Download

1 / 35

370 likes | 673 Vues

Economics The study of the allocation of scarce resources that have alternative uses . What is Economics?. Economics is the study of human efforts to satisfy what appear to be unlimited and competing wants and needs through the careful use of relatively scarce resources. Wants vs. Needs.

E N D

Economics The study of the allocation of scarce resources that have alternative uses.

What is Economics? • Economics is the study of human efforts to satisfy what appear to be unlimited and competing wants and needsthrough the careful use of relatively scarce resources

Wants vs. Needs Needs Wants The things we choose to use to satisfy our needs Those things required for survival Utility- measures how much a person’s situation is improved or how much satisfaction a person draws from their decisions.

Unlimited and Competing Wants • What do you want? Relatively Scarce Resources • What don’t we have enough of?

Scarcity and the Factors of Production • Scarcity -The fact that there aren’t enough resources available to satisfy all our desires • Factors of Production -The resources used to produce goods & services -Land -Labor -Capital -Entrepreneurship • Examples of Factors of Production that go into building a house

PROBLEM DUE TO SCARCITY • Choices must be made among a limited set of possibilities – TRADE-OFFS • The decision to have more of one thing means that we will have less of something else • THE STUDY OF THESE DECISIONS AND HOW THEY ARE MADE IS THE STUDY OF ECONOMICS

Homework Assignment • Read pages 5-11 Pay particular attention to -Opportunity Costs -Production Possibilities Curves -Principle of Increasing Costs

Scarcity Activity • Step 1: Go to www.realestate.com • Step 2: Enter your zip code and a price range of $500,000 to $1,000,000 and search • Step 3: Find a house you like and list the features of the house that most attracted you • Step 4: Go back and search in a price range of $300,000 to $500,000 • Step 5: Find a house you like in this price range • Step 6: Compare the first house you chose in Step 3 to the house you chose in Step 5 • Step 7: What did you have to give up?

Opportunity Costs • The benefit of the next best alternative use of scarce resources • What is given up in order to get something else • What did you lose in a trade-off? • The true cost of a car is not its market price but the value of other things (like refrigerators) that could have been made instead

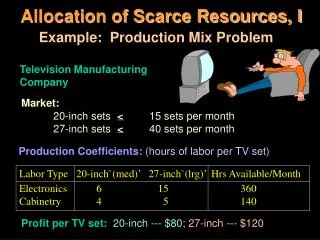

Production Possibilities Frontier • A diagram that shows the different combinations of goods that a producer can turn out given the available resources and the existing technology. • Each point on the production possibilities curve depicts an alternative mix of output

Production Possibilities Frontier • Create a PPF based on the following; -With its resources, a producer of TVs and computers can produce either 20 TVs or 10 computers (x axis-computers, Y axis-TVs) • Plot the following combinations of production • 4 TVs and 8 computers (Label it A) • 6 TVs and 7 computers (Label it B) • 8 TVs and 4 computers (Label it X) • 14 TVs and 10 computers (Label it Y)

Production Possibilities Frontier • Points A and B • Attainable and desirable points • Point X • Attainable but not desirable • Why isn’t this desirable? • Point Y • Desirable but not attainable • Why isn’t this attainable? • What would make it attainable

Production Possibilities Frontiers • Downward sloping because of ______________________ • Movement along the PPF indicates a _________________ • Making more of one means _________________________ • How much has to be given up is the __________________ • In this situation, with a linear PPF, the opportunity cost is ___________________ because the resources used in the production of both goods are basically _______________

A 5 B 4 C 3 OUTPUT OF TRUCKS D 2 E 1 F 0 1 2 3 4 5 OUTPUT OF TANKS Production Possibilities Frontiers – A More Realistic Look • Y • X • Still downward sloping because of ____________________ • Movement along the PPF still indicates a ______________ • Making more of one still means ______________________ • How much has to be given up is still the _______________

Production Possibilities FrontiersA More Realistic Look • Law of Increasing Opportunity Costs • The shape of the curve illustrates increasing opportunity costs. • Resources used to produce trucks aren’t ideally suited for producing tanks. • Resources do not transfer perfectly from the production of one good to another. • Increasing quantities of any good can be obtained only by sacrificing ever-increasing quantities of other goods.

Law of Increasing Opportunity Costs A 5 B C 4 D 3 OUTPUT OF TRUCKS E 2 1 F 0 1 2 3 4 5 OUTPUT OF TANKS Each time there is a one unit increase in the production of tanks (A to B, B to C, C to D, D to E, E to F), the amount of trucks that must be given up continues to increase.

Scarcity and Choice for an Entire Economy • Scarcity and choice are problems facing every society (economy) • Countries must decide what the make up of the output will be • Do we produce for today or do we produce for tomorrow? • What are the consequences of our choice?

Scarcity and Choice for an Entire Economy • Consumer goods • Goods that are available for immediate use by households but do not contribute directly to future production • Capital Goods • Goods that are used to produce other goods and services in the future rather than being consumed today

PPF For Entire Economy CAPITAL GOODS • JN • US CONSUMER GOODS

Homework Assignment • Read pages 11-15 1. Describe the three core economic questions 2. How are the questions answered in; -A market Economy (Adam Smith) -A command economy (Karl Marx) -In between (John Maynard Keynes) 3. Describe the on-going debate. 4. What is meant by a “mixed economy”?

Three Basic Economic Questions • Every society (economy) must answer them • How each society (economy) answers the questions depends on their economic system • The Questions • WHAT to produce? • HOW to produce? • FOR WHOM to produce? LO2

WHAT? • What to Produce? • What combination of goods and services should we produce? • On what should we use our scarce resources? • In a market economy • The question is answered by….. THE CONSUMER • The answer to the question is….. WHATEVER THE CONSUMER IS WILLING TO BUY LO2

HOW? • How to Produce? • What is the best way to utilize our scarce resources? • What are the best methods of production? • In a market economy • The question is answered by….. THE PRODUCERS • The answer to the question is…. IN THE MOST EFFICIENT MANNER POSSIBLE LO2

FOR WHOM? • For whom will the products be produced? • Who is going to get the output produced? • In a market economy • The answer to the question is…. WHOEVER HAS THE RESOURCES TO PURCHASE THE PRODUCTS WHOEVER CAN AFFORD IT • Why would this be considered one of the weaknesses of a market economy? LO2

The Mechanism of Choice • An economy is largely defined by how it answers the WHAT, HOW and FOR WHOM questions. LO3

The Invisible Hand of a Pure Market Economy (Smith) • The market mechanism is the use of market prices and sales to signal desired outputs (or resource allocations). • The market decides the mix of output in an economy. • Laissez faire is the doctrine of leave it alone — of nonintervention by government in the market mechanism. LO3

Command Economies (Marx) • Karl Marx argued that the government not only had to intervene but had to own all the means of production. • Why? • Markets permit capitalists to enrich themselves while the proletariat toil long hours for subsistence wages • Government (in the name of the people) would answer the basic economic questions LO3

Government Intervention (Keynes) • John Maynard Keynes offered a less drastic solution. • In Keynes’ view, government should play an active but not an all-inclusive role in managing the economy. • When the economy needed help, the government should step in to stimulate or slow down the economy LO3

Continuing Debates • The core of most debates is some variation of the WHAT, HOW, or FOR WHOM questions. • Conservatives favor Adam Smith’s laissez-faire approach. • Liberals tend to think government intervention is likely to improve the answers. • Countries answer the basic economics questions differently and their answers change over time LO3

A Mixed Economy • A mixed economy is one that uses both market signals and government directives to allocate goods and resources. • Most economies use a combination of market signals and government directives to select economic outcomes. • The challenge for society is to minimize failures by selecting the appropriate balance of market signals and government directives. LO3

Macro Versus Micro • Macroeconomics is the study of aggregate economic behavior, of the economy as a whole. • Microeconomics is the study of individual behavior in the economy, of the components of the larger economy.

Theory Versus Reality • The economy is much too vast and complex to describe and explain in one course (or one lifetime). • Economists use theories, or models, of economic behavior to evaluate and design economic policy.

Theory Versus Reality • In these theories, we typically ignore the possibility that many things can change at one time. • Ceteris paribus is the assumption that nothing else is changing.

Politics and Economics • Political forces are a necessary ingredient in economic policy decisions. • It would be very difficult to separate the two • Inevitably, political choices must be made.