Download

1 / 82

820 likes | 834 Vues

Chapter 12 Consumption, Real GDP, and the Multiplier. Introduction. Since the early 2000s, planned real investment spending has increased in most of the world’s nations.

E N D

Introduction Since the early 2000s, planned real investment spending has increased in most of the world’s nations. As a percentage of global real GDP, however, planned real investment spending in the world’s developed countries has declined. Yet, it has been rising in emerging-economy nations. These are countries transitioning to a developed status. How do changes in planned real investment spending affect a country’s real GDP? Reading Chapter 12 will help you answer this question.

Learning Objectives • Distinguish between saving and savings and explain how consumption and saving are related • Explain the key determinants of consumption and saving in the Keynesian model • Identify the primary determinants of planned investment

Learning Objectives (cont'd) • Describe how equilibrium real GDP is established in the Keynesian model • Evaluate why autonomous changes in total planned expenditures have a multiplier effect on equilibrium real GDP • Understand the relationship between total planned expenditures and the aggregate demand curve

Chapter Outline • Some Simplifying Assumptions in a Keynesian Model • Determinants of Planned Consumption and Planned Saving • Determinants of Investment • Determining Equilibrium Real GDP

Chapter Outline (cont'd) • Keynesian Equilibrium with Government and the Foreign Sector Added • The Multiplier • How a Change in Real Autonomous Spending Affects Real GDP When the Price Level Can Change • The Relationship Between Aggregate Demand and the C + I + G + X Curve

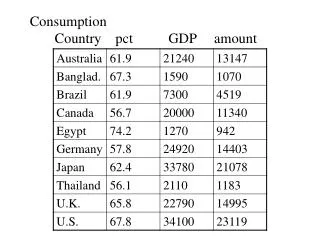

Did You Know That ... • The share of real GDP allocated to real consumption spending is: • 66 percent in Germany • 60 percent in the United Kingdom • 70 percent in the United States • Less than 41 percent in China? • In this chapter, you will learn how an understanding of households’ real saving and real consumption spending can help you evaluate fluctuations in a national’s real GDP.

Some Simplifying Assumptions in a Keynesian Model • To simplify the income determination model, let’s assume: • Businesses pay no indirect taxes (sales tax) • Businesses distribute all profits to shareholders • There is no depreciation • The economy is closed; no foreign trade

Some Simplifying Assumptions in a Keynesian Model (cont'd) • Real Disposable Income • Real GDP minus net taxes, or after-tax real income • Consumption • Spending on new goods and services out of a household’s current income • Whatever is not consumed is saved • Consumption includes such things as buying food and going to a concert

Some Simplifying Assumptions in a Keynesian Model (cont'd) • Saving • The act of not consuming all of one’s current income • Whatever is not consumed out of spendable income is, by definition, saved • Saving is an action measured over time (a flow) • Savings are a stock, an accumulation resulting from the act of saving in the past

Some Simplifying Assumptions in a Keynesian Model (cont'd) • Consumption Goods • Goods bought by households to use up, such as food and movies

Some Simplifying Assumptions in a Keynesian Model (cont'd) • Accounting identity: Consumption + saving disposable income Saving disposable income – consumption

Some Simplifying Assumptions in a Keynesian Model (cont'd) • Investment • Spending by businesses on things such as machines and buildings, which can be used to produce goods and services in the future • The investment part of real GDP is the portion that will be used in the process of producing goods in the future

Some Simplifying Assumptions in a Keynesian Model (cont'd) • Capital Goods • Producer durables; nonconsumable goods that firms use to make other goods

Determinants of Planned Consumption and Planned Saving • In the classical model, the supply of saving was determined by the rate of interest • The higher the rate, the more people wanted to save, and the less they wanted to consume

Determinants of Planned Consumption and Planned Saving (cont'd) • Keynes argued that: • The interest rate is not the most important factor in saving and consumption decisions • Rather, real saving and consumption decisions depend primarily on a household’s real disposable income. • Furthermore, a person’s anticipation about future flows of income influences how much of current income is allocated to consumption and how much is allocated to saving.

Determinants of Planned Consumption and Planned Saving (cont'd) • The Life-Cycle Theory of Consumption • The most realistic and detailed theory of consumption, often called the life-cycle theory of consumption, considers how a person varies saving and consumption as income ebbs and flows throughout an entire life span. • This theory predicts that when an individual anticipates a higher income in the future, he or she will tend to consume more and save less in the current period than would have been the case otherwise.

Determinants of Planned Consumption and Planned Saving (cont'd) • The Permanent Income Hypothesis • A related theory, called the permanent income hypothesis, suggests that the income level that matters for a person’s decisions about current consumption and saving is permanent income, or expected average lifetime income. • Thus, if a person’s flow of income temporarily rises without an increase in average lifetime income, the person responds by saving more and leaving consumption unchanged.

Determinants of Planned Consumption and Planned Saving (cont'd) • The Keynesian Theory of Consumption and Saving • Keynes argued that real consumption and saving decisions depend primarily on a household’s current real disposable income.

Determinants of Planned Consumption and Planned Saving (cont'd) • Consumption Function • The relationship between amount consumed and disposable income • A consumption function tells us how much people plan to consume at various levels of disposable income

Determinants of Planned Consumption and Planned Saving (cont'd) • Dissaving • Negative saving; a situation in which spending exceeds income • Dissaving can occur when a household is able to borrow or use up existing assets

Table 12-1 Real Consumption and Saving Schedules: A Hypothetical Case

Determinants of Planned Consumption and Planned Saving (cont'd) • 45-Degree Reference Line • The line along which planned real expenditures equal real GDP per year

Determinants of Planned Consumption and Planned Saving (cont'd) • Autonomous Consumption • The part of consumption that is independent of the level of disposable income • Changes in autonomous consumption shift the consumption function

Determinants of Planned Consumption and Planned Saving (cont'd) Real consumption APC = Real disposable income • Average Propensity to Consume (APC) • Real consumption divided by real disposable income • The proportion of total disposable income that is consumed

Determinants of Planned Consumption and Planned Saving (cont'd) Real saving APS = Real disposable income • Average Propensity to Save (APS) • Real saving divided by real disposable income (DI) • Saved proportion of real DI

Determinants of Planned Consumption and Planned Saving (cont'd) Change in real consumption MPC = Change in real disposable income • Marginal Propensity to Consume (MPC) • The ratio of the change in real consumption to the change in real disposable income

Determinants of Planned Consumption and Planned Saving (cont'd) Change in real saving MPS = Change in real disposable income • Marginal Propensity to Save (MPS) • The ratio of the change in saving to the change in disposable income

Determinants of Planned Consumption and Planned Saving (cont'd) $49,200 APC = = .911 $54,000 • Example • Income = $54,000 • C= $49,200 • S = $4,800 • What is the APC?

Determinants of Planned Consumption and Planned Saving (cont'd) $54,000 APC = = .90 $60,000 • Example • Income increases by $6,000 to $60,000 • C = $54,000 • S = $6,000 • What is the APC?

Determinants of Planned Consumption and Planned Saving (cont'd) • Some relationships APC + APS 1 MPC + MPS 1

Determinants of Planned Consumption and Planned Saving (cont'd) • Causes of shifts in the consumption function • A change besides real disposable income will cause the consumption function to shift • Non-income determinants of consumption • Population • Wealth

Determinants of Planned Consumption and Planned Saving (cont'd) • Net wealth • The stock of assets owned by a person, household, firm or nation (net of any debts owed) • For a household, wealth can consist of a house, cars, personal belongings, stocks, bonds, bank accounts, and cash (minus any debts owed)

Example: Lower Household Wealth and Subdued Growth in Consumption • Between 2007 and 2009, there was a substantial decline in two key components of real household wealth. • Inflation-adjusted wealth in housing fell by 25 percent • Inflation-adjusted wealth in corporate stocks fell by 50 percent • These wealth reductions shifted the U.S. consumption function downward. • Real disposable income also fell, causing a leftward movement along the consumption function and a further drop in consumption.

Determinants of Investment • Investment, you will remember, consists of expenditures on new buildings and equipment • Gross private domestic investment has been volatile • Consider the planned investment function, and shifts in the function

Example: Adding a Third Dimension Requires New Investment Spending • Of the approximately 40,000 movie screens in the United States, fewer than 8,000 are equipped with digital technology required for projection of three-dimensional (3D) movies. • Conversion to the 3D technology costs about $70,000. • Major movie-theater chains are currently undertaking this investment for more than 1,000 theaters. • This adds up to an aggregate investment expenditure of about $700 million.

Determining Equilibrium Real GDP • We are interested in determining the equilibrium level of real GDP per year • Consumption as a function of real GDP • The 45-degree reference line

Determining Equilibrium Real GDP (cont'd) AD = C + I + G + X • Adding the investment function

Determining Equilibrium Real GDP (cont'd) • Saving and investment: Planned versus Actual • Only at equilibrium real GDP will planned saving equal actual saving • Planned investment equals actual investment • Hence planned saving is equal to planned investment

Figure 12-5 Planned and Actual Rates of Saving and Investment

Determining Equilibrium Real GDP (cont'd) • Unplanned increases in business inventories • Consumers purchase fewer goods and services than anticipated • This leaves firms with unsold products and inventories will rise • Businesses respond by cutting back production and reducing employment

Determining Equilibrium Real GDP (cont'd) • Unplanned decreases in business inventories • Business will increase production of goods and services and increase employment • Ultimately there will be an increase in real GDP

Keynesian Equilibrium with Government and the Foreign Sector Added • To this point we have ignored the role of government in our model • We also left out the foreign sector of the economy in our model • Let’s think about what happens when we add these elements

Keynesian Equilibrium with Government and the Foreign Sector Added (cont'd) • Government (G): C + I + G • Federal, state, and local • Does not include transfer payments • Is autonomous • Lump-sum taxes = G • Lump-Sum Tax • A tax that does not depend on income or the circumstances of the taxpayer

Keynesian Equilibrium with Government and the Foreign Sector Added (cont'd) • The Foreign Sector: C + I + G + X • Net exports (X) equals exports minus imports • Depends on international economic conditions • Autonomous—independent of real national income