Download

1 / 23

230 likes | 283 Vues

COORDINATING RETIREMENT INCOME Where Does Social Security Fit?.

E N D

COORDINATING RETIREMENT INCOME Where Does Social Security Fit? This information is written in connection with the promotion or marketing of the matters addressed in this material. The information cannot be used or relied upon for the purpose of avoiding IRS penalties. These materials are not intended to provide tax, accounting or legal advice. As with all matters of a tax or legal nature, you should consult your own tax or legal counsel for advice.

Challenges: Fewer people working for each person collecting People retiring earlier Longer life expectancies, more centenarians Benefits: Consistent income for life Provides cost of living adjustments (COLAs) Government is helping to ensure citizens have some income in later years What do we know about Social Security? The first monthly payment was paid to Ida May Fuller of Ludlow, VT on 1/31/1940. From 1937- 1939 she paid in a total of $24.75. Her first check was for $22.54. She lived to age 100 and collected $22,888in benefits.* *Source: http://www.ssa.gov/history/idapayroll.html

What will happen to Social Security? “Without changes, in 2037 the Social Security Trust Fund will be able to pay only about 78 cents for each dollar of scheduled benefits.”* -Michael J. Astrue, Commissioner, Social Security Administration, 2010 *These estimates are based on the intermediate assumptions from “A Summary of the 2012 Annual Reports,” www.ssa.gov.

Average monthly payments: Retired worker = $1,294 Retired couple = $2,111 What can you expect? Income of Americans Age 65+1 For 2014:2 Maximum monthly Social Security retirement payment to someone retiring at age 66 is $2,642 1Source: Fast Facts and Figures About Social Security, 2013 2www..ssa.gov

How much will your benefit be? Source: www.ssa.gov04/13

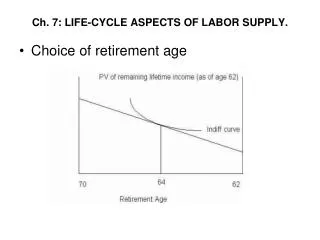

Early benefits Reduction in payments if benefits taken prior to Full Retirement Age Full Retirement Age (FRA) Full benefit available under Social Security guidelines Varies from age 65-67 depending on birth year 3. Delayed benefits Benefits will be increased by percentage (typically 7-8%) until age 70 When should you take benefits? Example: Hypothetical payments for a worker currently earning $37,000 and who has worked a full career. Source: Social Security online callculator, 2013

What about your spouse? Your spouse: • Is eligible for benefits as early as age 62 • Can receive an amount equal to the greater of: • His or her own benefit, or • Up to 50% of your benefit at FRA (“spousal benefit”) • May not collect on your benefit until you have filed for your benefit Your ex-spouse may be eligible if: • You are both age 62 or older • You were married for 10+ years • You’ve been divorced for 2+ years • He or she is not remarried

You can collect 100% of your spouse’s benefit at your FRA, or a reduced benefit as early as age 60. Or, you will receive your benefit, if higher, and you are of age to collect benefits. No survivor benefits paid if you remarry before age 60. If you care for children who are under 16 or disabled, you may apply for survivor benefits at any age. Your unmarried children younger than age 18, and attending school full time, or disabled before age 22, can also receive benefits. My spouse passed away.

Benefit Reductions (2014):* Prior to FRA Benefit reduced $1 for each $2 above $15,480 in earned income Year you reach FRA Benefits reduced $1 for each $3 above $41,400 in earned income Month you reach FRA & on Unlimited earned income No reduction in benefits What if you work? *If benefits are reduced you won’t receive any benefits for the year until Social Security has withheld the amount of the reduction; then you will receive regular monthly checks for the remainder of the year.

A Quick Way to Check if Your Benefits May be Taxable Adjusted Gross Income + ½ Social Security benefits + Non-taxable interest Benefits may be taxable based on the amount of “Combined Income” Combined Income • Non-taxable interest includes: • Tax-exempt interest (municipal bonds) • Interest on qualified U.S. Bonds (typically excluded from income) Qualified Roth IRA withdrawals may not be included. Talk to your tax advisor about all tax-related concerns.

How much is taxable? Combined Income (2014)Percent Taxed Less than $25,000 ($32,000 married filing jointly) Zero $25,000 - $34,000 ($32,000 - $44,000 married filing jointly) Up to 50% Over $34,000 ($44,000 married filing jointly) Up to 85% • Possible ways to reduce “Combined Income” • Reduce adjusted gross income (AGI) • Replace currently taxable assets with tax-deferred assets, to reduce the amount of taxable income in a year • Take qualified Roth IRA distributions, rather than Traditional IRA distributions, as they are not taxable and typically not included in combined income1 • Use permanent life Insurance loans/withdrawals as a source of income, as they are generally not taxable and not included in combined income2 1 Taxable distributions (including certain deemed distributions) are subject to ordinary income tax and if made prior to age 59½, may also be subject to a 10% Federal income tax penalty. 2 Both loans and withdrawals from a permanent life insurance policy may be subject to penalties and fees and, along with any accrued loan interest, will reduce the policy’s death benefit. Assuming a policy is not a Modified Endowment Contract (MEC), withdrawals are taxed only to the extent that they exceed the policyowner’s cost basis in the policy and usually loans are free from current federal taxation. A policy loan could result in tax consequences if the policy lapses or is surrendered while a loan is outstanding. Distributions from MECs are subject to federal income tax to the extent of the gain in the policy and taxable distributions are subject to a 10% additional tax prior to age 59½, with certain exceptions.

Two strategies for taking benefits • File & Suspend • Higher-earning spouse files for benefits at FRA, then immediately suspends benefits. • This allows lower-earning spouse to collect spousal benefits while higher earner continues to delay his or her own benefit and earn delayed retirement credits. • Double Dip • Spouse A files for his or her own benefits at FRA or later. • Spouse B files for spousal benefits on Spouse A when eligible to do so. Spouse B then continues to delay his or her own benefit and earn delayed retirement credits. Source: http://www.ssa.gov/retire2/applying6.htm#options

Questions to ask when taking benefits • When do you plan to stop working? • Do you need extra income? • Will you take your benefit or spousal benefit? Now or later? • How long will you live? • Will you have to pay taxes?

Where does Social Security fit in your plan? Social Security should be just one part of your overall retirement income plan.

Longevity Inflation Timing & amount of withdrawals Retirement is not the finish line Saving Taking Income The Fact:A portfolio's long-term performance is determined primarily by the distribution of dollars among asset classes -- percentage of savings in stocks, bonds, and cash.1 Asset allocation neither assures a profit nor guarantees against a loss. 1Source: 2004 Ibbotson Associates

At age 65, your probability of living to various ages Age Male Female One Memberof a Couple 80 71% 81% 94% 85 53% 65% 84% 90 34% 44% 63% 95 17% 23% 36% Longer lives Data source: Society of Actuaries Annuity 2000 Mortality tablesLongevity data presented does not reflect mortality from birth statistics available from U.S. Census Bureau.

How do you envision your life in retirement? 2 people 3 meals per day 365 days per year 20 years X $8 per meal $350,400

Inflation adds up Price of other essentials increased during that 10 year period:2 Homeowners insurance: 20%Gasoline: 123% Potatoes: 46%Eggs: 25%Bread: 49% Electricity: 46% Medicare Part B premiums: 79% From (2002–2012): Average annual inflation1 is 2.38% – a 26.6% cumulative increase over 10 years 1 Inflation is defined according to the Consumer Price Index (CPI-U) for all urban consumers. www.bls.gov. Cumulative number is based on rates for December 2003 to December 2013. 2 Source: U.S. Bureau of Labor Statistics, Consumer Price Index (CPI-U for All Urban Consumers, December 2013

Timing is everything $250,000 initial investment Annual Withdrawal: 5% of initial investment, adjusted for inflation Bull Market: Jane begins withdrawals 12/31/1974 Bear Market: John begins withdrawals 12/31/1972 PAST PERFORMANCE IS NOT INDICATIVE OF FUTURE RESULTS. This is for illustrative purposes only and not indicative of any investment. Hypothetical initial value of $250,000. Portfolio: 50% large-company stocks, 50% bonds. Assumes reinvestment of income and no transaction costs or taxes. Stocks—Standard & Poor’s 500® Index is a market capitalization weighted price index composed of 500 widely-held U.S. common stocks, frequently used as a measure of U.S. stock market performance. Bonds—Barclays Govtis an index of all publicly issued long-term government debt securities. Average maturity of 23-25 years. Jane invested on 12/31/1974 taking annual withdrawals of $12,500, adjusted for inflation and received withdrawals totaling $1,285,882; John invested on 12/31/1972 taking annual withdrawals of $12,500, adjusted for inflation and received withdrawals totaling $491,927. Fees and expenses not included.Indices are unmanaged and unavailable for direct investment. Data source: Thomson Financial Company, 1/14. $3,195,988 $0 2013

What impacts your success? Retirement Expenses Retirement Resources Insurance Life and Health Insurance Long-term Care Insurance Insurance Life/Health Longevity Long-term care Discretionary Mutual Funds Stocks & Bonds Certificates of Deposit (CDs) Discretionary Travel & Recreation Non-Necessity Unexpected Income Needs Basic Social Security Defined Benefit Plans Annuity Income Basic Medications Client Specific Food Housing

What can you do? Analyze your retirement expenses • Basic vs. discretionary expenses Take an inventory • Income vs. expenses Reposition your assets • Asset & product diversification Monitor your income plan

Resources • Social Security Administration • www.socialsecurity.gov1-800-772-1213 • Benefits estimator - online calculator to estimate benefits • Social Security statements • Social Security publications: “Retirement Benefits”, “How Work Affects your Benefits,” and “Survivor Benefits” • “Social Security and Equivalent Railroad Benefits” • IRS Publication 915, www.irs.gov • Taxation of benefits • SS Form 521 (Request for Withdrawal of Application) • Use this form to apply for a suspension of benefits. • AARP: www.aarp.org

“The Hartford” is The Hartford Financial Services Group, Inc. and its subsidiaries, including the issuing companies of the Hartford Life Insurance Company and Hartford Life and Annuity Insurance Company. Investing in a tax-advantaged retirement plan such as an IRA, you will get no additional tax advantage from the variable annuity. Under these circumstances, you should only consider buying a variable annuity if it makes sense because of the annuity's other features, such as lifetime income payments and death benefit protection. These features can be purchased at an additional cost. Variable annuities are long-term investment vehicles designed for retirement purposes and are subject to market fluctuation, investment risk, and possible loss of principal. Withdrawals of earnings are taxable as ordinary income and, if taken prior to age 59½, may be subject to a 10% federal tax penalty. Early withdrawals will reduce the death benefit and cash surrender value. This information is written in connection with the promotion or marketing of the matter(s) addressed in this material. The information cannot be used or relied upon for the purpose of avoiding IRS penalties. These materials are not intended to provide tax, accounting or legal advice. As with all matters of a tax or legal nature, you should consult your own tax or legal counsel for advice. Hartford variable annuities are issued by Hartford Life and Annuity Insurance Company and by Hartford Life Insurance Company and are underwritten and distributed by Hartford Securities Distribution Company, Inc. The Hartford Mutual Funds are underwritten and distributed by Hartford Investment Financial Services, LLC. You should carefully consider the investment objectives, risks, charges, and expenses of Hartford variable annuities and their underlying funds before investing. This and other information can be found in the prospectus for the variable annuity and the prospectuses for the underlying funds, which can be obtained from your investment representative or by calling 800-862-6668. Please read them carefully before you invest or send money. You should carefully consider investment objectives, risks, charges, and expenses of The Hartford Mutual Funds before investing. This and other information can be found in the Fund's prospectus or summary prospectus, which can be obtained from your investment representative or by calling 888-843-7824. Please read them carefully before you invest or send money. This seminar has been funded in whole or in part by Hartford Life Distributors, LLC, a broker dealer affiliate of The Hartford. All information and representations herein are as of 2/11 unless otherwise noted. Disclosures This information is written in connection with the promotion or marketing of the matter(s) addressed in this material. The information cannot be used or relied upon for the purpose of avoiding IRS penalties. These materials are not intended to provide tax, accounting or legal advice. As with all matters of a tax or legal nature, you should consult your own tax or legal counsel for advice. Investors should carefully consider the investment objectives, risks, charges, and expenses of Hartford Funds before investing. This and other information can be found in the prospectus and summary prospectus, which can be obtained by calling 888-843-7824 (retail) or 877-836-5854 (institutional). Investors should read them carefully before they invest. Hartford Funds are underwritten and distributed by Hartford Funds Distributors, LLC. This seminar has been funded in whole or in part by Hartford Funds Distributors, LLC. SEM_SS_0214 107750-3