Download

1 / 0

0 likes | 81 Vues

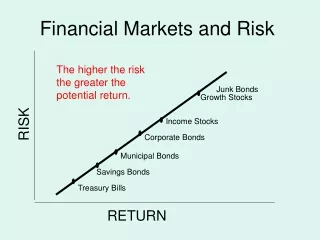

Risk in Financial Markets The Prime Directive versus Sharks. 21 June 2011. Rodney N. Sullivan, CFA Head, Publications and Editor, Financial Analysts Journal. Risk in Financial Markets. The Prime Directive versus Sharks. “ Forecasting is difficult,

E N D

![The Markets in Financial Instruments Directive [ MiFID ]](https://cdn3.slideserve.com/6718874/the-markets-in-financial-instruments-directive-mifid-dt.jpg)