Download

1 / 26

270 likes | 430 Vues

Federal Cost Principles. Georgia Department of Education School Nutrition Program Finance & Budget Unit Edward Dung. Statutory Authorization. Title 2 Part 225 Code of Federal Regulation (CFR) OMB Circular A – 87 Title 2 Part 230 Code of Federal Regulation (CFR) OMB Circular A – 122

E N D

Federal Cost Principles Georgia Department of Education School Nutrition Program Finance & Budget Unit Edward Dung

Statutory Authorization • Title 2 Part 225 Code of Federal Regulation (CFR) • OMB Circular A – 87 • Title 2 Part 230 Code of Federal Regulation (CFR) • OMB Circular A – 122 • Appendix A • Appendix B

Importance of Cost Principles • In order to be chargeable to the Child Nutrition Program, a cost (whether a direct or indirect cost) must be allowable under federal guidelines for the administration and operations of the CNP.

Objectives • Restrict the use of program funds to ensure expenses are incurred to meet ONLY the needs of the intended program {Child Nutrition Program (CNP)}. • Ensure compliance with government-wide and specific rules and regulations.

Factors To Consider In Deciding Allowable Costs • A cost item is allowable if it is: • Necessary • Reasonable • Allocable • Not prohibited under state or local laws • Conform to the limitations of the Federal Award

Factors To ConsiderIn Deciding Allowable Costs • A cost item is allowable if it is: • Consistently treated as a direct or indirect cost • Determined in accordance with GAAP • Net of applicable credits • Adequately documented

What Costs areReasonable & Necessary • Could the SNP operations be carried out without incurring this cost? • Would a prudent person find the cost to be reasonable under the circumstances? • Is the cost recognized as ordinary and necessary for the operation of SNP? • How does the cost contribute to achieving SNP objectives? • Could the SFA defend this purchase to the SA, the media, auditors, and other SNP stakeholders?

What Costs are Allocable • The CNP must benefit, directly or indirectly, from the cost incurred. • Each cost objective must be charged its fair share of the cost and adequate documents retained. • Costs may not be billed to the SNP to overcome fund deficiencies in other Federal Program(s) or School District or to avoid certain regulatory limitations.

Points To Remember • The list of cost items in Appendix B is extensive but not exhaustive. • A cost item may be unallowable, based on the application of Appendix A, even though it is listed as allowable in Appendix B.

Application of Cost Principles • Example 1: Murals • A school cafeteria is renovated and the cost includes expenditures for a mural. Is this cost allowable? • It depends • A mural would be allowable if it conveys some sort of message that promotes the program. Otherwise, it will be unallowable. Carefully consider the reasonableness of the mural.

Application of Cost Principles • Example 2: Lunch Room Monitors • An SFA pays a fee to individuals to monitor students in the cafeteria. Is the fee paid to the lunch room monitors allowable? • Yes • Fees for lunch room supervision can be considered an allowable cost of operations. FNS Instruction 782-6

Application of Cost Principles • Example 3: Construction • A new school is built and part of the cost of building the cafeteria is billed to the SNP. Is the cost assigned to the SNP allowable? • No • 7CFR 210.14 Specifically disallows the purchase or constructing a building or the purchase of land unless prior approval is obtained from FNS.

Application of Cost Principles • Example 4: Renovations/Remodeling/Reconstruction • A section of the cafeteria is reconstructed to properly locate the POS system to comply with meal count requirements. Is this cost of the reconstruction an allowable cost? What if the cost adds to the value of the cafeteria or prolongs its intended life? • Yes • It is a cost incurred to comply with federal requirements for the operations of SNP. However, it should not add to the value of the property or prolong its intended life.

Application of Cost PrinciplesOther Examples • Promotional Items • SNP Employee Incentives • Vehicles • Charges • Not Allowable • Allowable • Allowable • Not Allowable

Meaning of Indirect Cost • Indirect cost are costs incurred for the benefit of multiple programs, functions, or other cost objectives. • Indirect cost billed to the SNP must first be allowablecost for reasonable and necessary operations of the SNP.

Indirect Cost vs. Direct Cost • An indirect cost in one given circumstance could be a direct cost in another. • A cost item cannot be treated as a direct cost to the SNP if the same cost is treated as a indirect cost in other federal programs.

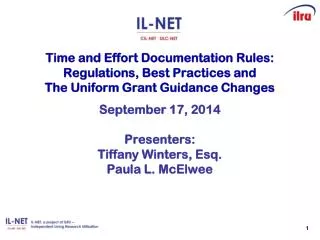

Water AT&T Georgia Power GNG Invoice Invoice Finance Office Indirect Cost SNP Allocation Instructions School Nutrition School Improvement Title 1

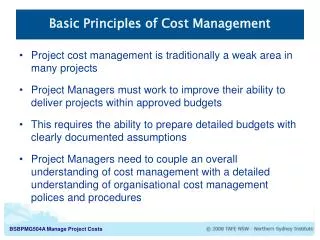

Water AT&T Georgia Power GNG Finance Office Direct Cost to SNP Indirect Cost SNP Allocation School Nutrition Instructions School Improvement Title 1

Application of Indirect Cost • The general fund often bills the food service for its share of the indirect by applying the State-approved indirect cost rate to the SNP adjusted cost base OR allocates indirect cost based of a more reasonable methodology. • The billed amount generated is the amount of indirect cost properly allocable to the school food service.

SFA must not overpay! • An SFA is NOT allowed to pay any amount in excess of the properly billed indirect cost with funds from the nonprofit school food serviced account. • SFAs paying indirect cost MUST be provided the necessary tools to verify and validate costs when necessary

Retroactive Billing Of Indirect Cost Is Unallowable • It is unallowable to bill the nonprofit school food service account for indirect costs that were paid from the general fund in prior years. • Unless an agreement exists indicating it was a loan to the SNP.

Shifting Indirect Cost IsUnallowable! • Shifting indirect cost to SNP because other programs do not have enough funds is NOT an option.

Edward Dung Auditor School Nutrition Program Finance and Budget Unit edung@doe.k12.ga.us

In accordance with State and Federal Law, the Georgia Department of Education prohibits discrimination on the basis of race, color, religion, national origin, sex, disability, or age in its educational and employment activities. Inquiries regarding the application of these practices may be addressed to the General Counsel of the Georgia Department of Education, 2052 Twin Towers East, Atlanta, Georgia, 30334, (404) 656-2800.In accordance with Federal law and U.S. Department of Agriculture policy, this institution is prohibited from discriminating on the basis of race, color, national origin, sex, age, or disability. To file a complaint of discrimination, write to USDA, Director, Office of Civil Rights, 1400 Independence Avenue, SW, Washington, DC 20250-9410 or call (800) 795-3272 or (202) 720-6382 (TTY). USDA is an equal opportunity provider and employer.