Download

1 / 3

30 likes | 103 Vues

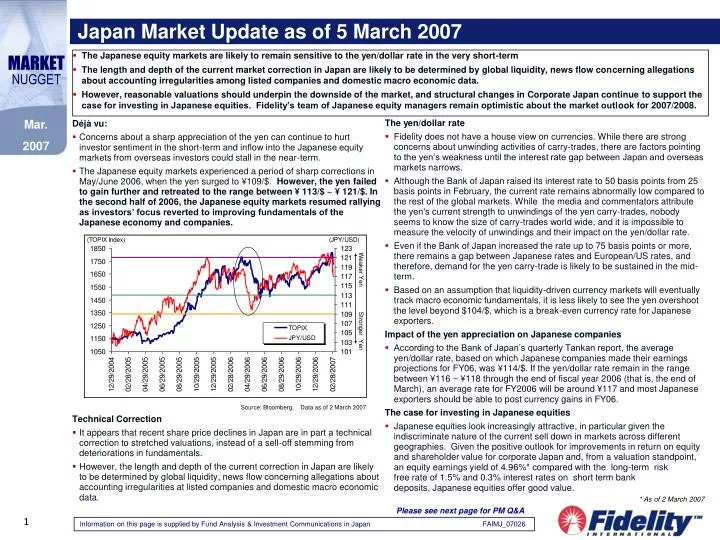

Japan Market Update as of 5 March 2007. The Japanese equity markets are likely to remain sensitive to the yen/dollar rate in the very short-term

E N D

Japan Market Update as of 5 March 2007 • The Japanese equity markets are likely to remain sensitive to the yen/dollar rate in the very short-term • The length and depth of the current market correction in Japan are likely to be determined by global liquidity, news flow concerning allegations about accounting irregularities among listed companies and domestic macro economic data. • However, reasonable valuations should underpin the downside of the market, and structural changes in Corporate Japan continue to support the case for investing in Japanese equities. Fidelity’s team of Japanese equity managers remain optimistic about the market outlook for 2007/2008. MARKETNUGGET Déjà vu: • Concerns about a sharp appreciation of the yen can continue to hurt investor sentiment in the short-term and inflow into the Japanese equity markets from overseas investors could stall in the near-term. • The Japanese equity markets experienced a period of sharp corrections in May/June 2006, when the yen surged to ¥109/$. However, the yen failed to gain further and retreated to the range between ¥ 113/$ ~ ¥ 121/$. In the second half of 2006, the Japanese equity markets resumed rallying as investors’ focus reverted to improving fundamentals of the Japanese economy and companies. Technical Correction • It appears that recent share price declines in Japan are in part a technical correction to stretched valuations, instead of a sell-off stemming from deteriorations in fundamentals. • However, the length and depth of the current correction in Japan are likely to be determined by global liquidity, news flow concerning allegations about accounting irregularities at listed companies and domestic macro economic data. Mar. 2007 The yen/dollar rate • Fidelity does not have a house view on currencies. While there are strong concerns about unwinding activities of carry-trades, there are factors pointing to the yen’s weakness until the interest rate gap between Japan and overseas markets narrows. • Although the Bank of Japan raised its interest rate to 50 basis points from 25 basis points in February, the current rate remains abnormally low compared to the rest of the global markets. While the media and commentators attribute the yen's current strength to unwindings of the yen carry-trades, nobody seems to know the size of carry-trades world wide, and it is impossible to measure the velocity of unwindings and their impact on the yen/dollar rate. • Even if the Bank of Japan increased the rate up to 75 basis points or more, there remains a gap between Japanese rates and European/US rates, and therefore, demand for the yen carry-trade is likely to be sustained in the mid-term. • Based on an assumption that liquidity-driven currency markets will eventually track macro economic fundamentals, it is less likely to see the yen overshoot the level beyond $104/$, which is a break-even currency rate for Japanese exporters. Impact of the yen appreciation on Japanese companies • According to the Bank of Japan’s quarterly Tankan report, the average yen/dollar rate, based on which Japanese companies made their earnings projections for FY06, was ¥114/$. If the yen/dollar rate remain in the range between ¥116 ~ ¥118 through the end of fiscal year 2006 (that is, the end of March), an average rate for FY2006 will be around ¥117 and most Japanese exporters should be able to post currency gains in FY06. The case for investing in Japanese equities • Japanese equities look increasingly attractive, in particular given the indiscriminate nature of the current sell down in markets across different geographies. Given the positive outlook for improvements in return on equity and shareholder value for corporate Japan and, from a valuation standpoint, an equity earnings yield of 4.96%* compared with the long-term risk free rate of 1.5% and 0.3% interest rates on short term bank deposits, Japanese equities offer good value. * As of 2 March 2007 Please see next page for PM Q&A Source: Bloomberg, Data as of 2 March 2007

Portfolio Manager Q&A MARKETNUGGET Q&A with our Portfolio Managers, Robert Rowland (managing FF Japan Fund) and Jun Tano (managing FF Japan Smaller Co’s Fund) • Robert, What is your funds’ exposure to exporters? • Robert Rowland: Roughly speaking, the current portfolio has equal weights in domestically focused companies and in exporters. However, this is not a result of conscious decisions. I do not divide my investment universe in two camps between exporters and domestic companies. • How is your fund performing? • Robert Rowland: After the outperformance in Q4 06, the fund has been underperforming for the year to date*. Large cap exporters in the fund’s top-ten holdings, which contributed to the performance in Q4 06, have detracted from relative returns for the year to date. These included major banking groups and technology exporters. Roughly about a half of the fund’s underperformance stemmed from disappointing share price performances of individual holdings in the electrical machinery sectors. • Have you made any changes to the portfolio in recent weeks? • Robert Rowland: It was widely expected that any sudden surge of the yen against the dollar could hurt investor sentiment towards exporters. However, I have not changed the portfolio positioning, as I am keeping my conviction in earnings growth potential of companies the fund invests in. I still believe the fund’s key stock selection themes – “reflation”, “capital spending”, “attractive valuations among global technology manufacturers” are valid, while I also look for investment opportunities in companies that offer relatively high dividend yield. • Jun, Do you think the recent market corrections mark the end of the large cap outperformance and that the yen appreciation signals the beginning of a small cap recovery? • Jun Tano: It is too early to say so. Valuations of small cap stocks are no longer stretched, therefore the downside may be limited. However, small cap stocks are still overvalued compared against large cap stocks. Furthermore, as investors’ appetite for risk has diminished substantially amid the recent global market corrections, it may take a while until investor sentiment recovers. • How is your fund performing? • Jun Tano: The fund has been underperforming the Russell/Nomura mid-small cap index since I inherited the portfolio from my predecessor in April last year. The more recent underperformance* is largely due to share price declines of some of the fund’s largest holdings whose earnings growth slowed down in Q3 06. Stock selection has been particularly disappointing in the electrical machinery, retail and information & communication sectors. • Where do you see opportunities in the current market environment? • Jun Tano: In the mid/small cap stock markets, we look for oversold names with better earnings visibility over the next 12 to 18 months. There are a number of technology manufacturers whose valuations look increasingly attractive due to recent share price declines. As capital spending in IT infrastructure development and support is increasing, companies that provide software and business support offer attractive growth prospects over the mid-term. We also look for special situations, which are bound to reap the fruit of corporate restructuring efforts and/or industry consolidations. Mar. 2007 * Performance for the year to 28/02/2007 Source: Fidelity International, Bloomberg, **Data as of 28 February 2007 Source: Fidelity International, Bloomberg, **Data as of 28 February 2007

Important Information For Professional Investors only – Not for public distribution MARKETNUGGET • Fidelity Funds is an open-ended Luxembourg based investment company. • We recommend that you obtain detailed information before making any investment decision. Investments in the Fidelity Funds should be made on the basis of the current prospectus, which is available along with the current annual and semi-annual reports free of charge from our distributors, from our European Service Centre in Luxembourg and from your financial advisor or from the branch of your bank. • Fidelity only gives information on its products and does not provide investment advice based on individual circumstances. • Past performance is no guide to the future. The value of investments and any income from them may go down as well as up and an investor may not get back the amount invested. An investment in a currency other than the shareholder’s own will be subject to the movements of foreign exchange rates. Foreign exchange transactions are effected through a Fidelity associated company at rates determined in aggregate with other transactions from which a benefit may be derived by the associated company. • Unless otherwise stated, all views expressed are those of the Fidelity organisation. This presentation may not be reproduced or circulated without prior permission and should not be passed in whole or in part to private investors. • Reference in this document to specific companies held within an investment fund should not be construed as a recommendation to buy or sell the same, but is included only for the purposes of illustration. • This communication is not directed at, and must not be acted upon by persons inside the United Kingdom and the United States and is otherwise only directed at persons residing in jurisdictions where the relevant funds are authorised for distribution or where no such authorisation is required. • Resources include those of Fidelity International Limited (FIL) established in Bermuda, its subsidiary companies and those of its US affiliate FMR. Fidelity means Fidelity International Limited (FIL), established in Bermuda, and its subsidiary companies. • Fidelity, Fidelity International and Fidelity Investments and Pyramid Logo are trademarks of Fidelity International Limited • Issued by Fidelity Investments International, regulated by the Financial Services Authority in the UK. • Registered office: Oakhill House, 130 Tonbridge Road, Hildenborough, Kent TN11 9DZ. CB30432/na Mar. 2007