Download

1 / 45

480 likes | 781 Vues

GLOBAL RECESSION AND IMPACT ON INDIA. Group 5. Shailendra singh N61 Shailendra singh N62 Subhash Kumar N63 Shweta Malik N66 Virender Singh N69 Virender Kumar N68 Sumeet Hans N64 Saumitro Ba nerjee N57 Sourabh Diddi N71. SCHEME OF PRESENTATION.

E N D

Group 5 Shailendrasingh N61 Shailendrasingh N62 Subhash Kumar N63 ShwetaMalik N66 Virender Singh N69 Virender Kumar N68 Sumeet Hans N64 SaumitroBanerjee N57 SourabhDiddi N71

WhatisRecession In economics, a recession is a general slowdown in economic activity over a long period of time, or a business cycle contraction.[1][2] During recessions, many macroeconomic indicators vary in a similar way. Production as measured by Gross Domestic Product (GDP), employment, investment spending, capacity utilization, household incomes, business profits and inflation all fall during recessions; bankruptcies and the unemployment rate rises

Predictors of Recession • In the US a significant stock market drop has often preceded the beginning of a recession • Inverted yield curve,the model developed by economist Jonathan H. Wright, uses yields on 10-year and three-month Treasury securities as well as the Fed's overnight funds rate • The three-month change in the unemployment rate and initial jobless claims • Lowering of Home Prices. Lowering of home prices or value, too much personal debts.

Government Responses • Most mainstream economists believe that recessions are caused by inadequate aggregate demand in the economy, and favor the use of expansionary macroeconomic policy during recessions. Strategies favored for moving an economy out of a recession vary depending on which economic school the policymakers follow. Monetarists would favour the use of expansionary monetary policy, while Keynesian economists may advocate increased government spending to spark economic growth. Supply-side economists may suggest tax cuts to promote business capital investment. Laissez-faire minded economists may simply recommend that the government not interfere with natural market forces.

Recessions bring anxiety and fear, not to mention financial disaster for many.

The 2008 recession had global effects. An Indian stock dealer copes with news that Indian share prices fell 6 percent.

Problems began when the subprime mortgage industry collapsed in late 2007.

Indymac was the first of many banks to close its doors. The real estate collapse affected the banking industry that provided mortgage loans, and before long, bank closings took over the headlines. As credit dried up and new construction slowed, unemployment rates spiked.

Some economists define a recession as two consecutive quarters in which the gross domestic product (GDP) decreases. Unemployment often rises as this occurs. And when people are unemployed, they're unable to pay their debts.

Many consumers felt trapped by credit card companies, who raised interest rates and lowered credit limits.

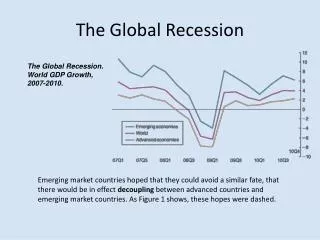

Impact on Capital Market Index Movement in last one year

ACTION BY CENTRAL BANK • Cash Reserve Ratio brought down to 5% in January 2009 from 9% (September 2008) injecting Rs. 1600 billion in primary liquidity. • Statutory liquidity ratios brought down, opening of refinance windows, refines to SIDBI and EXIM banks • Repo and Reverse Repo rates are cut down from 9% to 4.75% and 6% to 3.25% respectively. • MSS operations were reversed Balance Rs. 860 billion end March 2009 against Rs. 1754 billion at May 2007.

Various monitory and liquid measures released liquidity of Rs. 4900 Billion since mid September 2008 (about 9% GDP) • Banks were advised to step up lending to core sectors. • Banks were advised to bring down BPLR. • Restriction on interest rate to bulk deposits. • Restrictions loosened on External commercial borrowing by corporates.

STRENGTH OF INDIAN FINANCIAL SECTOR • Full but gradual opening of current account. • Foreign investment flows are encouraged. • External commercial borrowing is subject to ceiling and end – use restrictions. • Macro ceiling stipulated on portfolio investment in Govt. Securities and Corporate Bonds by FIIs. • Imposition of prudential limits on Banks, such as inter-bank liabilities, borrowing and lending, money market, assets - liability Management for both on and off balance sheet terms.

Implementation of Based II ……. Minimum 9% CRAR. • CRAR of all scheduled commercial banks at 13% at end March 2008. • Single factor stress tests reveal that Banks can withstand shocks on account of change in credit quality, interest rates and liquidity conditions. • Strict prudential norms towards income recognition, Asset classifications and provisions by the Banks.

WHY THE INDIAN FINANCIAL SECTOR WEATHERED THE STORM • Negligible direct exposure to toxic assets which contaminated Western Banking System. • Banks credit quality remained high. • Credit Growth apx. 30% during 2004-07. • RBI tightened prudential norms CRR at 13% at March 2008 end against regulatory requirement of 9%. • Net NPA at 1% of net advance and 0.6% of assets. • Better management of financial capitalism. • High saving rate of indian house hold.

PRE-POLL CRITICAL ISSUES • Global Financial crisis. • Razor-thin majority Government. • Melt down in Capital Market. Sensex touching a low of 8160 in April 2009, down from a peak of 20728, a fall of 61%. • Weakening economy. Rising job losses in export sector. • General Election in May 2009. Political Uncertainty • Formation of 4 front – UPA led by Congress, NDA led by BJP, Third Front – led by Left Parties. • No coalition likely to get majority

Lessons From recession • Avoid high volatility in monetary policy • Appropriate response of monetary policy to asset prices • Manage capital flow volatility • Look for signs of over leveraging • Active dynamic financial regulation Capital buffers, dynamic provisioning • Look for regulatory arbitrage incentives/ possibilities