Download

1 / 18

320 likes | 748 Vues

PART 1. INTRODUCTION TO DOUBLE ENTRY BOOKKEEPING. The Accounting Equation and Balance Sheet The Double Entry System for asset, liabilities and capital Inventory The effect of profit and loss on capital and the Double Entry System for expenses and revenues Balancing off the accounts

E N D

PART1 INTRODUCTION TO DOUBLE ENTRY BOOKKEEPING • The Accounting Equation and Balance Sheet • The Double Entry System for asset, liabilities and capital • Inventory • The effect of profit and loss on capital and the Double Entry System for expenses and revenues • Balancing off the accounts • The trial balance P1 Prepared by: Miss Syarifah Fairuz Binti Syed Radzuan PPIPT,UniMAP

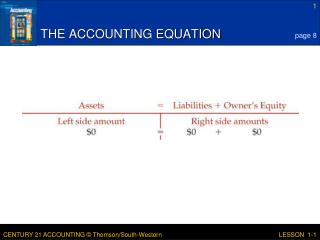

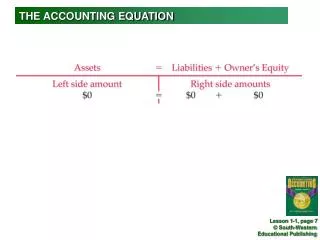

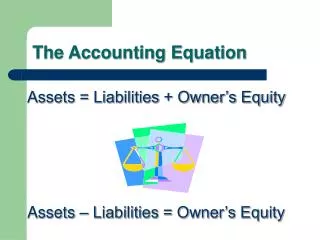

Chapter1 The Accounting Equation and the Balance Sheet Learning Objectives • What is accounting? • History of accounting • Relationship between bookkeeping and accounting • The main users of accounting information and what accounting information they interested in • Accounting Equation • Relationship between the Accounting Equation and the layout of the Balance Sheet • Terms Asset, Capital, Liabilities, Accounts Receivables (debtors) and Creditors Accounts Payables (creditors) • Accounting transaction affects the items in the accounting equation P1 Prepared by: Miss Syarifah Fairuz Binti Syed Radzuan PPIPT,UniMAP

1. What is Accounting? • Accounting as a business language because it is a general systemto communicate important information to the manager or administrator to make business decision. Prepared by: Miss Syarifah Fairuz Binti Syed Radzuan PPIPT,UniMAP

1. What is Accounting? (cont..) • Accounting involved with the process of identifying, classifying, measuring, recording and summarizing of transactions and business events in monetary terms, and interpreting the results to the interested parties (users of accounting information) to enable them to make decision. Prepared by: Miss Syarifah Fairuz Binti Syed Radzuan PPIPT,UniMAP

1. What is Accounting? (cont..) • Accounting involved with the process of identifying, classifying, measuring, recording and summarizing of transactions and business events in monetary terms, and interpreting the results to the interested parties (users of accounting information) to enable them to make decision. Prepared by: Miss Syarifah Fairuz Binti Syed Radzuan PPIPT,UniMAP

1. What is Accounting? (cont..) Major purposes of accounting: • As an evidence that the transaction have been taken place • To identifying, classifying, measuring, recording and summarizing all transactions in monetary terms • To analyze and interpret the business transactions based on the financial report to make decision Prepared by: Miss Syarifah Fairuz Binti Syed Radzuan PPIPT,UniMAP

2. The History of Accounting Accounting began because people needed to : • Record business transactions • Know if they were being financially successful • Know how much they owned and how much they owed Prepared by: Miss Syarifah Fairuz Binti Syed Radzuan PPIPT,UniMAP

2. The History of Accounting (cont..) Italian Book Keeping: • Luca Bartolomes Pacioli (1494), who wrote a mathematical treatise containing 36 chapters on accounting. • Luca Pacioli wrote about keeping track of debits and credits in two separate columns, with the aim of making sure both columns always tailed, so all monies would be accounted for. Prepared by: Miss Syarifah Fairuz Binti Syed Radzuan PPIPT,UniMAP

3. The relationship between Bookkeeping and Accounting • Until about 100 years ago all accounting data was kept by being recorded manually in books, so the part of accounting that is concerned with recording data if often known as BOOKKEEPING • Nowadays although handwritten books may be used (particularly by smaller organizations)most accounting data is recorded electronically and stored electronically using computers • Bookkeeping is the process of recording data relating to accounting transactions in the accounting books Prepared by: Miss Syarifah Fairuz Binti Syed Radzuan PPIPT,UniMAP

4. Users of Accounting Information Prepared by: Miss Syarifah Fairuz Binti Syed Radzuan PPIPT,UniMAP

Users of Accounting Information • investors • creditors • regulators • customers • competitors Financial Accounting • owners • managers • employees EXTERNAL USERS ManagerialAccounting INTERNAL USERS Prepared by: Miss Syarifah Fairuz Binti Syed Radzuan PPIPT,UniMAP

Internal Users: Those individuals inside a company who plan, organize and run the business. Example: Owners interested in profits earned, financial stability and business growth Managers need accounting information to guide it in business planning, organizing and control Employees interested in business stabilities to know whether the owners can pay increased wages and benefits Prepared by: Miss Syarifah Fairuz Binti Syed Radzuan PPIPT,UniMAP

External Users: Individuals and organization outside a company who wants financial information about the company. Direct financial interest: Investors who use accounting information to make decision to buy, hold or sell the stock Creditors (suppliers/bankers) use accounting information to evaluate the risk of granting credits or lending money Indirect financial interest: Government use accounting information for taxes and others regulatory requirements. Public (customers) interested in whether a company will continue to honor products warranties and support its product line Prepared by: Miss Syarifah Fairuz Binti Syed Radzuan PPIPT,UniMAP

Accounting PRINCIPLES • Going Concern Principle • The assumption from this principle of business is • assumed to run in the longer period. • Business Entity Concept • Business entity concept understood that the owner and • the business are separate entity. • Historical Cost Concept • All assets are recorded at the cost of acquiring them, • adjusted for depreciation where applicable. • 4) Duality Concepts • For every transaction, there must be both a debit and • credit entry and for the same amount. Prepared by: Miss Syarifah Fairuz Binti Syed Radzuan PPIPT,UniMAP

Accounting PRINCIPLES 5) Objectivity All financial information must be reliable and free from bias. The objective evidence can be included some of physical things. eg: bill, cheque, invoice or bank statement. 6) Time Period Principle The financial year or accounting period of the business should be identified clearly in the business. 7) Money Measurement Principle The business transaction recorded only can be measured in term of monetary value or terms of money and also known as quantitative measurement. Prepared by: Miss Syarifah Fairuz Binti Syed Radzuan PPIPT,UniMAP

Forms of Businesses • Sole Proprietorship – business with single or sole owner, who most often is also the manager of the business. • Partnership – business organization that is made up of two or more individuals or owners, who jointly own the business. • Companies – organizations which have many owners called shareholders or stockholders. Prepared by: Miss Syarifah Fairuz Binti Syed Radzuan PPIPT,UniMAP

Forms of Businesses (cont..) There are EIGHT (8) business characteristics that can be identified, which are: • Ownership • Capital contribution • Control and management • Business establishment • Division of profit • Liability • Tax payment • Documents and financial statements Prepared by: Miss Syarifah Fairuz Binti Syed Radzuan PPIPT,UniMAP

End of Chapter 1 If a problem has no solution, it may not be a problem, but a fact – not to be solved, but to be coped with over time – Shimon Peres Prepared by: Miss Syarifah Fairuz Binti Syed Radzuan PPIPT,UniMAP