Download

1 / 61

610 likes | 743 Vues

Monetary Policy and Foreign Exchange Rates. FUNDAMENTAL ISSUES. What is the monetary approach to exchange-rate determination? What are the main assets and liabilities of central banks? How do a central bank’s foreign-exchange market interventions alter the monetary base and the money stock?

E N D

FUNDAMENTAL ISSUES • What is the monetary approach to exchange-rate determination? • What are the main assets and liabilities of central banks? • How do a central bank’s foreign-exchange market interventions alter the monetary base and the money stock? • What is the portfolio approach to exchange-rate determination? • Should central banks sterilize foreign exchange interventions?

Monetary Approach • The Monetary Approach focuses on the supply and demand of money and the money supply process. • The monetary approach hypothesizes that exchange-rate movements result from changes in money supply and demand.

The Monetary Base • A nation’s monetary base can be measured by viewing either the assets or liabilities of the central bank. • Its assets are domestic credit (DC or DA), comprised of domestic sovereign debt/bonds, and foreign exchange reserves (FER or FACB), comprised of foreign sovereign debt/bonds. • Its liabilities are currency in circulation (C) and total reserves of member banks (TR).

Simplified Balance Sheet of a Central Bank Assets Liabilities Currency (C) Domestic Credit (DC) Foreign Exchange Reserves (FER) Total Reserves (TR) Monetary Base (MB) Monetary Base (MB)

Money Stock • There are a number of measures of a nation’s money stock (M). • The narrowest measure is the sum of currency in circulation and the amount of transactions deposits (TD) in the banking system.

Money Multiplier • Most nations require that a fraction of transactions deposits be held as reserves. • The required fraction is determined by the reserve requirement (rr). • This fraction determines the maximum change in the money stock that can result from a change in total reserves.

Money Multiplier • Under the assumption that the monetary base is comprised of transactions deposits only, the multiplier is determined by the reserve requirement only. • In this case, the money multiplier (m) is equal to 1 divided by the reserve requirement, m = 1/rr.

Relating the Monetary Base and the Money Stock • Under the assumptions above, we can write the money stock as the monetary base times the money multiplier. M = mMB = m(DC + FER) = m(C + TR). • Focusing only on the asset measure of the monetary base, the change in the money stock is expressed as M = m(DC + FER).

Example - BOJ Intervention • Suppose the Bank of Japan (BOJ) wanted to intervene to weaken the yen, what would it do? Buy Dollars ($) = Sell Yen

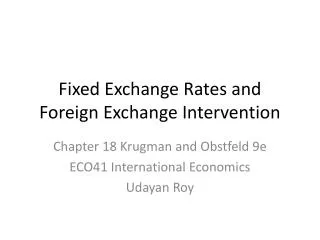

Spot Exchange Rate Domestic currency units/foreign currency units SFC S2 S1 DFC’ DFC Quantity of foreign currency. Q1 Q2

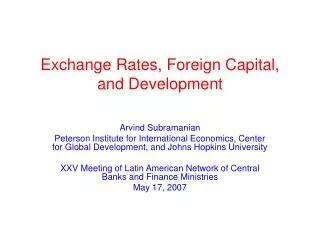

Example - BOJ Intervention This action increases the foreign exchange reserves (FER) and total reserves (TR) components of the BOJ’s balance sheet.

Example - BOJ Intervention • Suppose the Bank of Japan (BOJ) intervenes to weaken the yen by buying ¥1 trillion US dollars from the private banking system.

BOJ Balance Sheet Assets Liabilities DC C FER TR +¥1 million +¥1 million MB MB +¥1 million +¥1 million

BOJ Intervention • Because the monetary base increased, so will the money stock. • Suppose the reserve requirement is 10 percent. The change in the money stock is M = m(DC + FER), M = (1/.10)(¥1 trillion) = ¥10 trillion.

BOJ Intervention • Other things equal, what happens when we increase the money stock? • Answer: We increase aggregate demand. At full employment, that means inflation.

BOJ Intervention • Other things equal, what happens when we increase the money stock? • Answer: We increase aggregate demand. At full employment, that means inflation. • So how do we sterilize the effect of increasing foreign exchange reserves (FER) on the money supply?

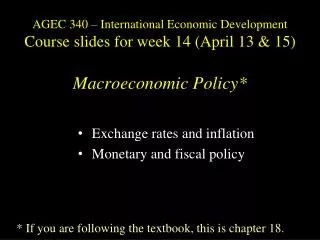

BOJ Intervention • The Bank of Japan (BOJ) would compensate for buying ¥1 trillion US dollars from the private banking system by selling ¥1 trillion domestic bonds.

BOJ Balance Sheet Assets Liabilities DC -¥1 million C FER TR +¥1 million MB MB

BOJ Intervention • What effect would selling ¥1 trillion domestic bonds have?

BOJ Intervention • What effect would selling ¥1 trillion domestic bonds have? C.P., Price of domestic bonds will fall, yields rise, demand for yen increase, putting greater pressure on BOJ to buy dollars. This implies that BOJ can control exchange rates (S) or interest rates, but not both.

BOJ Intervention There is an exception: where locals are averse to exchange risk, i.e., they have a strong preference for home currency. BOJ can keep this policy up as long as interest on FER is higher than on DC. Which is as long as Japanese savers prefer lower yield Japanese debt to higher yield foreign debt.

The Portfolio Approach • The portfolio approach expands the monetary approach by including other financial assets. • The portfolio approach postulates that the exchange value is determined by the quantities of domestic money and domestic and foreign financial securities demanded and the quantities supplied.

The Portfolio Approach • Assumes that individuals earn interest on the securities they hold, but not on money. • Assumes that households have no incentive to hold the foreign currency. • Hence, wealth (W), is distributed across money (M) holdings, domestic bonds (B), and foreign bonds (B*).

The Portfolio Approach • A domestic household’s stock of wealth is valued in the domestic currency. • Given a spot exchange rate, S, expressed as domestic currency units relative to foreign currency units, a wealth identity can be expressed as: W M + B + SB*.

The Portfolio Approach • The portfolio approach postulates that the value of a nation’s currency is determined by quantities of these assets supplied and the quantities demanded. • In contrast to the monetary approach, other financial assets are as important as domestic money.

An Example • Suppose the domestic monetary authorities increase the monetary base through an open market purchase of domestic securities. • As the domestic money supply increases, the domestic interest rate falls. • With a lower interest, households are no longer satisfied with their portfolio allocation. • The demand for domestic bonds falls relative to other financial assets.

Example - Continued • Households shift out of domestic bonds. • They substitute into domestic money and foreign bonds. • Because of the increase in demand for foreign bonds, the demand for foreign currency rises. • All other things constant, the increased demand for foreign currency causes the domestic currency to depreciate.

Spot Exchange Rate Domestic currency units/foreign currency units SFC S2 S1 DFC’ DFC Quantity of foreign currency. Q1 Q2

Interest Rates I Instrument Yields and Financial Instrument Prices 1. Alternative Measures of Interest Yields a. Nominal Yield b. Coupon Return c. Current Yield d. Yield to Maturity 2. Discounted Present Value 3. Price of a Bond 4. Term to Maturity 5. Interest Rate Risk

Interest Rates II Term Structure of Interest Rates 1. Yield Curves 2. Segmented Markets Theory 3. Expectations Theory 4. Preferred Habitat Theory

Interest Rates III Risk Structure of Interest Rates 1. Default Risk 2. Liquidity 3. Tax Differentials

Nominal rate (iNom) • Stated in contracts, and quoted by banks and brokers. • Not used in calculations or shown on time lines • Periods per year (m) must be given. • Examples: • 8%; Quarterly • 8%, Daily interest (365 days)

Periodic rate (iPer ) • iPer = iNom/m, where m is number of compounding periods per year. m = 4 for quarterly, 12 for monthly, and 360 or 365 for daily compounding. • Used in calculations, shown on time lines. • Examples: • 8% quarterly: iPer = 8%/4 = 2%. • 8% daily (365): iPer = 8%/365 = 0.021918%.

Effective Annual Rate(EAR = EFF%) • The EAR is the annual rate which causes PV to grow to the same FV as under multi-period compounding Example: Invest $1 for one year at 12%, semiannual: FV = PV(1 + iNom/m)m FV = $1 (1.06)2 = 1.1236. • EFF% = 12.36%, because $1 invested for one year at 12% semiannual compounding would grow to the same value as $1 invested for one year at 12.36% annual compounding.

An investment with monthly payments is different from one with quarterly payments. Must put on EFF% basis to compare rates of return. Use EFF% only for comparisons. • Banks say “interest paid daily.” Same as compounded daily.

m EFF% = - 1 (1 + ) iNom m How do we find EFF% for a nominal rate of 12%, compounded semiannually? (1 + ) 2 0.12 2 = - 1.0 = (1.06)2 - 1.0 = 0.1236 = 12.36%.

EAR (or EFF%) for a Nominal Rate of of 12% EARAnnual = 12%. EARQ = (1 + 0.12/4)4 - 1 = 12.55%. EARM = (1 + 0.12/12)12 - 1 = 12.68%. EARD(365) = (1 + 0.12/365)365 - 1 = 12.75%.

Can the effective rate ever be equal to the nominal rate? • Yes, but only if annual compounding is used, i.e., if m = 1. • If m > 1, EFF% will always be greater than the nominal rate.

When is each rate used? iNom: Written into contracts, quoted by banks and brokers. Not used in calculations or shown on time lines.

When is each rate used? iPer: Used in calculations, shown on time lines. If iNom has annual compounding, then iPer = iNom/1 = iNom.

The amount of credit extended via the purchase of a financial instrument is the A. front load. B. present discounted value. C. principal. D. sum of the coupons Answer: C

The coupon yield divides the coupon value by the ________ whereas the coupon value divides the coupon by the ________. A. bond’s face value; price of the bond B. price of the bond; bond’s face value C. nominal interest rate; real interest rate D. sum of the coupons; sum of the coupons and principal Answer: A

The rate of return that the owner of and instrument would earn by holding the instrument until maturity is called the A. coupon yield. B. coupon value. C. nominal rate of return. D. yield to maturity. Answer: D

To calculate the price of an instrument one must find the A. present discounted value of the stream of coupon payments and principal. B. sum of the coupons divided by the principal. C. sum of the coupons plus the principal. D. principal plus the present discounted value of the coupons Answer: A

A bond with no fixed maturity date is called a A. treasury bill. B. callable bond. C. perpetuity. D. discount bond. Answer: C

A bond with an infinite payment life will have a price A. that is arbitrarily high, as it will produce coupon payments forever. B. of the present discounted value of its principal. C. of the coupon amount divided by the interest rate. D. of the coupon amount divided by one plus the interest rate. Answer: C