Download

1 / 10

100 likes | 293 Vues

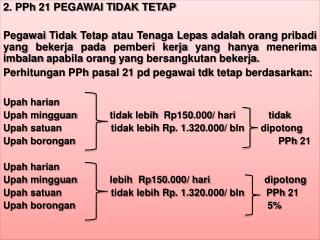

Segaf , SE.MSc. PPh 21. Preface. PPh 21 merupakan penghitungan & pemotongan pajak yang dilakukan oleh pemberi pekerjaan dan orang pribadi penerima pekerjaan. Subyek & Obyek PPh 21. Klasifikasi Pegawai. Definisi Pegawai Tetap. Definisi Pegawai Tidak Tetap. Definisi Bukan Pegawai.

E N D

Segaf, SE.MSc. PPh 21

Preface PPh 21 merupakanpenghitungan & pemotonganpajak yang dilakukanolehpemberipekerjaandanorangpribadipenerimapekerjaan.

PenjabaranobyekPPh 21 Source: Per-31/PJ./2009 Pasal 1

BiayaJabatanatauBiayaPensiun • Penghasilanpegawaitetap/pensiunanbulanandipotongpajakdaripenghasilanbrutodikurangiBiayaJabatan/ BiayaPensiun • BiayaJabatan • 5% x penghasilanBruto tau maksimal Rp.500.000 perbulanatauRp. 6.000.000 per tahun • BiayaPensiun • 5% x penghasilanBruto tau maksimalRp.200.000 perbulanatauRp. 2.400.000 per tahun