Download

1 / 32

320 likes | 492 Vues

Short - form report (clean opinion). All 4 statements and full disclosure GAAP GAAS (sufficient evidence) No other circumstances. Parts of Audit Report. 1. Title 2. Report addressee 3. Introduction 4. Scope 5. Opinion 6. CPA name 7. Date - end of fieldwork. Expectation Gap.

E N D

Short - form report(clean opinion) • All 4 statements and full disclosure • GAAP • GAAS (sufficient evidence) • No other circumstances

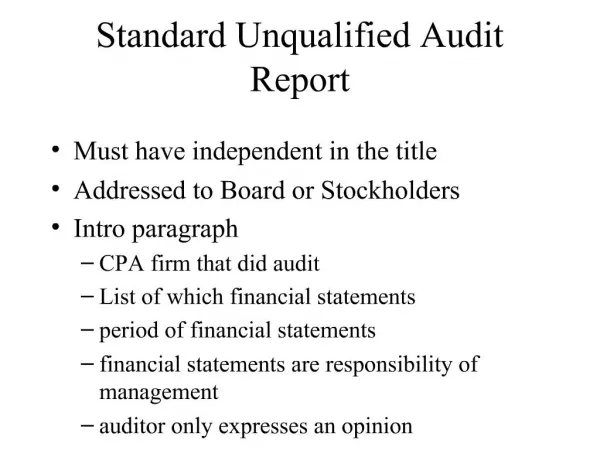

Parts of Audit Report • 1. Title • 2. Report addressee • 3. Introduction • 4. Scope • 5. Opinion • 6. CPA name • 7. Date - end of fieldwork

Expectation Gap • Public Expects • Expectation • Gap • Audit • Provides • Pre - 89 (2002?) Today

Key Report Elements • Introduction- Management is responsible • Scope • 1. Reasonable assurancethat statements are free of material misstatement • 2. Evidence is sufficient • 3. Test basis • Opinion- not a guarantee,judgmentis involved

Comparison of Deloitte and PwC Report • Content is same - PwC combines the three paragraphs • PricewaterhouseCoopers • IntroductionScopeOpinion

Audit Report on Internal Control • Required under Section 404 of Sarbanes-Oxley Act for public companies • Applicable for fiscal years after 12/14/04 for accelerated filers (cap > $75 million) • Effective date extended to 12/15/09 for other filers

Audit Report on Internal Control • Auditor’s report on internal control can be combined with financial statement audit report or issued separately • Combined report includes paragraphs on definition and inherent limitations of internal control • Report is as of the end of the company’s fiscal year • Auditor’s report date same as date of auditor’s report on financial statements

Types of Audit Reports • Standard Unqualified • Unqualified with Explanatory Paragraph • Qualified (Opinion only - GAAP or Scope and Opinion - GAAS) • Adverse (not fair - GAAP) or Disclaimer (no opinion - GAAS)

Explanatory Paragraphs • Going Concern • Consistency • Agree with Departure • Emphasis of Matter

Consistency Explanatory Paragraph • Applies whenever a change in accounting method (principle) • Voluntary or mandatory • Voluntary change must be to • preferable method

Consistency vs. Comparability • Consistency - Change in principle and explanatory paragraph • (ex. SL to accelerated depr.) • Comparability - Change in estimate with no explanatory paragraph • (ex. Increased in life of fixed assets)

Other Auditors • Assume No reference • Responsibility Unqualified • SharedModified Wording • Responsibility (All 3 para.) • No Responsibility Qualified or • Disclaimer

MC 3-24 (a) • An entity changed from the straight-line method to the declining balance method for all newly acquired assets. The change has no material effect on the current year f/s, but is reasonably certain to have a material effect in later years. If the change is adequately disclosed, the auditor should issue a(n) : • 1. Qualified opinion. • 2. Unqualified opinion w/ explanatory paragraph. • 3. Unqualified opinion. • 4. Qualified opinion with explanatory paragraph regarding consistency.

Types of Reports • Auditor has Auditor lacks • Materiality knowledge knowledge • level (not GAAP) (non-GAAS) • Immaterial Unqualified Unqualified • Material Qualified Qualified scope • opinion and opinion • Highly • material Adverse Disclaimer

Auditor has Auditor lacks • Materiality knowledge knowledge • level (not GAAP) (non-GAAS) • Immaterial Unqualified Unqualified • Material Qualified Qualified scope • opinion and opinion • Highly • material Adverse Disclaimer

Auditor hasAuditor lacks • Materiality knowledgeknowledge • level (not GAAP)(non-GAAS) • Immaterial UnqualifiedUnqualified • Material QualifiedQualifiedopinionscope and • opinion • Highly • material AdverseDisclaimer

Practice MC • In which of the following situations would an auditor normally choose between an “except for” qualified opinion or and adverse opinion? • 1. The auditor did not observe the entity’s • beginning inventory and is unable to apply • alternative procedures. • 2. The financial statements fail to disclose • information required by GAAP. • 3. The auditor is asked to report on the balance • sheet only. • 4. Events disclosed in the f/s cause the auditor to • have doubts about going concern.

MC 3-25 (a) • The CPA will issue an adverse auditor’s opinion if: • 1. The scope is limited by the client. • The exception is so material that an “except • for opinion is not justified. • The auditor did not perform sufficient • procedures to form an opinion. • Major uncertainties exist concerning the • company’s future.

MC #1 (p. 23 of notes) • Green was appointed auditor after y/e and was unable to confirm receivables. Green applied other procedures and was satisfied as to the account balance. His opinion is most likely: • 1. Unqualified opinion • 2. Unqualified with explanatory paragraph • 3. Qualified due to scope limitation • 4. Qualified due to departure from GAAS

Materiality • A misstatement is material if it would affect the decision of a reasonable user • Usually defined as 5-10% of net income • Need to consider multiple bases • Qualitative factors

Location of 4th Paragraph • QualificationsBefore • opinion • Explanatory After • paragraph opinion

Report Key Wording Para. Mod. • Qualified “Except for” Opinion • opinion • Adverse “Do not present • fairly”Opinion • Qual. Scope & • S & O “Except for” Opinion • Disclaimer “Do not express Opinion • an opinion No Scope

Problem 3-28 • 1.Inventory scope restriction • Qualified Scope & Opinion or Disclaimer • Probably disclaimer: • Amount unknown • Client imposed

Problem 3-28 • 3. Supervisor has material investment in • client (materiality not a factor) • Disclaimer (lack of independence)

Problem 3-28 • 4. Change from purchasing to leasing trucks • Unqualified(change in financing is not a change in method)

Problem 3-28 • 5. Unable to Test Beginning • Balances • Unqualified on B/S • (ending balance) • Disclaimer on I/S and C/F • (flows depend on beginning balance)

Problem 3-28 • 6. Inventory scope limitation, satisfied by • alternative procedures • Unqualified

Problem 3-30 • 1. Heavy fire to client plant - not disclosed in footnotes. • Qualified opinion only - except for • (Lack of disclosure is non-GAAP)

Problem 3-30 • Improper revenue recognition • Unqualified - Standard (1) • Not GAAP; but immaterial • Observed ending inventory, but not beginning inventory. • Unqualified on balance sheet • Disclaimer on income statement and • cash flows

Problem 3-30 • 4. CPA not allowed to review minutes. Offered copies of resolutions. • Probably disclaimer (6) • materiality not known • client imposed

Problem 3-30 • 6. Increased value of inventory to replacement cost based on supplier price increase. • Qualified opinion only • - except for (4) • Replacement cost • not GAAP, material

Problem 3-30 • 7. Changed life of buses from 10 years to 12 years. CPA agrees with change. • Unqualified - standard wording • (change in estimate, • not change in method)