Download

1 / 20

210 likes | 365 Vues

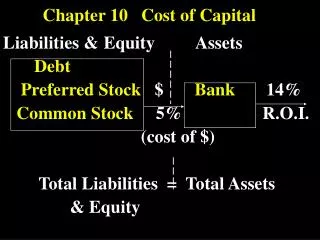

CHAPTER 10 The Cost of Capital. Sources of capital Component costs WACC Adjusting for flotation costs Adjusting for risk. What sources of long-term capital do firms use?. Calculating the weighted average cost of capital. WACC = w d r d (1-T) + w p r p + w c r s

E N D

CHAPTER 10The Cost of Capital Sources of capital Component costs WACC Adjusting for flotation costs Adjusting for risk

Calculating the weighted average cost of capital WACC = wdrd(1-T) + wprp + wcrs • The w’s refer to the firm’s capital structure weights. • The r’s refer to the cost of each component.

Relevant costs of capital • After-tax • Only debt needs tax adjustment • Dividends paid on preferred and common stock not tax-deductible • Marginal cost • Cost of raising the next dollar of funds

Component cost of debt WACC = wdrd(1-T) + wprp + wcrs • rd is the marginal pre-tax cost of debt capital. • The yield to maturity on outstanding bonds is often used to measure rd. • rd(1-T) is the after-tax cost of debt.

A 15-year, 12% semiannual coupon bond sells for $1,153.72. What is the after-tax cost of debt rd(1-T)? • Remember, the bond pays a semiannual coupon, so rd = 5.0% × 2 = 10%. • Interest is tax deductible, so rd (1-T) = 10% (1 - 0.40) = 6% INPUTS 30 -1153.72 60 1000 N I/YR PV PMT FV OUTPUT 5

Component cost of preferred stock WACC = wdrd(1-T) + wprp + wcrs • rp is the marginal cost of preferred stock, which is the return investors require on the firm’s preferred stock. rp = Dp / Pp = $10 / $111.10 = 9%

Component cost of equity WACC = wdrd(1-T) + wprp + wcrs • rs is the marginal cost of common equity using retained earnings. • re is the marginal cost of issuing new common stock.

Why is there a cost for retained earnings? • Earnings can be reinvested or paid out as dividends. • If earnings are retained, there is an opportunity cost. • Investors could buy similar stocks and earn rs.

Three ways to determine the cost of common equity, rs • CAPM: rs = rRF + (rM – rRF) s • DCF: rs = (D1 / P0) + g • Own-Bond-Yield-Plus-Risk-Premium: rs = rd + RP

If the rRF = 7%, RPM = 6%, and the firm’s beta is 1.2, what’s the cost of common equity based upon the CAPM? rs = rRF + (rM – rRF) s = rRF + (RPM) s = 7% + (6%)1.2 = 14.2%

If D0 = $4.19, P0 = $50, and g = 5%, what is the cost of common equity based on the DCF approach? D1 = D0 (1 + g) D1 = $4.19 (1 + .05) D1 = $4.3995 rs = (D1 / P0) + g = ($4.3995 / $50) + 0.05 = 13.8%

Estimating the future growth rate • The firm has been earning 15% on equity (ROE = 15%) and retaining 35% of its earnings (dividend payout = 65%). This situation is expected to continue. g = (1 – Payout ratio) (ROE) = (Retention ratio) (ROE) = (0.35) (15%) = 5.25%

If rd = 10% and RP = 4%, what is rs using the own-bond-yield-plus-risk-premium method? • This method produces a ballpark estimate of rs, and can serve as a useful check. rs = rd + RP = 10% + 4% = 14% • This RP is not the same as the CAPM RPM.

What is a reasonable final estimate of rs? MethodEstimate CAPM 14.2% DCF 13.8% rd + RP 14.0% Average 14.0%

If issuing new common stock incurs a flotation cost of 15% of the proceeds, what is re?

Why is the cost of retained earnings (rs) cheaper than the cost of issuing new common stock (re)? • When a company issues new common stock they also have to pay flotation costs to the underwriter. • Issuing new common stock may send a negative signal to the capital markets, which may depress the stock price.

Ignoring flotation costs, what is the firm’s WACC? WACC = wdrd(1-T) + wprp + wcrs = 0.3(10%)(0.6) + 0.1(9%) + 0.6(14%) = 1.8% + 0.9% + 8.4% = 11.1%

What factors influence a company’s WACC? • Interest rates • Tax rates • Investment policy • Dividend policy • Capital structure

Should the company use the composite WACC as the hurdle rate for each of its projects? • No. The WACC reflects the risk of an average project undertaken by the firm. Therefore, the WACC only represents the “hurdle rate” for a typical project with average risk. • Different projects have different risks. The project’s WACC should be adjusted to reflect the project’s risk.