Download

1 / 39

580 likes | 1.11k Vues

Understanding the Financial Planning Process . Chapter 1. Why is Financial Planning Important?. What are the Rewards of Sound Financial Planning?. Best way to achieve your financial objectives Maintain & improve standard of living Control spending in order to live well today & tomorrow

E N D

What are the Rewards of Sound Financial Planning? • Best way to achieve your financial objectives • Maintain & improve standard of living • Control spending in order to live well today & tomorrow • Accumulate wealth

Standard of Living The necessities, comforts, and luxuries we have or desire

What Determines Our Quality of Life? • Wealth is the primary determinant • Other factors • Geographic location • Public facilities • Local cost of living • Pollution • Traffic • Population density

The Two-Income Family • Has a profound effect on our standard of living • Was relatively rare in the early 1970s • Has become commonplace today • 75% of married adults say they and their mate share all their money • Requires greater responsibility to manage the money wisely

Spending Money Wisely • Major benefit of financial planning • Determining your current and future spending patterns is important • Goal is to plan to spend your money to get the most satisfaction

Current Needs • Current spending level is based on necessities of life and your average propensity to consume • Minimum level of spending allows you to obtain only the necessities of life: food, clothing, and shelter

Average Propensity to Consume The percentage of each dollar of income that is spent, on average, for current needs rather than savings. What is your average propensity to consume? Income spent on current needs Total income

Average Propensity to Consume • Ultraconsumers choose to splurge on a few items and scrimp elsewhere. • These people also exhibit high average propensities to consume. • Other individuals who earn large amounts quite often have low average propensities to consume because necessities represent only a small portion of their income.

Future Needs • Set aside a portion of current income for deferred, or future spending • Build up a retirement fund • Save for a child’s education • Save to buy a home • Save for a car • Defer actual spending until the future

Accumulating Wealth • Wealth is • Function of the total value of all the items a person owns • Consists of financial and tangible assets • Financial assets – intangible, paper assets, such as a savings account • Tangible assets – physical assets, such as real estate • Goal of most people is to accumulate as much wealth as possible while maintaining desirable standard of living

What is Personal Financial Planning? • Not only for the wealthy • Taking conscientious and systematic steps toward financial goals • Knowing what you need to accomplish financially • Knowing how you intend to accomplish it • How to be Financially Successful

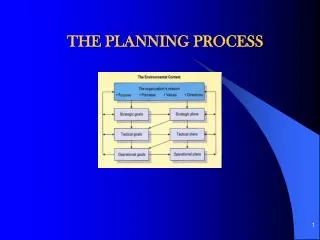

Steps in the Financial Planning Process 1. Define financial goals 2. Develop plans

1. Define financial goals 2. Develop plans 3. Implement plans 4. Develop budgets • FINANCIAL ACTIONS • Asset decisions • Credit decisions • Insurance decisions • Investment decisions • Retirement and • estate decisions

1. Define financial goals 2. Develop plans 3. Implement plans 4. Develop budgets • FINANCIAL ACTIONS • Asset decisions • Credit decisions • Insurance decisions • Investment decisions • Retirement and • estate decisions Prepare financial statements 5. Evaluate results 6. Revise plans

The Role of Money • Money is the common denominator by which all financial transactions are gauged • Money is the medium of exchange • Money is the main consideration in establishing financial goals • It is not money that most people want

The Utility of Money • Utility is the amount of satisfaction a person receives from purchasing something • People may choose one item over another because of a special feature that provides additional utility • Example iPhone vs. TracFone • The added utility may result from actual usefulness or from “status”

Psychology of Money • Your personal value system will also shape your attitude toward money • For every 76 Americans who believe that money can’t buy happiness, one believes that it does • Can money buy happiness? • Key to effective financial planning is a realistic understanding of the role of money and its utility in the individual’s life • Effective financial plans are both economically and psychologically sound

Money and Relationships • Money can be one of the most emotional issues in any relationship • Learning to communicate with your partner about money is a critical step in developing effective financial plans • Best way to resolve money disputes is to be aware of your partner’s financial style

Financial Goals • Cover a wide range of financial desires • Should be realistic and attainable • Be specific in defining goals & focus on results • Involve family members & enlist their cooperation • Prioritize goals & set a definite time frame

Put Target Dates on Financial Goals • Long-Term Goals • Should indicate desires for a time period covering about 6 to 30 or 40 years • May be difficult to pinpoint but important to establish tentative ones • Short-and Intermediate-Term Goals • Short-term covers a 12-month period • Short-term should include establishing an emergency fund with 3-7 months’ income • Intermediate-term goals bridge gap between short- and long-term goals • Unless you attain your short-term goals, you probably won’t achieve your intermediate- or long-term goals

The Life Cycle of Financial Plans Financial planning is a dynamic process Needs and goals change through different stages of your life With careful planning, you can get through tough times and prosper in good times

Benefit of Planning • Your money works more efficiently for you by... • Utilizing the financial wonder-- The power of compounding through time!

Growth of $1000 at 10% interest: 45,259 21,725 Years

Using the Personal Computer • Prepare financial statements • Plan retirement • Prepare and file tax returns • Track investments • Analyze needs

The Planning Environment • Your purchase, saving, investment, and retirement plans and decisions are influenced by both the present and future state of the economy • A strong economy can lead to big profits in the stock market which can positively affect your investment and retirement programs • The economy can also affect the interest rates you pay on your mortgage and credit cards as well as savings accounts

The Players • Government • Taxation—changes in tax rates and procedures will increase or decrease consumer income • Regulation—take into consideration legal requirements that protect consumers and those that constrain their activities • Business • Provides consumers with goods and services. To produce them, firms hire labor and use land and capital • Consumers • Choice of whether to spend or save has a direct impact on the present and future circular flow of money

The Economy • Influenced by interaction between government, business, consumers and world conditions

Government Policy Decisions • Provide economic stability • Maintain acceptable employment levels

Government Policy Decisions Monetary Policy • Controls money supply • Used to stimulate or contract economic growth • Federal Reserve Fiscal Policy • Controls levels of taxation • Sets levels of government spending on various programs

Economic Cycles • The upward and downward movement of the economy • Expansion--high levels of employment and production; strong economy • Recession—decline lasts more than 6 months • Depression—recession worsens to point where economic growth is almost at a standstill • Recovery—increasing levels of employment and production; follows either a recession or a depression

Economic Cycles Levels of Employment and Production HIGH LOW Expansion Recession Depression Recovery

Inflation, Prices, and Planning • Affects not only what we pay but also what we earn • As prices rise purchasing power (amount of goods & services we can buy with our dollars) declines • Affects financial plan & goals

What Determines your Income? • Demographics • Typically people with lowest income are very young or very old • People with highest income are 46-65 • Education • Solid formal education greatly enhances earning power • Where You Live • Salaries vary regionally—higher in Northeast and West • Salaries higher in metropolitan areas • Your Career • Career planning and personal financial planning are closely related activities; the decisions you make in one area affect the other