Download

1 / 39

390 likes | 443 Vues

LIABILITY INSURANCE - INTRICASIES. BY. Liability - Meaning. As per dictionary - responsibility or accountability to pay. Legal Liability connotes – strict liability (legal compulsion to pay)

E N D

Liability - Meaning • As per dictionary - responsibility or accountability to pay. • Legal Liability connotes – strict liability (legal compulsion to pay) • A wrong doer is obligated to pay as damages to the aggrieved person for the personal injury or damage to the property of the later.

Civil Liability Case made by an injured party against the wrong doer resulting in: Damages in monitory terms . Criminal Liability Enforced by the state resulting in: a. Fines/penalties b. Imprisonment c. both a & b above Liabilities – Civil Vs Crime

Civil Liability may arise from • Tort • Statutes • Contracts

Liability – Tort Vs Contractual • In Tort there is no privity between parties and the duty breached affect the society at large. • whereas there is clear privity based on offer and acceptance. It applies only the party to the contract • Liability Insurance Mainly concerned withTort as result of negligence and nuisance

Instances of Tort • Libel • Slander • Negligence • nuisance

WHAT IS NEGLIGENCE • ABSENCE OF CARE: it can be established when: • Existence of duty of care towards third party • Breach of that duty leads to an accident • Such accident resulted in Injury or damage to Properties • Casual connection between breach and the injury or damage

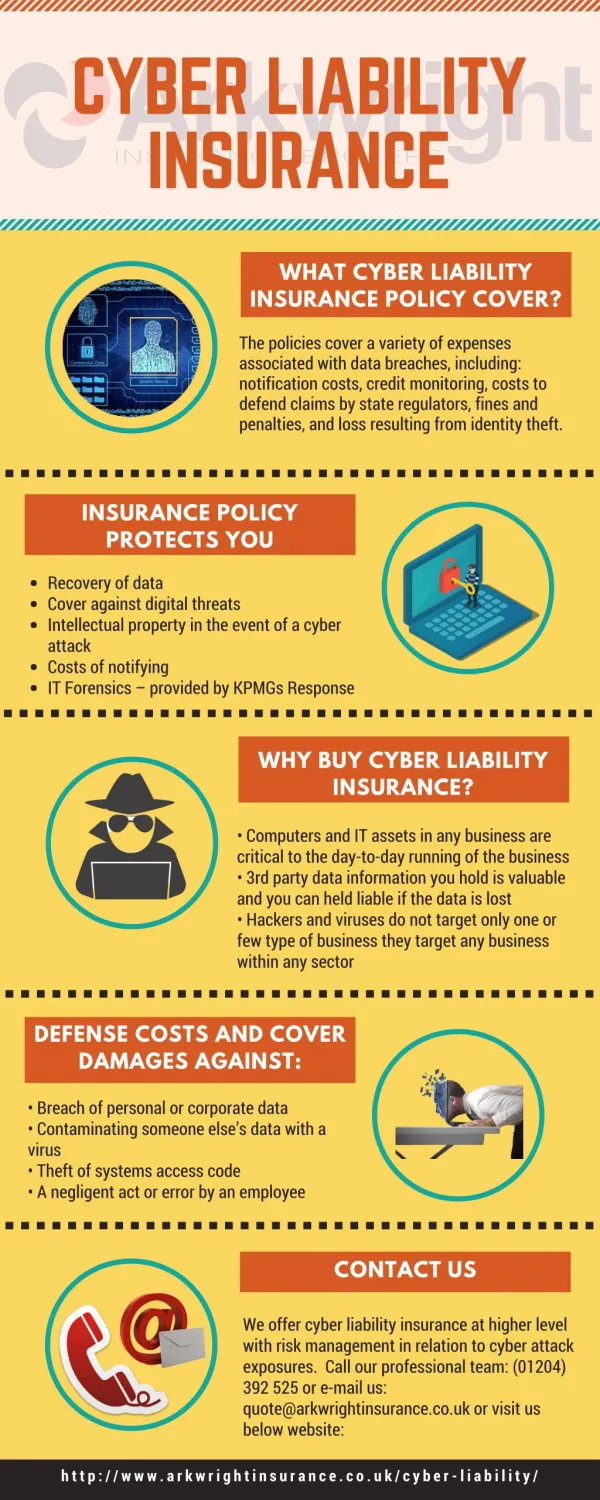

Liability Policies • Public Liability (Industrial Risks) Policy • Public Liability (non-Industrial Risks) policy • Public Liability Act Policy • Product Liability policy • Professional Indemnity (Doctors) Policy • Professional Indemnity (Medical Establishment) policy • Professional Indemnity (chartered Accountants) • Professional Indemnity (Architects/engineers) • Professional Indemnity (Advocates) Policy • Directors and Officers Liability Policy • IPO/prospectus liability policy • Carriers’ Legal liability Policy • Workmen’s Compensation Policy • Lift Insurance (Third Party) Policy • Couriers legal Liability Policy • Automobile Liability • Cyber crime liability Policy • Commercial general Liability policy

Public Liability – operative clause “----------Will indemnify the insureds against their legal liability to pay compensation including claimant’s costs, fees and expenses in accordance with the Indian Law. The indemnity only applies to claims arising out of accidents occurring in the insured premises during the period of Insurance, first made in writing against the insureds…and arising out of and in connection With the business specified ….”

INDEMNITY • To the insured • To others • Anybody acting on behalf of the insured • Cross Liability • Components • Damages • Cost • Expenses • Towards • For bodily injuries and damage to the properties of third parties • Limits – AOA and AOY

POLICY BASIS Occurrence Basis Claims Made basis Cover retrospective and responds to incidents occurred on or after the policy retroactive date reported during the Policy period Single indemnity of the policy during which the claim is made first in writing against the insured Policy cancellation poses problem Always claims are made under current policy. Non-existence is very remote There is opportunity to revise the indemnity limit each year • Cover prospective and responds to incidents during the policy period - regardless of when claims are reported. • Have accumulative effect of indemnity limit over a period since Separate indemnity limit for each year of policy • Not much impact on policy cancellations • Insurance Co’s non-existence at the time of Claim is also possible • Long gap make the indemnity inadequate

Terminologies commonly used in Liability Policies • Indemnity Limit AOA and AOY • Injury • Damage • Policy dispute clause • Compulsory Excess • Voluntary Excess • Cross Liability • Claims made Basis • Occurrence basis • Claim series clause • Defense Costs • Excess Liability • Retroactive Date • Notification extension Clause • Extended claim reporting Clause • Right to defend • Duty to defend

Public Liability - Rating Factors • Risk Group • Turn over • Limit of Indemnity and ratio AOA:AOY • Number of godown • Effluent discharge (treated) through pipe lines • Extensions Pollution, Transportation and AoG

Public Liability Insurance – Important Exclusions • Liability assumed by agreements • AoG Perils, transportations and pollution • Deliberate non-compliance of statutory obligations • Pure Financial Losses ( loss of good will, market etc. • Personal Injuries like libel, slander etc. • Infringement of plans, copy rights • Fines and penalties • Motor Third party • Damage to Property under custody of insured • Liability prior to Retroactive date

Public Liability Policy (Non Industrial Risks) • Office / Residential Premises / Medical Establishment / Research Institutes & Laboratories / Air Port Premises • Hotels / Motels / Clubs / Restaurants / Boarding and Lodging Houses / Guest Houses including Flight Kitchens • Cinema Halls / Auditorium / Theatres / Open Theatres / Public Halls • Schools / educational Institution / public Libraries • Film Studios – Indoor & outdoor / Circus / Zoo • Depots / Warehouses / Godowns / shops and Tank forms • Exhibitions / Fairs and Fetes / stadium and pandals

Public Liability Act Policy (Issued as per Public Liability Insurance Act 1991) Objective “To Provide through insurance Immediate relief by owners to Persons affected due to accident while handling hazardous Substances on No Fault Liability Basis” Special Features • Indemnity limit AOA: Minimum equal to Paid up capital up to a maximum of Rs.5 Crs. • Indemnity limit AOY: 3 times of AOA subject to a maximum of Rs. 15 Crs • Claims Exceeding the above Limit is to be met from Environmental Relief Fund set up under sec 7 of the Act • Excess liability over and above has to borne by the owner • Equal amount premium has to be collected from the insured towards the Fund.

PLI Act Policy – contd.. Schedule of Compensation: • Towards Medical Exp. Upton a maximum of Rs.12500/- in each case. • Toward fatal Accident Rs. 25000/- per Person (besides medical Expenses) • Towards PTD Rs. 25000/- per person (besides medical expense) • Towards PPD % of disability on Rs. 25000/- • Towards loss of wages Rs. 1000/- per month if hospitalization is beyond 3 days and the injured is above 16 years of age • Towards property damage Rs. 6000/- per person • The claim settling authority is the District Collector

Product Liability - Coverage • Indemnity to the insured towards • Damages • Cost • Fees and expenses • for bodily injuries, pollution and damage to the properties of third parties • arising out of accidents during the POI due to defects in the specified products sold and delivered • Claim made against the insured first in writing during the policy period • Subject to Limits – AOA and AOY

Product Liability - exclusions Cost incurred for repair and recondition of the defective product Product recall expenditure Product intended for incorporation into aircraft Deliberate disregard of insured’s Technical and administrative management to take reasonable care to prevent claims Injury to employees War and nuclear perils Loss of market or good will

Product Liability - Extensions Vendors’ Liability Named unnamed Technical Collaborators Product recall expenditure Expenses incurred to recall the product as a result of a decision taken by the insured. The decision to recall should have been taken during the period of insurance. The recall decision is necessitated because of the possibility further legal liability due to the continuous use or consumption Excluding Recall under Government Order. Recall of product under the custody and control of insured or his representative or its associates. Mis delivery Weather compulsion Deliberate product contamination. Non payment of duties associated

Product Liability - Rating Factors • Indemnity Premium. • Indemnity limit Slab • Ratio of AOA to AOY • Export Multiplier • Turn over loading • Risk group (7) • Export Multiplier • Export Multiplier • USA and Canada (15) • OECD Countries (5) • Other countries including Non-OECD Countries (2) • Extensions

Directors and officers Liability Insurance ORIGIN • Common Law • Companies Act • Regulatory Authority

Directors & Officers Liability –Contd. Potential Claimants • Shareholders • Employees • Creditors • Customers • Competitors • Govt. & Regulatory Bodies • Members of the public

D & O LIABILITY ….Contd. BASIC DUTIES OF D & Os • Duty of Care and skill • Duty of fiduciaries • Duty of Disclosure

D & O LIABILITY ….Contd. The test of reasonable care is to ascertain whether the particular director has: behaved with reasonable care that an ordinary person would have behaved in the same circumstances The test of reasonable skill is to ascertain whether the particular director has: exercised reasonable care and skill that is expected of someone with similar knowledge and experience would have exercised in the same circumstances

D & O LIABILITY ….Contd. Fiduciary duties • Results from position of trust which directors hold with regard to the company. • Although not trustees in the legal sense, directors role is described as akin to the combined role of a trustee and an agent. • They should act in good faith in the best interest of the company, its employees etc. • To exercise their powers judiciously

D & O LIABILITY ….Contd. The policy covers Personal legal liability of D & Os arising from their: • Wrongful acts or omissions in the capacity as D&O of the company while discharging their duties of managing day to day affairs of the company. • The cover is available for past, present and future directors.

Directors & Officers Liability –Contd. Wrongful act shall include • Error, act of omission, commission or neglect • Mis-statement, misleading statement • breach of duty, breach of trust or breach of warranty of authority or • Other act done or wrongly attempted by the D&Os while the discharge of their duties, individually or collectively or any matter claimed against them solely by reasons of their being directors and/or officers of the company

Directors & Officers Liability--- Contd.. The indemnity provided under the policy • D & O’s legal liability to pay damages • Costs awarded against them and • Costs and expenses incurred by them with the consent of insurers in respect of • Investigation • Defense and • Settlement Of any claim and appeals there from • Arising out of • Prosecution (Criminal or otherwise) • Attendance at any official investigation or other proceedings ordered by any official body or • By reason of wrongful acts

Directors & Officers Liability –Contd. Exclusions • Dishonest or fraudulent acts • Personal profit/remuneration • Bodily injury/property damage • Pension funds • Fines & Penalties • Pollution • Professional indemnity • “Company vs. insured” and “insured vs. insured” • First party loss • Danger of collusion • Entrepreneurial risk

Professional Indemnity Insurance • Doctors and Medical Practitioners • Medical Establishments • Consulting Engineers, Architects and Interior Decorators • Chartered Accountants, Financial Accountants and Management Consultants • Lawyers, Advocates, Solicitors and Counsels

Professional Liability -- Contd. .. • A professional is vicariously liable for the negligence of his employees in the course of their employment • Liability may also arise under the Consumer Protection Act • Classification of Professional Risks • Resulting in bodily injuries (fatal or otherwise) – Eg: Doctors, Dentists etc. • Resulting in financial loss – Eg: Accountants, Solicitors etc. • Resulting in financial loss and/or bodily injury – Eg: Architect etc.

Professional Liability -- Contd. .. • Covers legal liability of the insured to third party • Arising from Errors and/or Omissions on the part of the insured • Whilst rendering professional services • Arising out of claims first made in writing against the insured during the policy period • Compensation includes payment of damages and defense cost and expenses incurred with the consent of the insurer • Subject always to the limits of Indemnity specified in the policy • Limit to be reduced by amounts paid under the policy • reinstatement of the indemnity limit not permitted

Professional Liability -- Contd. .. Exclusions • Criminal act or act in violation of law/ordinance • Deliberate non-compliance of any statute • Loss of pure financial nature such as loss of goodwill, loss of clientele etc. • Personal injuries such as libel, slander, mental injury, anguish or shock • Fines, penalties, punitive or exemplary damages • War or warlike situations • Nuclear radiation, contamination, explosion etc. • Services rendered under influence of intoxicating liquor or drugs

Carriers Legal Liability Policy • Covers legal liability of the road carriers to the cargo owners under the contract of affreightment • Basic Cover • Liability arising out of • Actual physical Loss/damage to goods • Directly caused by Fire, Explosion or Accidents to the carrying insured vehicle • Arising out of Negligence of the insured or criminal acts of his servants • Duration of Cover • Commences with the loading of goods onto the vehicle • Remains in force • until unloading of the goods at the discharging point or • Until expiry of 7 days after the first arrival of the vehicle at the destination town • Whichever occurs first

Carriers Legal Liability Policy • Liability • AOA • AOY • In addition, policy pays • Costs and expenses incurred with the consent of insurers in defending any claim made against the insured

Carriers Legal Liability Policy • Exclusions • Contractual liability other than legal liability • Damage/Loss to property owned by insured, his servants, sub-contractors and agents and property held under his control other than goods entrusted to him • Inherent defect or vice, insects, moths, mildew, mould, damp, wear and tear, deterioration, spontaneous combustion or decay of perishable goods • Depreciation, delay, loss of market and confisscation by a public authority • Consequential loss arising from loss or damage to goods • War, Strikes, Riots, Civil Commotion • Nuclear Risks • Act of God, Change of law, Action of Public Authority • Illicit, illegal, contaband, smuggled goods

Carriers Legal Liability Policy • Wider Cover to be issued on selective basis In addition to Basic Cover • Burglary • Riot, Strikes, Malicious Damage • Water Damage • Taint Damage • Breakage, Leakage, bad handling • Underwriting • Reputation of the carrier • Comprehensive Motor Insurance on Insured Vehicle throughout the currency of CLL policy • Road-worthiness of the insured Vehicle • Consignment Note as per IBA • Full Reinstatement of SI is permitted only once on settlement of claims • Single policy can be issued to cover all the vehicles owned/hired by the carrier

WISH YOU ALL THE BEST THANK YOU VERY MUCH