Download

1 / 18

180 likes | 275 Vues

Swaps Chapter 7 (all editions) Sections 7.1 and 7.4 only. 7.1 Nature of Swaps. A swap is an agreement between two companies to exchange cash flows at specified future times according to certain specified rules

E N D

7.1 Nature of Swaps • A swap is an agreement between two companies to exchange cash flows at specified future times according to certain specified rules • Calculation of cash flows involves the future value of an interest rate, exchange rate or other market variable • Most popular is the plain vanilla swap (fixed-for-floating).

Notional Principal • Definition: The amount upon which the interest payments in an interest-rate swap are based; in other words, it is the nominal value used to calculate the cash flows on swaps • Notional Principal itself is not exchanged

LIBOR • LIBOR, or London Interbank Offer Rate, is the interest rate offered among international banks in London on the eurodollars • Eurodollars: U.S.-dollar denominated deposits at foreign banks or foreign branches of American banks • The market for interest rate swaps frequently (but not always) uses LIBOR as the base for the floating rate.

An Example of a “Plain Vanilla” Interest Rate Swap • A 3 year swap initiated on March 5, 2001 between Microsoft and Intel • Microsoft agrees to pay to Intel an interest rate of 5% p.a. on a notional principal of $100 million • Intel agrees to pay Microsoft the 6-month LIBOR rate on the same notional principal • Agreement specifies that payments are to be exchanged every six months and the 5% rate is quoted with semiannual compounding • Next slide illustrates cash flows

---------Millions of Dollars--------- LIBOR FLOATING FIXED Net Date Rate Cash Flow Cash Flow Cash Flow Mar.5, 2001 4.2% Sept. 5, 2001 4.8% +2.10 –2.50 –0.40 Mar.5, 2002 5.3% +2.40 –2.50 –0.10 Sept. 5, 2002 5.5% +2.65 –2.50 +0.15 Mar.5, 2003 5.6% +2.75 –2.50 +0.25 Sept. 5, 2003 5.9% +2.80 –2.50 +0.30 Mar.5, 2004 6.4% +2.95 –2.50 +0.45 Cash Flows to Microsoft

Converting a liability from fixed rate to floating rate floating rate to fixed rate Converting an investment from fixed rate to floating rate floating rate to fixed rate Typical Uses of anInterest Rate Swap

Converting a liability from floating rate to fixed rate Eg. Microsoft has arranged to borrow $100 million at LIBOR plus 10 basis points (LIBOR + 0.10%) With a swap, Microsoft: Pays LIBOR plus 0.1% Receives LIBOR under the swap agreement Pays 5% fixed under the swap agreement Net is that Microsoft pays 5.1% Liability

Converting a liability from fixed rate to floating rate Eg. Intel has arranged to borrow $100 million at 5.2% fixed With a swap, Intel: Pays 5.2% Receives 5% under the swap agreement Pays LIBOR under the swap agreement Net is that Intel pays LIBOR + 0.2% Liability cont’d

Intel and Microsoft Transform a Liability 5% 5.2% Intel MS LIBOR+0.1% LIBOR

Financial Intermediary-usually gets 3 or 4 basis points 4.985% 5.015% 5.2% Intel F.I. MS LIBOR+0.1% LIBOR LIBOR Microsoft (MS) ends up borrowing at 5.115% and Intel ends up borrowing at LIBOR + 0.215%

7.4 The Comparative Advantage Argument • Swaps originated because of a phenomenon known as comparative advantage. • This means that different companies are able to raise capital at different rates in different markets • For example, one company may be able to enter into fixed-rate loans at more advantageous rates than another • Similarly, a company may enjoy a relationship with the floating rate market, able to raise capital more cheaply than other companies

The Comparative Advantage Argument cont’d • US: $10 to produce one gun and $1 to produce one paperweight • New Zealand: $15 dollars to produce one gun and $5 to produce one paperweight • US has an absolute advantage in the production of both guns and paperweights; however, New Zealand has a comparative advantage in gun production • It costs New Zealand three paperweights to produce one gun; it costs the US ten paperweights to produce one gun. • US has a comparative advantage in paperweight production because it costs the US 0.1 guns to produce one paperweight while it costs New Zealand 0.3 guns • the US should only produce paperweights and New Zealand should only produce guns, assuming they are both willing to trade freely, and they will both come out ahead, getting more goods at a lower cost.

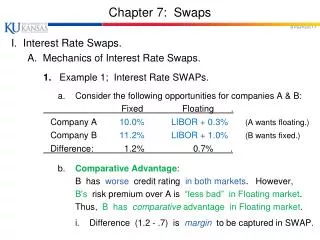

Fixed Floating AAACorp 10.00% 6-month LIBOR + 0.30% BBBCorp 11.20% 6-month LIBOR + 1.00% 7.4 The Comparative Advantage Argument – swap example • AAACorp wants to borrow floating • BBBCorp wants to borrow fixed • AAACorp has a comparative advantage in the fixed rate market and borrows at 10.00% • BBBCorp has a comparative advantage in the floating rate market and borrows at LIBOR + 1.00% • They enter into a swap to ensure they each borrow in the desired market

The Swap 9.95% 10% AAA BBB LIBOR+1% LIBOR • Net effect: • AAACorp borrows at LIBOR + 0.05% • BBBCorp borrows at 10.95%

The Swap when a Financial Institution is Involved 9.93% 9.97% 10% AAA F.I. BBB LIBOR+1% LIBOR LIBOR • Net effect: • AAACorp borrows at LIBOR + 0.07% • BBBCorp borrows at 10.97% • Financial instituation gains 0.04% or 4 basis points

Criticism of the Comparative Advantage Argument • Why should the spread between the rates offered to AAACorp and BBBCorp be different in fixed and floating markets? • Floating: both corporations have little chance of default in the next 6 months • BBBCorp (low credit rating) has a higher probability to default on the five-year fixed rate • Therefore, greater spread on the fixed rates than on floating rates

Questions • All editions: 7.1, 7.7, 7.9