Download

1 / 16

170 likes | 176 Vues

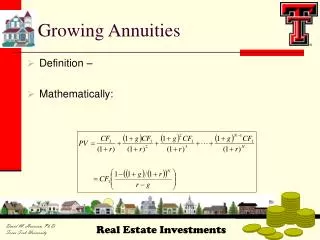

Lifetime Annuities. A public/private model for sustainable real lifetime additions to retirement income from superannuation assets.

E N D

Lifetime Annuities A public/private model for sustainable real lifetime additions to retirement income from superannuation assets. Disclaimer: Figures show are “ball-park” illustrations and no liability is accepted by Financial Demographics for any use of this material. Information is current only at 18 February 2011 Bruce Gregor FIAA AIA Financial Demographics

Purpose of this Presentation This presentation outlines a Proposed Research Project which would be conducted jointly by Financial Demographics and the Australian School of Business at the University of New South Wales. The purpose of the presentation is to seeksponsorship for this research. The presentation illustrates a working model of a system proposed by Financial Demographics for provision of lifetime annuities from part of Australian superannuation assets. Any figures used are purely “ball-park” indicators. The purpose of the figures is so that people unfamiliar with annuities and reinsurance can readily picture the system to be studied. The research project will provide actual numbers and conclusions from the latest academic research on mortality pooling and from population projections for Australia and superannuation assets.

Essential Elements of the Model • “Not for profit” annuity terms • Community rating of life expectancy • Maintain annuity assets in superfunds • Government covers extreme longevity risk • Government oversight of risk pooling • Standardisation of annuity terms • Compulsory 20% in deferred annuity • Nil net long term cost to government • Investment Guidelines for annuity pools

“Not-for-Profit” • Insurance company rates for annuities have been shown to include 15-25% loading for selection, longevity risk and profit margin • NFP Super system has substantial scale efficiency which is under-utilised • Insurance company annuity rates are hard to sell compared to high Aust. cash rates • Most people have modest super balances which need to be stretched as far as possible by working on cost margins and efficiency

“Community Rating” • Selection in voluntary insurance makes annuities more expensive • Assumes only long-livers are buying • ‘Catch 22’ of current annuity market • Rates are not attractive so no one buys • If everyone had to buy an annuity, rates would be more attractive • Deferred annuities are very attractive if community rating applies and NFP

Illustration – Annuity $pa / $100k Main Assumptions: Government Actuary’s Australian Life Table 2005-07 with 25 year average longevity improvement. Investment return 5.5%pa, inflation 2.5%pa. “Select” has 20% margin. Purchase price refunded on death (no interest). All annuity figures are current dollars which are assumed to be indexed for CPI inflation after purchase date.

Maintain assets in current funds • A strong fund regulatory structure exits including provision for segregated pension assets pools • Large funds can leverage current operational efficiency • If full annuitisation existed, post retirement assets would be about 25% of super assets within 20 years • Pooling annuitant mortality in current funds avoids transfer of assets to insurers and saves transaction/intermediation costs (assuming longevity risk can be absorbed by government)

Government covers extreme longevity • Govt. covers this for public servants • Govt. covers this for age pension • Insurers “over-reserve” for longevity risk due to unpredicted future trends and no natural hedge • Nil net cost to government if amount of extreme longevity reserve is balanced by less age pension outgo (if modest income test for deferred annuities) or levy on annuity pools– see Illustration.

Govt. Oversight of risk pooling • Govt. oversight increases confidence of fund members in annuity rates • Pooling reduces unproductive and costly “competitive” activity • Pooling gives more stable annuity rates averaging over more lives (subject to minimum no. of lives for participant pools) • Government actuary already maintains Life Tables • Future Fund money to incubate a reinsurance co-op company

Illustration • Required Reinsurance reserve for greater than projected longevity risk (which is in annuity terms) • Extreme risk level illustration is 2 x Govt. Actuary 25yr projection of mortality improvement • Equivalent Age Pension Income Test clawback (normal is 50%) to apply to Deferred Annuities: • 2.5% if all have 100% age pension • 5% if they average 50% age pension due to other income and assets • Alternative is to collect a levy of 1.5%pa of assets from deferred annuity pools • Reinsurance refund to DA pools if Australian population longevity exceeds projected level in annuity terms • Reinsurance company supervises the annual mortality equalisation transfers between DA pools

Standardised Annuity terms • Lifetime annuities are most efficient when early deaths release reserves to balance long-livers annuity payments (“communal assets”) • Complex optional annuity terms offer “all things to all people” and reduce the above efficiency / reduce annuity • Pooling works best if annuitant risks are as similar as possible in each fund participating in the pool and the aggregate of all pools equates close to population average mortality

Compulsory 20% Deferred Annuity • Many Australian’s have little experience with self management of income production from assets during their working life • Financial Planners are not incentivised to spread super money over life expectancy • Advance provision of deferred annuity covers the most fragile stage of life • Population ageing will bring old age voter pressure for age pension rises which could have been funded by super assets

How the Compulsory DA works Members Are educated On DA system Members commit 20% of balance to a DA pool Deferred Annuity Starts 55 60 65 70 75 Annuity Calculations • At age 60 the deferred annuity payment is advised • This payment is calculated from government actuary tables • Members are advised a new deferred annuity each year indexed for CPI • At age 75 the deferred annuity has a further one-off increase if the member’s selected annuity pool earned more on investment than the real return assumed in the original calculation of standard annuity rates • After 75 annuity stays fixed for duration of life except for CPI indexation

Nil net cost to Government • Future Fund invests in new reinsurance pooling company; on-sell equity to NFP funds when mature – say 10yrs+ • Modest income test on deferred annuities or levy on annuity pool to offset extreme longevity risk reserve for deferred annuities • Super funds responsible for annuity admin and keeping track of deaths • Reinsurance claims paid for extreme longevity are balanced by premiums paid • FF return + Cost of established and admin of Reinsurance company covered by sale price

Investment Guidelines for pools • 30% Maximum in listed equity exposure • All offshore assets 100% currency hedged • Annual cash income from investments to exceed a set scale % of annuity outgo • Inflation linked bonds encouraged • Requirement for participating funds to absorb assets and liabilities of any pools which fall below annuity payment sustainability rules • Governments required to give priority to inflation linked bonds(ILB) when issuing new debt until ILB’s on issue > 50% of deferred annuity pools’ assets

For more information on this Proposal, please contact: Bruce Gregor at cbgregor@optusnet.com.au