Download

1 / 26

260 likes | 381 Vues

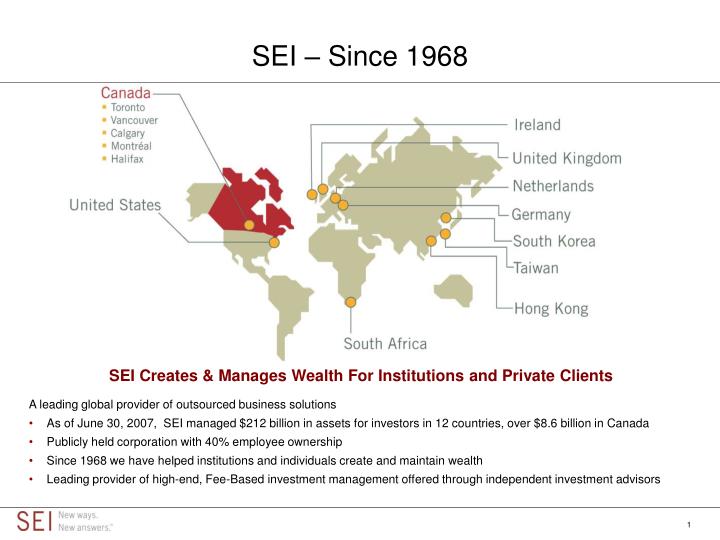

SEI – Since 1968. SEI Creates & Manages Wealth For Institutions and Private Clients. A leading global provider of outsourced business solutions As of June 30, 2007, SEI managed $212 billion in assets for investors in 12 countries, over $8.6 billion in Canada

E N D

SEI – Since 1968 SEI Creates & Manages Wealth For Institutions and Private Clients • A leading global provider of outsourced business solutions • As of June 30, 2007, SEI managed $212 billion in assets for investors in 12 countries, over $8.6 billion in Canada • Publicly held corporation with 40% employee ownership • Since 1968 we have helped institutions and individuals create and maintain wealth • Leading provider of high-end, Fee-Based investment management offered through independent investment advisors

Potential Danger Signals in Your Portfolio Yes No • Lack of clear investment policy (IPS) • Investments mismatched with objectives • Inappropriate level of risk • Lack of diversification • Under performing investments or managers • Style drift • Overlapping investments or management styles • Excessive expenses or trading activity • Lack of monitoring, adjusting, rebalancing • Unclear or untimely reporting • Lack of communication and service

Proper Asset Allocation DiversifiesAcross Global Security Markets International Developed Equities High Yield Canadian Equities International Fixed Income Canadian FixedIncome Emerging Markets Equity Emerging Markets Debt

Why Diversify by Asset Class? Performance of Various Asset Classes: 1993 to 2006 Annual Total Returns of Key Indices (Based on Sector) 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 The information seen is for illustrative purposes only and is not reflective of the performance of any SEI Funds. Past performance is no guarantee of future results.

Why Diversify by Style? Performance of Various Canadian Equity Investment Styles: 1994 to 2006 Annual Total Returns of Key Styles The information seen is for illustrative purposes only and is not reflective of the performance of any SEI Funds. Past performance is no guarantee of future results.

Your Optimal Asset Allocation • How much in stock? • How much in bonds? • How much cash? • How much in Canadian securities? • How much foreign content? The Importance of Asset Classes Canadian vs. Foreign? Stocks? Cash? Bonds? Asset Allocation = Diversification = Lower Risk

Institutional Investors Consider both return and risk Invest long term Use professional managers Have a portfolio Diversify Use a scientific process Retail Vs. Institutional? Retail Investors • Chase return • Buy/sell short-term • Make decisions themselves • Have individual positions • Concentrate • Act on emotion

SEI Managed Process A Scientific Approach to Disciplined Investing Planning Process Establishes Goals Sets Risk Limits Custom Portfolio Sets Long Term Target Sets Short Term Limits Manager Selection Low Cost Vehicle Specialist Managers Rebalancing Reallocation Maintains Objectives Monitoring and Reporting Keeps YouInformed and On Track

Mutual Funds vs. SEI… Represents a Difference From Regular Mutual Funds • SEI Manager of Managers • Customized asset management from the world’s leading money managers • Combining multiple managers intelligently with less risk • Strict monitoring of each manager Regular Mutual Funds • Intensely marketed products • Good managers go bad • Star managers move • DSC fees lock people in • Mutual fund portfolios become unbalanced and too risky

SEI Portfolios vs. Separately Managed Accounts • While most SMAs offer access to one portfolio manager, SEI’s Portfolios offer access to numerous global portfolio managers, typically only available to pension plans or institutional investors • SEI’s programs can offer clients further diversification than in SMAs, as portfolio manager’s specialties lies within different mandates • The chart below gives examples of some account minimums of portfolio managers within the underlying funds of the SEI Portfolios * Separate Account Minimums listed are as of December 2006

Asset allocation is the key determinant of performance Portfolio structure is the key determinant of performance within each asset class Specialist managers add value in their respective areas of expertise Continuous monitoring of each manager’s daily trading is the only effective way to control managers and maintain portfolio structure SEI’s Investment Philosophy Objective: Achieve superior long-term investment returns while managing risk Efficient Portfolio Construction Structured Asset Allocation Continuous Portfolio Monitoring Manager Selection

SEI’s Manager Research Process is Proven and Comprehensive • Identify the inefficiencies in the market • Measure the quality of the alpha source • Understand the sustainability of the inefficiencies Analyze Markets to Identify Drivers of Excess Return (Alpha Sources) • Proprietary framework to assess markets • Leverages academic and manager network • Global sourcing of managers • Leverage knowledge and reputation Define Manager Universe by Alpha Source • 90+ experienced professionals worldwide • Proprietary database with 26,000 products • Strong relationship with academia • Understand drivers of return • Separate quality of decisions from outcomes • Determine competitive advantage Analysis of Decisions and Decision Making Process • Extensive analytical technology • Database of historical investment decisions Onsite Due Diligence • 20+ years assessing investment firms • 1,000 global meetings annually • Assess sustainability of competitive advantages Construct Portfolios to Diversify Alpha Risk • 30+ current managers • Approved backup list of managers • Incentive based research team • Analyze changes in market dynamics • Monitor firm and process changes

Manager Discovery: Casting a Wide Net • Client and portfolio objective drive manager discovery • Seek opportunities and inefficiencies in the market place • Reputation leads to many firms visiting SEI’s offices each year • Focused research - no legal requirements to have opinion on many firms • Breadth of research allows us “first mover” advantage • Global presence and industry experience 19,000 Managers in initial universe 3,000 Managers remain after initial fundamental screen 1,000 managers remain after qualitative screen 45 managers remain for further analysis

SEI’s Investment Management Unit:Leveraging Global Coverage Client Portfolio Management Portfolio Strategy Global Investment Strategy Fundamental Research | Quantitative Research Global Fixed Income Non-Directional Strategies GlobalEquity Global PrivateMarkets Execution and Operations *As of 1/31/2007

Additional Monitoring Ongoing dialogue with managers Onsite annual visits Risk management Our Monitoring Process is Rigorous and Dynamic Daily Weekly Monthly • Performance attribution • Review of buys & sells Daily trade oversight Performance attribution Review of buys & sells

Reasons for Sell Decision Organization (stability, liquidity event, etc.) Investment Team (turnover, generational transition) Process (inability to exploit inefficiencies, asset growth) Structural Change in Market Better Ideas (discovered higher quality manager) SEI Triggers for Manager Changes SEI Manager Turnover (1995-2006) Organization (1) 6% Better Ideas (5) 22% Team (2) 20% Process (3) Structural (4) 29% 23% • Advantages of SEI’s Sell Discipline • Decision Speed • Back-up Managers • Market and Industry Analysis

Canadian Equity Structure As of August 2007

Portfolio Structure: Style and Size % Importance of Large Cap Manager Style 45 Large Cap 40 Growth 35 Outperforms Average = 9.84% 30 Return Difference 25 Large Cap Value Outperforms 20 15 10 5 0 Year 82 83 84 85 86 87 88 89 90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 % Importance of Market Capitalization 25 Large Cap Outperforms 20 Return Difference Small Cap 15 Outperforms 10 5 0 Source: BARRA, SEI Year 82 83 84 85 86 87 88 89 90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06

Canadian Equity Market Investing (1998 – 2007) Style indices returns are courtesy of BARRA Consulting. Commissions, trailing commissions, management fees and expenses all may be associated with mutual fund investments. Please read the prospectus before investing. Rates of return do not take into account sales, redemption, distribution or optional charges or income taxes payable by any security holder that would have reduced returns. Mutual funds are not guaranteed, their values change frequently and past performances may be repeated. Index performance returns do not reflect any management fees, transaction costs or expanses. One cannot invest directly in an index. Past performance does not guarantee future results.

SEI Sample Balanced Fund As of August 2007 5 Asset Classes 25% Canadian Equity 35% Foreign Equity 40% Fixed Income Multi-Asset International Equity Cdn. Fixed Income U.S. Equity Global Fixed Income Canadian Equity Canadian Equity 10 Underlying SEI Funds Cdn. Equity - 23% Cdn. Small Company Equity - 2% SEI Canadian U.S. Large Company Equity - 14% U.S. Small Company Equity - 2% U.S. MidCap Synthetic - 5% SEI U.S. Large SEI U.S. Small EAFE Equity - 12% Emerging Markets Equity - 2% Cdn. Fixed Income - 30% Real Return Bond - 6% Enhanced Global Bond - 4% Multi-Fund SEI EAFE Equity Fund Company Fund Company Fund Equity Fund 30 Investment Styles 26 Styles Large Cap Market Driven Relative Value Relative Value Value Premium Global Value Value Focused Value Global Bonds Contrarian Value Duration Management Deep Value Value Premium/Momentum Deep Value Value Contrarian Global GARP Multi-Style Momentum Growth Investment Grade/Credit Relative Value Core Value Global Growth Emerging Growth Earnings Anticipation GARP Relative Growth Earnings Momentum Factor Customization Small Cap Value Core Quality Growth Small Cap Growth Core – Customized Factors Growth Core – Volatility Capture Value Factor Rotation Discipline Equity Core Research Factor Customization 36 Managers Sanford C. Bernstein & Co., LLC Beutel, Goodman & Company Ltd. Strategic Fixed Income, LLC Jarislowsky Fraser Limited Aronson+Johnson+Ortiz, LP Sionna Investment Managers Inc. Connor, Clark & Lunn Inv. Mgt. Inc. AXA Rosenburg Inv. Mgt. LLC LSV Asset Management McKinley Capital Management Inc. Goodman & Company Inv. Cnsl Ltd. Sanford C. Bernstein & Co., LLC Addenda Capital Inc. Multi-Manager Highstreet Asset Management Inc. Delaware Investment Advisors Capital Guardian Trust Company AEGON Capital Management Inc. Fuller & Thaler Asset Mgt, Inc. Goldman Sachs Asset Mgt., L.P. Co-operators Inv. Counselling Ltd. PCJ Investment Counsel Ltd. Quantitative Management Ass, LLC J. Zechner Associates Inc. Montag & Caldwell, Inc. MFC Global Investment Mgt. Fiera YMG Management Inc. AllianceBernstein LP Beutel, Goodman & Company Ltd. Quantitative Management Ass, LLC The Boston Co. Asset Mgt, LLC Enhanced Investment Tech., LLC Montrusco Bolton Investments Inc. Martingale Asset Management, L.P. Please note the number of managers is based on the total managers in each asset class. TD Asset Management Inc. Los Angeles Capital Management PanAgora Asset Management, Inc.

Automatic Portfolio Rebalancing • Rebalancing ensures that your recommended asset mix is constantly in place. • Rebalancing reduces unintended and unnecessary risk keeping your portfolio on the right course. Equities 60% CurrentAssetAllocation Cash 10% Fixed Income 30% Equities TargetAssetAllocation Cash 50% 5% Fixed Income 45%

What Should You Expect from a Professional Investment Advisor? • Keep you from making emotional decisions that may hurt your long-term goals • Take the time to update you on your portfolio’s progress and keep you on course with your investment objectives • Continuously monitor your portfolio • Provide you with a customized monthly report and quarterly and annual reporting statements • Keep you abreast of any additional opportunities in the market • Develop an investment plan based on your needs that utilizes an institutional investment process The right advisor is someone who will:

Representative Canadian Institutional Client List AFG Industries Ltd. Saint-Augustin, QC Bell Aliant Regional Communications Saint John, NB Blount Canada Ltd. Guelph, ON BOC Canada Limited Mississauga, ON Brewster Transport Company Limited Banff, AB Brink’s Canada Limited Toronto, ON BAX Global (Canada) Ltd. Mississauga, ON Canadian Tire Corporation Limited Toronto, ON Connell Industries Canada CompanyMississauga, ON Diamond Foundation Vancouver, BC Falconbridge Limited Toronto, ON Health Services Foundation of the South Shore Bridgewater, NS Hitachi Construction Truck Manufacturing Ltd. Guelph, ON HSBC Financial Corporation Limited Toronto, ON Jewish Community Foundation of Montreal Montreal, QC Lafarge Canada Inc. Concord, ON Laurentian University of Sudbury Sudbury, ON Laurentian University of Sudbury Sudbury, ON Mercedes-Benz Canada Inc. Toronto, ON Moore Corporation Limited Chicago, IL (USA) Northern Cancer Research Foundation Sudbury, ON Northern Development Initiative Trust Prince George, BC Peerless Clothing Inc. Montreal, QC Reitmans (Canada) Limited Montreal, QC Ryerson Canada, Inc. Etobicoke, ON Smucker Foods of Canada Co. Markham, ON St. Peter’s Seminary Foundation London, ON Representative clients are selected by SEI to illustrate a sampling of SEI’s client base, but may not necessarily endorse all of the services provided by SEI. List as of June 30, 2007.

Representative U.S. Corporate Institutional Client List Ahlstrom USA Windsor Locks, CT Alfa Insurance Companies Montgomery, AL AT&T Inc. San Antonio, TX Builders Mutual Insurance Raleigh, NC California Casualty Management Co. San Mateo, CA Carlisle Companies Inc. Charlotte, NC C & D Technologies, Inc. Blue Bell, PA Clarks America, Inc. Boston, MA Cleveland-Cliffs Inc Cleveland, OH Comcast Corporation Philadelphia, PA CommScope* Hickory, NC CoorsTek, Inc.* Golden, CO Deloitte & Touche LLP Morristown, VT Ecolab, Inc. St. Paul, MN Elkem Metals Inc. Pittsburgh, PA ESSROC Italcementi Group Nazareth, PA Federal Mogul Corporation Southfield, MI FLSmidth Inc.* Bethlehem, PA Givaudan Corporation Cincinnati, OH Hercules, Inc. Wilmington, DE Independence Community Bank Brooklyn, NY Intelsat Global Services Corp. Washington, DC Jackson Energy Authority Jackson, TN JM Smucker company Orrville, OH Joy Global, Inc. Milwaukee, WI Lafarge NA, Inc. Herndon, VA LVMH Moet Hennessy Louis Vuitton New York, NY Marine Corps Community Services Quantico, VA Nalco Holding Company Naperville, IL Nashville Electric Services* Nashville, TN National Services Industries, Inc. Atlanta, GA Ottaway Newspapers Campbell Hill, NY Panasonic Corporation Secaucus, NJ Pearson, Inc. New York, NY Qantas Airways Ltd.* Los Angeles, CA Ryerson Chicago, IL SAP America Inc. Newtown Square, PA The Clearing House New York, NY US Filter Corporation Palm Desert, CA Valero Energy, Inc.* San Antonio, TX Representative clients are selected by SEI to illustrate a sampling of SEI’s client base, but may not necessarily endorse all of the services provided by SEI. List as of June 30, 2007. * Sourced through the Advisor channel

Representative Global Institutional Client List South Africa UK • Old Mutual Symmetry (Cape Town) • Grant Thornton (Johannesburg) • Transnet (Johannesburg) • BOC Group plc (Windlesham, Surrey) • Diamond Trading Company (London) • Nynas (Cheshire) • Perenco (London) • University of Bristol (Bristol) Hong Kong Benelux • American Club Hong Kong • Hong Kong Jockey Club • Hong Kong Housing Society • Shui On Investment Company • Hong Kong Electric Holdings Limited • Equens, St. Psf. (Utracht) Representative clients are selected by SEI to illustrate a sampling of SEI’s client base, but may not necessarily endorse all of the services provided by SEI. List as of June 30, 2007.

Disclosures • For more information about the SEI funds, please consult with your investment professional. The prospectus and other important information relating to the SEI funds can be found at www.seic.com or www.sedar.com. • Commissions, trailing commissions, management fees and expenses all may be associated with mutual fund investments. Please read the prospectus of the SEI fund before investing in them. Mutual fund securities are not covered by the Canada Deposit Insurance Corporation or any other government deposit insurer.Mutual funds are not guaranteed, their values change frequently and past performances may not be repeated. • For those SEI funds which employ the 'manager-of-managers' structure, SEI Investments Canada Company has ultimate responsibility for the investment performance of the fund due to its responsibility to oversee the sub-advisors and recommend their hiring, termination and replacement. • Material that discusses the SEI funds and index returns, represent an assessment at a specific point in time and is not intended to be a forecast of future events, or a guarantee of future results. You cannot invest in an index. Index returns do not reflect the impact of any management fees, transaction costs or expenses. The index information presented is for illustrative purposes only, and is not reflective of the performance of specific SEI Funds. • Except as otherwise noted, the rates of return shown are the historical annual compounded total returns including changes in unit value and reinvestment of all distributions. The rates of return shown for periods of less than one year are simple rates of return. Rates of return do not take into account sales, redemption, distribution or optional charges or income taxes payable by any security holder that would have reduced returns. • The information contained herein is for general information purposes only and is not intended to constitute legal, tax, accounting, securities, or investment advice, nor an opinion regarding the appropriateness of any investment. You should not act or rely on the information contained herein without obtaining specific legal, tax, accounting and investment advice from an investment professional.