Download

1 / 19

190 likes | 269 Vues

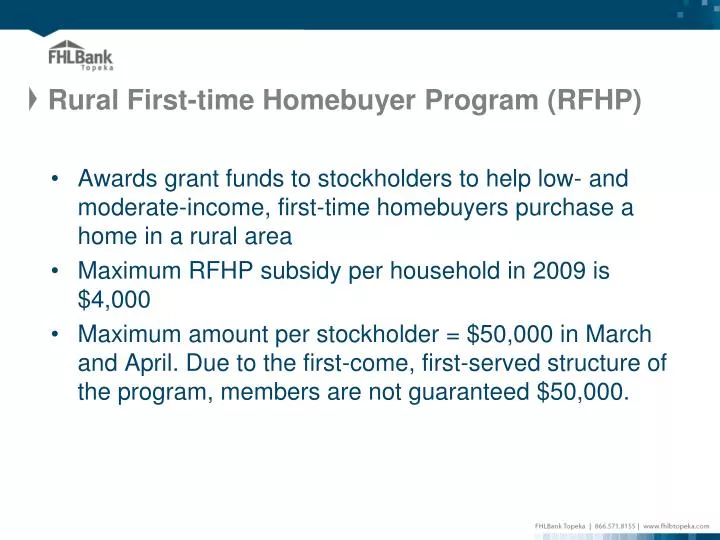

Rural First-time Homebuyer Program (RFHP). Awards grant funds to stockholders to help low- and moderate-income, first-time homebuyers purchase a home in a rural area Maximum RFHP subsidy per household in 2009 is $4,000

E N D

Rural First-time Homebuyer Program (RFHP) • Awards grant funds to stockholders to help low- and moderate-income, first-time homebuyers purchase a home in a rural area • Maximum RFHP subsidy per household in 2009 is $4,000 • Maximum amount per stockholder = $50,000 in March and April. Due to the first-come, first-served structure of the program, members are not guaranteed $50,000.

Member Registration • There will only be one agreement form this year and it is for all of the set aside programs: RFHP, TOP and disaster related assistance • FHLBank notifies member banks of funds available • Members must submit agreements in order to submit disbursement requests • No registration deadlines; Set aside agreements will be accepted from members at any time during the year. • Agreements must be signed by an authorized signer

Rural First-time Homebuyer Program • The maximum per member is increased by $25,000 each month beginning May 1 through August. • There will be six monthly offerings of RFHP funding in 2009. The total RFHP allocation for the year will be divided among the six periods. Disbursement periods will open the first day of the month beginning in March and ending in August this year.

RFHP Criteria • First-time homebuyer with income (documented and qualified by FHLBank Topeka guidelines) < 80% MRB limits • Home must be primary residence and located outside the urbanized area of the central city of MSA • Minimum of $500 down or documented sweat equity, no cash back received • Mandatory homebuyer education • Set aside funds can only be requested by institutions that are members of FHLBank. The lender must be the member institution, USDA or a bona fide nonprofit housing organization.

Eligible Uses of RFHP funds • Down payment • Closing costs • Homebuyer education fees or rehabilitation costs associated with purchase of home • Rehabilitation costs for owner-occupied homes in federally declared disaster areas to address disaster related damage • New construction to replace homes in federally declared disaster areas • Can only be used in conjunction with first mortgage loans originated by FHLBank members

New for 2009 • Closing Costs – Points cannot exceed 1.5% and lender fees cannot exceed 2.5% of the total loan amount New in 2008 • No reservations (More than a third of approved reservations in 2007 were not used) • Rehabilitation of owner-occupied homes damaged in federally declared disaster areas • Waiver of first-time homebuyer requirement for homes being rebuilt in a federally declared disaster area

Disaster Area Repair Assistance • Set aside funds can now be used in rural federally declared disaster areas • Household does not have to be first-time homebuyer • Set aside funds must be used for costs related to damage associated with disaster and new construction of homes in a federally declared disaster area • Use Disaster Related funds request form on our website for owner-occupied rehab. Use regular RFHP funds request form for new construction.

Rural Location • Rural = located outside of the urbanized area of the central city of a Metropolitan Statistical Area (MSA) • Examples of ineligible communities: Lincoln and Omaha

$500 Down Payment or Equivalent • Down payment • Equity contribution (ex. lot on which new house was built or sweat equity contributed through a self-help housing program) • Costs paid outside of closing • provide documentation of cost of appraisal, loan application, inspections, etc. if POCs are not shown on HUD 1 • Gifts cannot be used as part of the $500 down payment • Documented Sweat Equity – Self-help and Habitat programs

Mandatory Homebuyer Education • Complete “acceptable” homebuyer counseling program prior to disbursement, including training provided by: • HUD-approved Housing Counseling Agency • FHLBank approved • State Homebuyer Education Association Certified (ex. REACH, OHEA) • Provide certificate of completion or name of training agency • Training based on a recognized homebuyer education program • FHLBank Topeka prefers classroom counseling, though phone or web-based training may be satisfactory depending on the circumstances. A list of classes for each state is available on our website.

Using RFHP to Pay Counseling Costs • RFHP funds may be used to pay for counseling costs only when: • Incurred in connection with counseling of homebuyers who purchase an RFHP-assisted unit • Costs have not been covered by another source, including the stockholder bank

Funds Disbursed • Credited to stockholder demand-deposit account • Stockholders must disburse to eligible households within 60 days after receiving set aside funds.

Retention Period • 5-year retention secured by lien requires: • Notice of any sale or refinancing of the unit during that period • If sold, repayment of a pro rata share of the subsidy upon sale, reduced by 1/60 per month for every month the RFHP-assisted borrower owned the unit or sale to an RFHP-qualified buyer • If refinanced, FHLBank will subordinate its position to the first lender

Targeted Ownership Program (TOP) • Awards grant funds to stockholders to help first-time homebuyers that have a disabled household member to purchase a home. • Funds up to $4,000 per qualified homebuyer. • Cannot be used for RFHP or AHP assisted households. • There will not be a separate TOP offering this year. All set aside programs will begin March 1.

TOP Criteria Same as RFHP except: • TOP funds can be used in urban and rural areas. • Need proof of disability – social security payment that shows individual is disabled or medical documentation from physician. • Disability means a physical or mental impairment that substantially limits one or more of the major life activities of an individual.

Changes to 2009 AHP Program • One round of AHP for 2009 with a submission deadline of May 1, 2009. • Maximum amount of AHP in 2009 - $350,000.

FHLBank Topeka’s Housing and Community Development Staff – 866.571.8155 • Chris Imming, Director and First VP, ext. 6029 • Dawn Harris, HCD Assistant, ext. 6030 • Mark Ward, Operations and Community Programs Manager, ext. 6037 • Noelle St. Clair – Community Dev. Specialist, ext. 6033 • Casey Howard, Compliance Specialist, ext. 6237 • Michele Carter, AHP Homeownership Supervisor, ext. 6032 • Utika Scales, HCD Specialist, ext. 6035 • Jeff Ragsdale, AHP Rental Supervisor, ext. 6034 • Amy Apitz, HCD Specialist, ext. 6031