Download

1 / 20

200 likes | 296 Vues

How Financial Aid Works And How It Makes College Affordable for You. In a Nutshell. The financial aid system is based on the goal of equal access— that anyone should be able to attend college, regardless of financial circumstances . . In a Nutshell. Here's how the system works:

E N D

How Financial Aid WorksAnd How It Makes College Affordable for You

In a Nutshell The financial aid system is based on the goal of equal access— that anyone should be able to attend college, regardless of financial circumstances.

In a Nutshell Here's how the system works: • Students and their families are expected to contribute to the cost of college to the extent that they're able. • If a family is unable to contribute the entire cost, financial aid is available to bridge the gap.

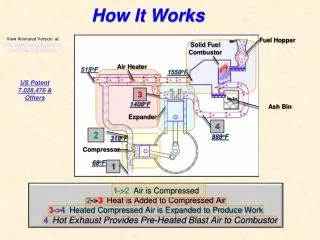

$50,000 $5,000 How Financial Aid Works: Cost of College Financial Aid Expected Family Contribution

Don't Rule Out Colleges with Higher Costs • Say your EFC is $5,000. At a college with a total cost of $8,000, you'd be eligible for up to $3,000 in financial aid. At a college with a total cost of $25,000, you'd be eligible for up to $20,000 in aid. In other words, your family would be asked to contribute the same amount at both colleges.

Who Decides How Much My Family Is Able to Contribute? • Expected Family Contribution, or EFC. The amount is determined by whomever is awarding the aid—usually the federal government or individual colleges and universities. • The federal government and financial aid offices use formulas that analyze your family's financial circumstances (things like income, assets, and family size) and compare them proportionally with other families' financial circumstances.

This is your financial aid http://economix.blogs.nytimes.com/2010/08/23/how-americans-pay-for-college/

Summer before Senior Year: Request College Applications and get financial info together FALL of Senior Year: Fill out and submit college applications BEFORE deadlines hit JAN-FEB of Senior Year: File FAFSA (deadline is usually Feb 1). You’ll need your parents tax forms, so may sure they will them out!!!

READ your SAR (Student Aid Report) What does it tell you? • FAFSA Info.The information you provided on your FAFSA will be listed on your SAR. Review this section carefully to make sure all the information is correct. If you find any errors, you can make corrections • Estimated Family Contribution (EFC). The amount the government believes your family is able to contribute to college expenses. This number is based on information that you supplied on your FAFSA such as family income, assets, number of children in college, etc. • Verification. If there is an asterisk next to your EFC, this means that your SAR has been selected for verification. Verification is a process used to verify the accuracy of information provided on your FAFSA. • Next Step. The schools you listed on FAFSA will receive your SAR information electronically. The financial aid office staff at your school(s) will use this information to determine if you are eligible for financial aid and put together an award package for you • Step 2:

Step 3: Compare “Packages” from Colleges • (March-April)

GRANTS SCHOLARSHIPS Look around, there are scholarships for everyone! Remember to fill out the Local Hamburg Scholarship form And check out… • FEDERAL PELL GRANT (based on need, up to $5,550) • STATE GRANTS (TAP) • COLLEGE GRANTS http://www.fastweb.com/

CHECK YOUR UNDERSTANDING: • What is the purpose of the FAFSA? • Will your expected family contribution (EFC) amount be different if you choose a more or less expensive college? • What is a “Financial Aid Award?” • What THREE things make up Financial Aid? • To determine your expected family contribution • No – your family is expected to pay a certain amount, no more • A letter from a college you were accepted at, outlining the financial aid you qualify for if you choose to go to that school. • Grants/Scholarships, Work Study, Student Loans

Step 4: Choose College, let them know (May), and begin loan process

TYPESOF LOANS FEDERAL PERKINS LOAN • Awarded by college to students with a lot of need • Fixed 5% interest rate with no fees • Repayment begins 9 months after graduation • Subsidized – government pays the interest on the loan when you are in school

TYPESOF LOANS FEDERAL STAFFORD LOAN • Subsidized and unsubsidized • Subsidized: need based • Unsubsidized: not need based

TYPESOF LOANS FEDERAL PARENT PLUS LOAN • Unsubsidized loan for parents to take out • Fixed 7.9% interest rate with 4% fees PRIVATE STUDENT LOANS • Made by Credit Unions and Banks • Interest rate is based on credit worthiness (3-10%) • Most have fees associated with them

Paying Back Your LOANS • Payment will probably begin 6-9 months after you graduate • The payments will be the same each month for the term (usually 10 years) • If you're having trouble making payments on your loans, contact your loan servicer as soon as possible. Options include: • Changing repayment plans. • Deferment—(temporarily stop making payments) • Forbearance – (temp stop, or make smaller pmts)

DON’T DEFAULT! • Your credit rating will go down, making it hard to buy a car or a house. • You will be ineligible for additional federal student aid if you decide to return to school. • Loan payments can be deducted from your paycheck. • State and federal income tax refunds can be withheld and applied toward the amount you owe. • You will have to pay late fees and collection costs on top of what you already owe • You can be sued.