Download

1 / 23

230 likes | 322 Vues

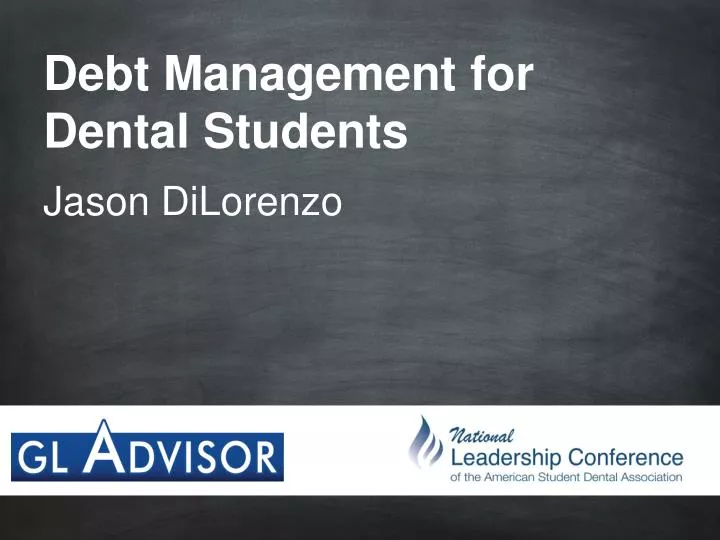

Debt Management for Dental Students. Jason DiLorenzo. Debt levels have more than tripled in the last 17 years. Changes in Student Debt Levels. ~$203K. ~$115k. ~$50k. 1993. 2003. 2011. * Based on data collected by ADEA and GL internal student database. Changes in Student Debt Levels.

E N D

Debt Management for Dental Students Jason DiLorenzo

Debt levels have more than tripled in the last 17 years Changes in Student Debt Levels ~$203K ~$115k ~$50k 1993 2003 2011 * Based on data collected by ADEA and GL internal student database Changes in Student Debt Levels - Confidential Document, Property of Graduate Leverage, LLC -

Agenda • Federal Loan Basics • Federal Loan Repayment Options • Private Loan Repayment Options • Dental Case Studies • How to Calculate Payments • Review and Q & A Key Takeaway: How recent and upcoming regulations will help address the mounting debt burden facing many dental students.

High Cost To Borrower Low Cost To Borrower Sources of Funding High Rate Private • Federal Loans: (Stafford, Grad PLUS) • Federal Stafford: Fixed Rate 6.8% (since July 1st 2006) • Subsidized: government pays interest during school and deferment • Unsubsidized: all interest accrues • Direct Graduate PLUS: Fixed Rate 7.9% (all interest accrues) • Private Loans: • Sometimes needed for Externships, Internships, or Residencies • Interest rates vary • Margins have decreased but minimum credit requirements have tightened Grad PLUS Unsubsidized Stafford Subsidized Stafford Perkins Low Rate Private Grants/Scholarships

Key to student loan management is finding the right balance between these two competing pressures. The right balance will change over time! $1,000 $1,000 Liquidity $ 500 $ 150,000 $ 300,000 Total Cost of Your Student Debt Competing Pressures - Confidential Document, Property of Graduate Leverage, LLC -

Federal Loan Repayment Options • Ways to Postpone Payments: • Forbearance: • NO SUBSIDY – All loans accrue interest. • Economic Hardship Deferment (EHD): • FULL SUBSIDY – Unsubsidized accrue interest. • In-School Deferment: • FULL SUBSIDY – Unsubsidized accrue interest • Ways to Make Full Payments: • Standard 10 Year Term • NO SUBSIDY – Shortest term available • Prepaying • Prepayment allowed without penalty on all federal repayment programs.

Federal Loan Repayment Options • Ways to Reduce Payments: • Extended 25 Year Term: • NO SUBSIDY • Consolidated 30 Year Term: • NO SUBSIDY • Available for consolidated loans $60,000 or greater • Income-Based Repayment (IBR): • PARTIAL SUBSIDY • Pay As You Earn (ICR-A): • PARTIAL SUBSIDY • No loans before Oct. 2007 + loan post Oct. 2011

Partial Financial Hardship • Limit monthly payment to 15% of discretionary income, capped at 10-year standard payment • 2012/2013:10% (ICR-A) • Government Subsidy • Subsidized interest not covered by reduced payment is paid by government • Subsidy is provided for maximum of 3 years • Taxable Loan Forgiveness • After 25 years any outstanding balance is forgiven • 2012/2013:20 years (ICR-A) IBR and ICR-A

Many Graduates Not Taking Advantage Of New Tax Breaks • Taxes during final year school: • Lifetime Learning Tax Credit • Tuition and fees tax deduction • Married Filing Jointly or Separately • Decision Process: • Tax benefit of each option calculated • Changes in subsidy benefit added back for final number

Savings opportunity immense – more stringent requirements. • PSLF – Public Service Loan Forgiveness • Federal program enacted by Congress in 2007 • Specific requirements: • Borrower must make 120 qualifying payments on a Federal Direct Loan • Borrower must work for a public service entity as defined by the program, such as a Federal, State, Local, or non-profit organization • New Employment Certification Form (released 2012) Tax Free Forgiveness

Understand the Loss of Federal Benefits % Private or Grad PLUS Loan 7.9% 3% 7.5% ? 4.9% Interest Rate Increase? Current For illustrative purposes only. Assumptions based on good credit & sample lenders. Private Loans or Federal Loans - Confidential Document, Property of Graduate Leverage, LLC -

Important Considerations Federal Loan Benefits: Evaluate loss of federal repayment plans / forgiveness opportunities Fees: Application or origination fees may erode savings potential Interest Rate: Evaluate rate difference and type: Variable vs. Fixed Pay Down Quickly Refinance to Lower Interest Rate Private Loan Grad PLUS 7.9% / 8.5% Credit Card Debt 15%+ Solutions for High Rate Debt

Monthly Payments Total Payments Y1: $264 Y10: $856 Y20: $1,303 $329,435 ICR-A* $504,340 Y1: $396 Y10: $1,284 Y20: $1,955 IBR* $1,901 $1,774 $570,295 $638,513 30 Year Consolidated Term 25 Year Extended Term Y4:$3,757 $450,799 3 Year Forbearance + 10 Year • Case Details • 2013 graduate, unmarried, family size of one • $260,000 total debt, all Federal debt ($159K Stafford / $101K Grad PLUS) • $100,000 starting salary increasing by 3% annually • high monthly expenses * Total payments under ICR-A and IBR include tax liability generated from forgiven loans. Case #1

Present Value Savings of ~$90k * PV analysis includes tax liability and assumes 3% annual increase in salary increase. Detailed assumptions available upon request. - Confidential Document, Property of Graduate Leverage, LLC -

Monthly Payments Total Payments $334,185 Y1: $0 Y10: $2,078 Y25: $2,078 IBR* $342,963 Y1: $0 Y10: $1,517 Y20: $1,984 ICR-A* $385,901 $1,286 25 Year Term Y4: $1,553 $466,025 3 Year Forbearance + 25 Year • Case Details • 2013 graduate, married, family size of three (one child) • $202,000 total debt • $25,500 Subsidized Stafford and $136,500 Unsubsidized Stafford @ 6.8% • $20,000 Grad PLUS @7.9% and $25,000 Private Loan @ 9.5% • 1 year of general practice residency at $25,000, salary increases to $120,000 • Spouse salary of $60,000 * Total payments under ICR-A & IBR include tax liability generated from forgiven loans. Case #2

Case #2 Total Paid $ $38,819 $31,820 5.0% 9.5% Loan Refinance 9.5% PrivateLoan Lowering interest rate on private loan by 4.5% saves $7,000 in interest costs.Greater savings for larger principle amounts.

Case Details • 2013 graduate, unmarried, family size of one • $96,000 total debt • $80K Stafford @ 6.8% • $8K Private @ 8.25% • $8K Private @ 9.5% • $130,000 starting salary increasing by 3% annually, NO FORGIVENESS 1st & 2nd Year Monthly Payments Extra Cash Flow $924 $0 10 Year Standard $350 $583 IBR $389 $500 ICR-A Case #3 Targeting

Targeted Repayment Plan Non-payment 4.75% Non-payment 6.8% 7.9% Non-pay 9.25% 1 yr 5 yrs 0.5 yr 7 yrs 9.5 yrs Typical Repayment Plan Consolidation – 4.75% Stafford – 6.8% Loans Grad Plus – 7.9% Private Loan - 9.25% Repayment Period 8 yrs 10 yrs $11,675 Effective Rate (APR) = 6.29% Effective Rate (APR) = 5.69% *Assumes $168,000 in federal debt and $8,000 in private loans Case #3 Targeting

Targeting Private Loans Total Paid $ Savings of $6,566 earned in 28 months of prepayment. $12,422 $11,775 10 YEARS 10 YEARS $9,146 $8,485 28 MONTHS 15 MONTHS 9.5% 9.5% w/$500 prepay 8.25% 8.25% w/$500 prepay Case #3 Targeting

Returns PLUS Loan 8.1% Average PLUS Return S&P 500 7.4% Average S&P Return (A/T) All Returns Here Are After Tax 16% 8% 0% 1940 1960 1987 2001 Sources: Yale Econ/Robert Shiller, Standard & Poor’s, Federal Reserve, Bloomberg Case #3 - Should I Be Investing? - Confidential Document, Property of Graduate Leverage, LLC -

What every dental student with loans should do: Understand Your Debt • What kind of loans do I have? (Federal Stafford, GRAD Plus, Perkins, etc.) • Who is my lender? (Federal Direct, Federal through Private Lender, Non-Federal Private Lender) • What are the interest rates on my loans? (fixed, variable, 6.8%, 7.9%, 8.5%, etc.) Position Loan for Appropriate Balance Between Liquidity and Total Cost • Calculate monthly payment options and compare to monthly budget • Take advantage of “exceptions to the rule” – targeting and forgiveness • Evaluate refinancing opportunities - Confidential Document, Property of Graduate Leverage, LLC -

What every dental student with loans should do: 3. Prepare & File Taxes Advantageously • Preparation in fall of final year to understand tax implications for loan subsidy programs • Understand the trade-off of filing jointly with spouse • File taxes in final year as appropriate 4. Manage your Financial Net worth • Properly allocate discretionary income • Only invest when returns exceed cost of debt and liquidity issues met

Jason DiLorenzo 415-722-8552 jdilorenzo@glAdvisor.com If you have any questions or would like a personalized debt assessment, please call or visit our website. www.gladvisor.com www.facebook.com/glAdvisor www.twitter.com/glAdvisor Thank You *The information in this presentation is for informational purposes only.