Download

1 / 16

160 likes | 291 Vues

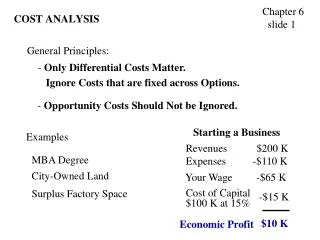

Cost Analysis. Yale Braunstein School of Information Management & Systems. How does this course differ from all other project-related courses at SIMS?. We explicitly look at alternatives. We care about economic feasibility. [others ?]. Why do we want to know costs?.

E N D

Cost Analysis Yale Braunstein School of Information Management & Systems

How does this course differ from all other project-related courses at SIMS? • We explicitly look at alternatives. • We care about economic feasibility. • [others ?]

Why do we want to know costs? • We need to measure and understand costs • To help the organization • Operate efficiently & effectively • Allocate scarce resources • Choose between competing projects • To meet legal & organizational requirements

General introduction to our approach • Identify opportunities & alternatives for meeting them • Agree on selection/evaluation criteria • Apply the criteria • Make choices/decisions and monitor results A nine-step, more detailed approach is on the web and in the handout. A complete manual is available in the computer lab.

Special problems with new technologies • New technologies, in general, and IT, in particular, often cause problems • Exact costs are unknown/unknowable • Only some benefits are quantifiable • New technology projects can change the organization, its outputs, etc.

Costing terms • Costs are misleadingly concrete. It is important to understand: • Allocated vs. out-of-pocket costs • Sunk costs • Opportunity costs • Fixed, variable & total costs • Joint costs • Marginal or incremental costs • Consistency is VERY important

Costs depend on your perspective • Department costs vs. project costs • Current costs vs. future costs; upfront costs vs. continuing costs; etc. • (More on this later) • For public projects: CTA, CTG, CTN

Costs vs. Prices • We need to distinguish between costs and prices • Energy in California ! • DSL (component-by-component) • “Fully distributed costs” or “allocated costs” are very popular and can easily mislead • The leased-line anecdote…a true story of faulty economic logic in a major university

Where to Get Cost Information • Statistical studies • Engineering studies • Simulations • Bills of Materials • Comparables • Case studies • Previous experience (at your organization & elsewhere)

Additional considerations • We do a sensitivity analysis to identify those factors that have the major impacts on costs • Try to understand the issues relating to economies of scale and scope. • Computer automation in publishing example • See Morton * : • IT potentiallyincreases productivity by lowering transaction costs…if you reorganize work. * Michael Scott Morton, “How Information Technologies can Transform Organizations,” in Rob Kling, Editor, Computerization and Controversy (San Diego: Academic Press 1996) 148-160.

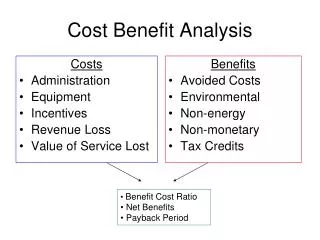

Cost-benefit analysis • We distinguish between cost-benefit analysis and cost-effectiveness analysis • In CBA, both costs and benefits are measured in dollars • In CEA, only the costs are measured in dollars; we use non-monetary measures for the benefits • Examples: increased reliability, reduced lag times

Time value of money • General rules: • Dollars spent at different times have different costs to the organization • Dollars received at different times have different values to the organization • Therefore, we need to explicitly account for timing of cash flows (in & out) • We “discount” future flows to the present to obtain their “present value”

Calculating PVs • Logic: • Take each year’s cash flow and “discount” it back to the present using the “discount rate” • See spreadsheet with examples

Three ways to compare projects • Payback period – NEVER use this • Internal rate of return – very common, but has problems • One: assumption about re-investment • Two: multiple solutions possible • Three: (most important) can lead to incorrect choices with MX projects • Net present value – the preferred approach

Review: General principles • Focus on total costs OR incremental costs, whichever is appropriate • Are we introducing something entirely new or a change in an existing system? • Comparability of data is important • Timing matters • Have similar start & end points • Know what is in and what is out

Using the principles • Sunk costs are sunk – ignore them • You need to know the purpose of the analysis • Planning for the future vs. benchmarking current operations • Forecasting & Projections • Know what is changing