Download

1 / 66

670 likes | 792 Vues

April 17th, 2010. Heidi Shierholz Economist, Economic Policy Institute. National Association of Planning Councils 2010 National Conference. after the great Recession. First things first, Where are we now?. Technically, recession is almost surely over. But over for whom??.

E N D

April 17th, 2010 Heidi Shierholz Economist, Economic Policy Institute National Association of Planning Councils 2010 National Conference after the great Recession

Layoffs now at pre-recession levels Source: Bureau of Labor Statistics, Job Openings and Labor Turnover survey

But hiring still incredibly low Source: Bureau of Labor Statistics, Job Openings and Labor Turnover survey

Unemployment rate Source: Bureau of Labor Statistics, Current Population Survey

But, the short- and medium-term are going to be ugly. The recovery in the labor market is going to take a very long time. Important – we Do not have to settle for Permanently High unemployment!

To fill the 11 million jobs-gap by March 2011, we would need to add 1 million jobs every month between now and then. To fill it by March ‘12, need 559,000 jobs per month. To fill it by March ‘13, need 408,000 jobs per month. To fill it by March ‘14, need 333,000 jobs per month. To fill it by March ‘15, need 288,000 jobs per month. Employment growth needed to fill in the gap Source: Author’s analysis of Current Establishment Survey data.

Unemployment, 2015 Source: Author’s analysis of Bureau of Labor Statistics, Current Population Survey data

MORE SPENDING FOR JOBS! (Important subtext: ARRA worked, but wasn’t big enough) What should be done?

Perhaps counterintuitive, but true! A key way to bring the deficit down is to deficit spend to create jobs

Case against deficits in a healthy economy • In a healthy economy, the private sector is borrowing all the available “loanable funds” to make investments. (Investments are good, because they lead to productivity growth, and productivity growth is what leads to rising living standards.) • If the government runs big deficits – i.e. also wants to borrow a lot – then it is competing with the private sector for those loanable funds. This competition bids up the price of those funds – i.e. bids up interest rates. • Higher interest rates lead to less private-sector investment – i.e. government borrowing “crowds out” investment. And that is bad (see above!)

In short, Right now there is plenty of room for the government to borrow without causing anything bad to happen!

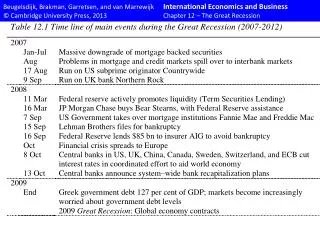

So deficit spending is what we need in the short run. But what about the long-run? What’s the Root cause of our long-run deficit problems?

In longer-run, we have a health-care problem, not a social security problem Spending on Social Security, % of GDP

It’s all about runaway health care costs, NOT an aging population

For more information Heidi Shierholz hshierholz@epi.org 202.533.2560 Economic Policy Institute 1333 H Street, NW Suite 300, East Tower Washington, DC 20005-4707 202.775.8810 www.epi.org

And, trade deficits are driven byover-valued dollar, not fiscal profligracy

Generational inequity? Those determined to worry about generational distribution need to focus on trade, not budget deficits Budget deficit => higher taxes tomorrow, but these higher taxes just get recycled into higher interest payments for bondholders Trade deficit => excess of imports over exports financed by transferring ownership of domestic assets to foreign lenders – money spent today that really does get foregone tomorrow

Why is deflation bigger worry? Increases real burden of a given debt $1,000 mortgage gets more and more burdensome if prices/salaries begin falling Increases real interest rates real interest rate = nominal rate - inflation