Download

1 / 35

350 likes | 582 Vues

Aggregate Supply. CHAPTER 11. © 2003 South-Western/Thomson Learning. Aggregate Supply in Short Run. Aggregate supply is the relationship between the price level in the economy and the aggregate output firms are willing and able to supply, with other things constant

E N D

Aggregate Supply CHAPTER 11 © 2003 South-Western/Thomson Learning

Aggregate Supply in Short Run • Aggregate supply is the relationship between the price level in the economy and the aggregate output firms are willing and able to supply, with other things constant • Assumed constant along a given aggregate supply curve are • Resource prices • State of technology • Set of formal and informal institutions that structure production incentives

Labor and Aggregate Supply • Labor is the most important resource, accounting for about 70% of production costs • The supply of labor in an economy depends on • The size and abilities of the adult population, and • Household preferences for work versus leisure

Labor and Aggregate Supply • Along a given labor supply curve, the quantity of labor depends on the wage rate the higher the wage, other things constant, the more people are willing and able to work • However, the purchasing power of any given nominal wage depends on the economy’s price level

Labor and Aggregate Supply • The higher the price level, the less any given money wage will purchase and the lower the price level, the more any given money wage will purchase • Because the price level matters, we must distinguish between the nominal wage and the real wage • Nominal wage measures the wage in current dollars • Real wage measures the wage in constant dollars dollars measured by the goods and services they will buy

Real and Nominal Wages • All resource suppliers, including labor, must reach agreement based on the expected price level • Wage agreements may be either explicit or implicit • Explicit agreements would be those based on a labor contract • Implicit agreements would be those based on labor market practices

Potential Output • If these price-level expectations are realized, the agreed-upon nominal wage translates into the expected real wage • When the actual price level turns out as expected, the resulting level of output is referred to as the economy’s potential output • Potential output is the amount produced when there are no surprises associated with the price level

Potential Output • Potential output can be thought of as the economy’s maximum sustainable output level, given the • Supply of resources • State of technology • Formal and informal production incentives • Often referred to by other terms • Natural rate of output • Full-employment rate of output

Natural Rate of Unemployment • Natural rate of unemployment • The unemployment rate that occurs when the economy is producing its potential GDP • The rate that prevails when cyclical unemployment is zero • The number of job openings is equal to the number unemployed for frictional, structural, and seasonal reasons • Estimates of the natural rate range from about 4 to 6% of the labor force

Actual Price Higher than Expected • Since the prices of many resources are fixed for the duration of the contract, firms welcome a price level higher than expected • Their selling price (thus revenue) of their products, on average, are higher than expected, while the costs of at least some of the resources remain constant firms have an incentive in the short run to expand production beyond the economy’s potential level

Actual Price Higher than Expected • Even in an economy producing its potential output, there is some unemployed labor and unused production capacity • Potential GDP can be thought of as the economy’s normal capacity • Firms and workers are able, in the short run, to push output beyond the economy’s potential

Why Costs Rise • As output expands above potential GDP, the cost of producing this additional output increases • Additional workers are harder to find • Some workers may not be properly prepared • The prices of those resources purchased in markets where prices are flexible will increase reflecting their increased scarcity • Firms use their capital resources more intensively

Why Costs Rise • However, because the prices of some resources are fixed by contracts, the price level rises faster than the per-unit production cost firms find it profitable to increase the quantity supplied • When the actual price level exceeds the expected price level, the real value of an agreed-upon nominal wage declines

Summary • If the price level is higher than expected, firms have a profit incentive to increase the quantity of goods and services supplied • At higher rates of output, however, the per-unit cost of additional output increases • Firms will expand output as long as the revenue from additional production exceeds the cost of the production

Actual Price Lower than Expected • Production is less attractive to firms because the prices they receive for their output are on average lower than they expected • However, many of their production costs, such as the nominal wage, do not fall production is less profitable than expected firms reduce their quantity supplied the economy’s output is below its potential

Actual Price Lower than Expected • As a result, some workers are laid off and capital resources go unused • In this case, some costs decline when output falls below the economy’s potential • As output falls, some resources become unemployed

Summary • If the price level is higher than expected • Firms increase the quantity supplied beyond the economy’s potential • The per-unit cost of additional production increases • If the price level is lower than expected • Firms reduce output below the economy’s potential output • Prices fall more than costs

Short-Run Aggregate Supply Curve • What what have just described can be used to trace out the short-run aggregate supply curve – SRAS • SRAS shows the relationship between the actual price level and real GDP supplied, other things constant • The short run is the period during which some resource prices are fixed by either explicit or implicit agreement

Exhibit 1:Short-Run Aggregate Supply Curve Potential output SRAS 130 The expected price level is 130; the SRAS is based on that expected price level. 140 l e v e l 130 a e c If the price level turns out to be 130 as expected, producers supply the economy’s potential level of output, $10.0 trillion. i r P 120 0 10.0 Real GDP (trillions of dollars)

Potential output SRAS 130 140 l e v e l 130 a e c i r P 120 0 10.0 Real GDP (trillions of dollars) Exhibit 1: Short-Run Aggregate Supply Curve The short-run aggregate supply becomes steeper as output increases because resources become more costly as output increases

b 135 AD 10.2 Exhibit 2: Expansionary Gap Potential output SRAS 130 140 Price level 130 a 0 10.0 Real GDP (trillions of dollars) Expansionary gap

SRAS 140 c 140 b 135 AD 10.2 Expansionary gap Exhibit 2: Expansionary Gap Potential output Price level SRAS 130 130 a 0 10.0 Real GDP (trillions of dollars)

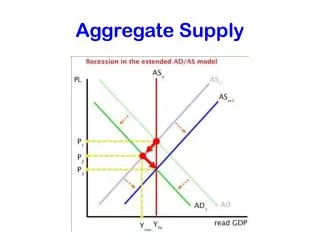

Exhibit 3: Contractionary Gap Potential output SRAS 130 130 a Price level d 125 e 120 AD 9.8 10.0 0 Contractionary gap

Exhibit 3: Contractionary Gap Potential output SRAS 130 SRAS 120 130 a Price level d 125 e 120 AD 9.8 10.0 0 Contractionary gap

Contractionary Gap • The key to closing a contractionary gap is the flexibility of wages and prices • If wages and prices are not very flexible, they will not adjust very quickly to a contractionary gap shifts in the short-run aggregate supply curve may occur slowly the economy can be stuck at an output and employment level below its potential

Long-Run Aggregate Supply • The long-run aggregate supply curve, LRAS, depends on the • supply of resources in the economy • level of technology • production incentives provided by the formal and informal institutions of the economic system • As long as wages and prices are flexible, the economy’s potential GDP is consistent with any price level

b 140 c 120 AD' AD'' Exhibit 4: Long-Run Aggregate Supply Curve The initial price level of 130 is determined by the intersection of AD with the long-run aggregate supply curve. Potential output LRAS a 130 Price level AD 10.0 Real GDP (trillions of dollars) 0

Wage Flexibility and Employment • An expansionary gap creates a labor shortage that eventually results in a higher nominal wage and a higher price level • A contractionary gap does not necessarily generate enough downward pressure to lower the nominal wage, e.g., that is, nominal wages are slow to adjust to high unemployment they tend to be sticky in the downward direction

Wage Flexibility and Employment • However, an actual decline in the nominal wage is not necessary to close a contractionary gap • All that is needed is a fall in the real wage • The real wage will fall as long as the price level increases more than the nominal wage

Increases in Aggregate Supply • The economy’s potential output is based on the • willingness and ability of households to supply resources to firms which can be caused by a change • in the size, composition, or quality of the labor force • in household preferences for labor versus leisure • level of technology • institutional underpinnings of the economic system

Exhibit 6: Change in the Supply of Resources A gradual increase in the supply of resources increases the potential level of real GDP the long run aggregate supply curve shifts from LRAS to LRAS' LRAS LRAS' l e v e l e c i r P Real GDP 0 10.0 10.5 (trillions of dollars)

Supply Shocks • Supply shocks are unexpected events that change aggregate supply, sometimes only temporarily • Beneficial supply shocks increase aggregate supply; examples include • Abundant harvests that increase the supply of food • Discoveries of natural resources • Technological breakthroughs that allow firms to combine resources more efficiently • Sudden changes in the economic system that promote more production

LRAS' SRAS 125 125 b 10.2 Exhibit 7: Beneficial Supply Shock Here, the beneficial supply shock is assumed to be a technological breakthrough, which shifts the SRAS from SRAS130 to SRAS125 and the long-run aggregate supply curve from LRAS to LRAS´. LRAS SRAS 130 Price level 130 a Thus, for a given aggregate demand curve, a beneficial supply shock leads to an increase in output and a decrease in the price level. AD 0 10.0 Real GDP (trillions of dollars)

Decreases in Aggregate Supply • Adverse supply shocks are sudden, unexpected events that reduce aggregate supply, again sometimes, only temporarily • Drought could reduce the supply of a variety of resources • Government instability • Terrorist attacks

LRAS'' SRAS 135 c 135 9.8 Exhibit 8: Adverse Supply Shock The adverse supply is shown as the leftward shift of both the short and long-run aggregate supply curves with the result that the price level increases and the level of output declines stagflation as equilibrium moves from point a to point c LRAS SRAS l 130 e v e l e c i r P a 130 AD 0 10.0 Real GDP (trillions of dollars)