized overhead rate is when an annual average overhead rate is used consistently throughout the year for product costing, without altering it from day to day and from month to month. The resultant “normal” product costs include an average or normalized chunk of overhead.

Normalized Overhead Rates • During the year and at year end, the actual overhead amount incurred will rarely equal the amount applied. • The variance between incurred and applied cost is due to many factors such as:

Normalized Overhead Rates • A different level of volume than the level used as a denominator in calculating the budgeted overhead rate, • Poor forecasting, • Inefficient use of overhead items, • Price changes in individual items, • Erratic behavior of individual overhead items, and • Calendar variations.

Normalized Overhead Rates • Thus, an annual rate is budgeted and used regardless of the month-to-month peculiarities of specific overhead costs. • Because overhead cannot be traced to physical products, overhead is applied on an average or normalized basis to get representative or normal inventory valuations.

Normal Costing System • Hence, we shall label the system a normal costing system: The cost system in which overhead is applied on an average or normalized basis, in order to get representative or normal inventory valuations.

Overapplied Overhead • When the amount of overhead applied to products exceeds the amount of actual overhead incurred by departments, the difference is called overapplied overhead.

Underapplied Overhead • When the amount of overhead applied to products is less than the amount of actual overhead incurred by departments, the difference is called underapplied overhead.

Disposition of Underapplied or Overapplied Overhead • At year end, the difference between actual overhead incurred and overhead applied is disposed of through either: • a write-off or • proration.

Disposition of Underapplied or Overapplied Overhead • Illustration using transactions journalized earlier: Transaction 4a. Factory overhead incurred Rs392,000 4b. Factory overhead applied 375,000 Underapplied factory overhead Rs 17,000

Immediate Write-Off • The theory underlying direct write-off is that most of the goods worked on have been sold, and a more elaborate method of disposition is not worth the extra trouble. • The immediate write-off eliminates the Rs17,000 difference with a simple journal entry as follows:

Immediate Write-Off • Transaction 7: Cost of Goods Sold 17,000 Factory Depart. Overhead Control 17,000 To close ending underapplied overhead directly to Cost of Goods Sold.

Proration Among Inventories • To prorate underapplied overhead or overapplied overhead means to assign it in proportion to the sizes of the ending account balances in Work-in-Process Inventory, Finished Goods Inventory, and Cost of Goods Sold.

Proration Among Inventories • Underapplied overhead is then added to the ending balances and overapplied overhead is subtracted from the ending balances.

Proration Among Inventories • Theoretically, if the objective is to obtain as accurate a cost allocation as possible, all the overhead costs of the individual jobs worked on should be recomputed, using the actual, rather than the budgeted, rates.

Proration Among Inventories • This approach is rarely feasible, so a practical attack is to prorate on the basis of the ending balances in each of three accounts, WIP, Finished Goods, and Cost of Goods Sold. • In our illustration, the proration is calculated as follows:

Proration Among Inventories Unadjusted Balance Proration of End of 19X2 Underapplied Overhead WIP Rs 155,000 155/2,667 x Rs17,000 Finished Goods 32,000 32/2,667 x Rs17,000 Cost of Goods Sold 2,480,000 2,480/2,667 x Rs17,000 Rs2,667,000

Proration Among Inventories Proration of Adjusted Underapplied Balance Overhead End of 19X2 WIP = Rs 988 Rs 155,988 Finished Goods = 204 32,204 Cost of Goods Sold = 15,808 2,495,808 Rs17,000 Rs2,684,000

Proration Among Inventories • The journal entry for the proration follows: WIP 988 Finished Goods 204 Cost of Goods Sold 15,808 Factory Depart. Overhead Control 17,000 To prorate ending underapplied overhead among three accounts.

Activity-Based Costing in aJob Order Environment • As is the case with any business, understanding profitability means understanding the cost structure of the entire business. • One of the key advantages of an ABC system is its focus on understanding how work (activity) is related to the consumption of resources (costs).

Activity-Based Costing in aJob Order Environment • In developing an ABC system, begin by focusing on the most critical (core) processes across the value chain. • After the initial system is in place, the remaining phases of the value chain can be added.

Activity-Based Costing in aJob-Order Environment • To understand product-line profitability, the key activities must be identified. • Once the key activities have been identified, appropriate cost drivers are used to allocate activity costs to the assembly lines that produced the product lines.

Product Costing in Service and Nonprofit Organizations • The job-costing approach is used in nonmanufacturing situations too. • The focus shifts from the costs of products to the costs of services.