Download

1 / 17

170 likes | 393 Vues

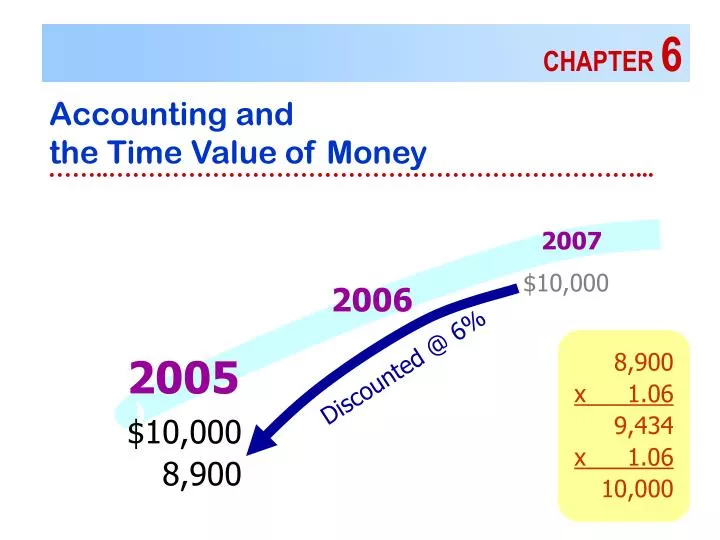

2007. 2006. 2005. Discounted @ 6%. CHAPTER 6. Accounting and the Time Value of Money. ……..…………………………………………………………. $10,000. 8,900 x 1.06 9,434 x 1.06 10,000. $10,000. 8,900. Using Present Value in Accounting. notes receivable and payable

E N D

2007 2006 2005 Discounted @ 6% CHAPTER 6 Accounting and the Time Value of Money ……..…………………………………………………………... $10,000 8,900 x 1.06 9,434 x 1.06 10,000 $10,000 8,900

Using Present Value in Accounting • notes receivable and payable • amortization of bond premiums and discounts • valuation of long-term assets Interest rates • Sometimes effective interest rates need to be estimated • purchase a 5-year, 3%, $1000 bond for $874 • Sometimes an appropriate interest rate must be chosen • capitalizing interest costs

Nper Rate Type Pmt Pv = number = number = number = number = number FV Future Value of a Single Sum Rate = 9% FV = ? PV = $1,000 Periods = 4

Nper Rate Type Pmt Fv = number = number = number = number = number PV Present Value of a Single Sum Rate = 5% FV = $5,000 PV = ? Periods = 4

($1300) ($1300) ($1300) ($1300) Nper Rate Type Pmt Pv = number = number = number = number = number FV Future Value of an Annuity Rate = 8% Periods = 4 FV = ? PV = $5,000

Date Cash Withdrawal Interest (8%) Inc (decr) in balance Bank Balance 1/1/03 5,000 12/31/03 (1,300) 400 (900) 4,100 12/31/04 12/31/05 12/31/06

$1000 $1000 $1000 $1000 Nper Rate Type Pmt Pv = number = number = number = number = number FV Second Example Rate = 8% Periods = 4 FV = ? PV = $0

Payments at beg. of period ($1300) ($1300) ($1300) ($1300) Nper Rate Type Pmt Pv = number = number = number = number = number FV Future Value of an Annuity Due Rate = 8% Periods = 4 FV = ? PV = $5,000

Date Cash Withdrawal Interest (8%) Inc (decr) in balance Bank Balance 1/1/03 5,000 1/1/03 (1,300) 1/1/04 (1,300) 1/1/05 (1,300) 1/1/06 (1,300) 12/31/06

Periods Periods Rate Rate PV PV Annuity Annuity FV FV AD? AD? Sample Problems What is the present value of $7,000, due 8 periods hence, discounted at 11%? Jane Pauley has $20,000 to invest today at 9% to pay a debt of $56,253. How many years to accumulate enough?

Periods Periods Rate Rate PV PV Annuity Annuity FV FV AD? AD? How much deposited every 6 months for next 5 years to accumulate $14,000. Interest rate = 8%, compounded semiannually? You deposit $15,000 on 8/31 in a bank account paying 3% interest compounded monthly. How much can you withdrawal on the first day of each of the next 9 months?

Periods Rate PV Annuity FV AD? What would you pay for a $50,000 bond that matures in 15 years and pays $5,000 a year in interest if you wanted to earn a 12% return?

Issuing Long-Term Bonds • Firm issues bonds and receives cash • premium: cash exceeds face value • discount: cash is less than face value $43,189 • Firm makes annual interest payments • based on face value and stated rate $5,000 • Firm pays face value to bondholders at maturity $50,000

Date Cash Payment Interest (12%) Inc (decr) in balance Carrying Amount 10/1/04 43,189 Amortizing Bond Discount or Premium Issuing bonds at a discount: Cash 43,189 Discount on Bonds Payable 6,811 Bonds Payable 50,000 10/1/05 (5,000) 5,183 183 43,372 10/1/06 (5,000) 5,205 205 43,577 10/1/19 (5,000) 5,893 893 50,000

Date Cash Payment Interest (12%) Inc (decr) in balance Carrying Amount 10/1/04 43,189 10/1/05 (5,000) 5,183 183 43,372 10/1/06 (5,000) 5,205 205 43,577 Making the first interest payment: Interest Expense 5,183 Discount - Bonds Pay 183 Cash 5,000 Making the second interest payment: Interest Expense 5,205 Discount - Bonds Pay 205 Cash 5,000

$1500 $1500 $1500 $1500 PV = $0 FV = ? Periods Rate PV Annuity FV AD? Future Value of a Deferred Annuity • An ordinary 8%, 4-year annuity deferred 2 years.

($1500) ($1500) ($1500) ($1500) PV2 = ? PV1 = ? FV = 0 Periods Periods Rate Rate PV2 PV1 Annuity Annuity FV FV AD? AD? Present Value of a Deferred Annuity • An ordinary 8%, 4-year annuity deferred 2 years.