Download

1 / 64

680 likes | 871 Vues

Federal Retirement Pre-Retirement Counseling. Sonny Barber - USDA Becky Priebe – Washington State Mary Fran San Soucie – Montana State. OPM Advice Five years out. OPM advises them to see you

E N D

Federal Retirement Pre-Retirement Counseling Sonny Barber - USDA Becky Priebe – Washington State Mary Fran San Soucie – Montana State

OPM AdviceFive years out • OPM advises them to see you • Must carry health continuously for 5 years prior to retirement (or during all federal employment since 1st opportunity to enroll) in order to be eligible to carry it into retirement • Must begin annuity within 30 days, unless under certain provisions of FERS • Health insurance years of service can be waived, but rare

OPM AdviceFive years out • Life Insurance - Basic • Must have coverage when you retire • Must not have converted to an individual policy • Must begin annuity within 30 days (again, some exceptions with FERS) • Must have been insured under FEGLI for the 5 years preceding retirement or the full periods(s) of service when coverage available

OPM AdviceFive years out • Life insurance – Optional • Can keep if eligible to continue basic AND • Covered by optional for 5 years immediately preceding retirement of full periods of service when coverage available, if less than five years. These life insurance qualifications may not be waived

OPM AdviceFive years out • Review Service history • Can make corrections for previous service or military service. • Will be able to make deposits and/or re-deposits • Must make military deposits before you retire

OPM – AdviceFive Years Out • Check eligibility for Social Security • Government Pension Offset • Windfall Elimination Provision

OPM AdviceOne year out • Confirm eligibility • Decide WHEN to retire • Get info about other benefits: • TSP • Social Security • Foreign Service • Pensions from Private Industry • IRAs • Other Life Insurance

OPM AdviceOne year out • Review OPF with Personnel Officer to be sure: • All is correct • All service is verified • Insurance coverage documented

OPM AdviceOne year out • Review OPF • Employment dates correct • Salary amounts correct • Salary change dates correct • Part time service correct • Military service correct

OPM AdviceOne year out • Check Designations of Beneficiary • If no designation, retirement lump sum paid in following order: • Your widow or widower. • Your children in equal shares. • Your parents in equal shares. • Your appointed executor or administrator of your estate. • Your next of kin under the laws of the state you reside in when you die.

OPM AdviceSix months out • Resolve debts to employer • Waive Military Retired Pay • IF you want to receive credit for military service • Defense Finance and Accounting ServiceU.S. Military Retirement PayP.O. Box 7130London, KY 40742-7130 • You can "fax" your request to 1 (888) 469-6559

OPM AdviceSix months out • Eligibility for Medicare • Need to contact SSA at least 3 months before your 65th birthday • If info incorrect, will need to supply them with info • You should provide the following information in your request: • your name, as shown on your payroll records; • date of birth; • Social Security Number; • mailing address; • years for which earnings are needed; • name and location of employer for each year; • reason for request; • written signature; and, • a statement that all other sources of information have been exhausted.

OPM AdviceTwo months out • Choose your retirement Date • Complete your retirement application • If you performed military service after 1956, check on military service deposit • Request direct deposit of your annuity checks • Work on TSP withdrawal options (can take 2-3 months to process)

Types of Retirement Systems at Podunk U • State Retirement System (TRS) • TIAA-CREF (maybe?) • Civil Service Retirement System (CSRS) and CSRS-Offset • Federal Employees’ Retirement System (FERS) • Public Employee’s Retirement System (PERS) – typically classified employees

Civil Service Retirement System (CSRS) • Defined Benefit Plan • Contribution rates Employee Employer 0.07 0.07

CSRS Retirement Eligibility AGE is at least... and CREDITABLE SERVICE is at least.. 62 5 years 60 20 years 55 30 years Military service can be included Unused sick leave is included

CSRS benefit determination 1st 5 years of service x hi-3 average salary x 0.015 - -plus- - 2nd 5 years of service x hi-3 average salary x 0.0175 - -plus- - Remainder years of service x hi-3 average salary x 0.02

CSRS Monthly Benefit Options • Full annuity – nothing to survivors • Full survivor annuity • reduction of less than 10% to annuitant • 55% of full survivor benefit to survivor • Partial survivor annuity • Reduction to retiree’s annuity based upon survivor annuity • Can be any amount between zero and full survivor annuity

CSRS Monthly annuity options • Must have some survivor annuity in order for survivor to receive federal health benefits after death of retiree • Does not have to cover health insurance premium amount

Federal Employees’ Retirement System (FERS) • Defined Benefit plan • Contribution rates: Employee Employer 0.008 .112

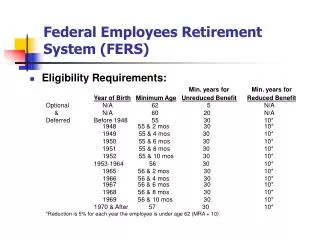

FERS Retirement Eligibility Age Years of Service 62 5 60 20 MRA 30 MRA 10 If you retire at the MRA with at least 10, but less than 30 years of service, your benefit will be reduced by 5 percent a year for each year you are under 62, unless you have 20 years of service and your benefit starts when you reach age 60 or later.

FERS Retirement EligibilityMinimum Retirement Age (MRA) If you were born Your MRA is Before 1948 55 In 1948 55 and 2 months In 1949 55 and 4 months In 1950 55 and 6 months In 1951 55 and 8 months In 1952 55 and 10 months In 1953 through 1964 56 In 1965 56 and 2 months In 1966 56 and 4 months In 1967 56 and 6 months In 1968 56 and 8 months In 1969 56 and 10 months In 1970 and after 57

FERS benefit determination Hi-3 Average Salary x 1% (1.1% if over age 62 and at least 20 years of service) x Number of years of service (Plus TSP and Social Security)

FERS Monthly Benefit Options • Full annuity – nothing to survivor • Full survivor annuity • 10% reduction to retiree’s annuity • Survivor receives 50% of retiree’s annuity • Partial Survivor annuity • 5% reduction to retiree’s annuity • Survivor receives 25% of retiree’s annuity

FERS Monthly annuity options • Must have some survivor annuity in order for survivor to receive federal health benefits after death of retiree • Does not have to cover health insurance premium amount

When to apply • Three day rule • If apply last day of the month, or during the first three days of the month, annuity begins the next day. • Otherwise, begins beginning of next month.

What happens when you apply • We send info on to OPM • OPM uses our annuity calculation to low-ball an annuity payment, which they send to you shortly thereafter (2-3 weeks) • After a month or more, they make a final determination of your annuity, and they adjust the payment

Social Security and CSRS annuity • Windfall Elimination Provision (WEP) • Why? • Social Security benefits are intended to replace only a percentage of a worker’s pre-retirement earnings. The way Social Security benefit amounts are figured, lower-paid workers get a higher return than highly paid workers. • Congress passed the Windfall Elimination Provision to remove that advantage.

WEP • If you paid Social Security tax on 30 years of substantial earnings you are not affected by the Windfall Elimination Provision (WEP). • There is a chart that shows the maximum monthly amount your benefit can be reduced because of WEP if you have fewer than 30 years of substantial earnings. (To calculate your WEP reduction, please use our WEP Online Calculator or download our Detailed Calculator.)

Websites for WEP • http://www.socialsecurity.gov/retire2/wep.htm • http://www.socialsecurity.gov/pubs/10045.html • http://www.socialsecurity.gov/pubs/10045.pdf

What comes out of your annuity check • Taxes – can have state taxes taken out, too, if your state participates in this • Health insurance premiums (same as before retirement) • Life insurance premiums (options on this) • Preference is direct deposit – have to “opt out”

Federal Taxes on Annuity • “Olden days” • Only deducted taxes AFTER your contributions ran out • Olden days are over • Now • Use “Simplified Formula” to determine tax base • IRS Publication 721 (www.irs.gov)

Federal Health Benefits Post-ret • OPM picks up Employer Share, so no huge changes to retiree • NARFE has great publications about Medicare options (http://www.narfe.org) • Various Life Insurance Options • Extension Personnel office (or whatever your state does) works with each retiree to discuss options

Life insurance options after retirement • BASIC • No reduction after age 65 • Big premiums upon retirement – less expensive at 65 • 50% reduction after age 65 • Less big premiums upon retirement – less expensive at 65 • At age 65, 2%/month reduction of life insurance to 50% reduction (i.e., $40,000 to $20,000) • 75% reduction after age 65 • Regular premiums only upon retirement – FREE after age 65! • At age 65, 2%/month reduction to 75% reduction ($40,000 to $10,000)

Life insurance - Optional • Plan A • reduce by 2% per month beginning the second month after you are 65 or the second month after you retire, whichever is later, until it reaches 25% of the face value ($2,500). • Premiums for Option A insurance from your annuity will be withheld through the end of the month in which you are 65, unless you elect to cancel this coverage.

Life Insurance - Optional • Option B • Elect how many of your Option B multiples would continue in retirement and whether — at age 65 — multiples will continue at their full value or will gradually reduce to zero. • At retirement and age 65, the annuitant may elect either Full Reduction or No Reduction for each separate multiple of Option B. For example, a person with five multiples may elect No Reduction on two multiples, while the three remaining multiples reduce fully. • If you elect Full Reduction or if you separated for retirement before April 24, 1999, effective the first day of the second month after you reach age 65 or the first day of the second month after you retire, whichever is later, your Option B full-reduction multiples will reduce by 2% of the face value per month for 50 months, at which time this coverage will end.

Life Insurance - Optional • Option C • Elect how many of your Option B multiples would continue in retirement and whether — at age 65 — multiples will continue at their full value or will gradually reduce to zero. • At retirement and age 65, the annuitant may elect either Full Reduction or No Reduction for each separate multiple of Option B. For example, a person with five multiples may elect No Reduction on two multiples, while the three remaining multiples reduce fully. • If you elect Full Reduction or if you separated for retirement before April 24, 1999, effective the first day of the second month after you reach age 65 or the first day of the second month after you retire, whichever is later, your Option B full-reduction multiples will reduce by 2% of the face value per month for 50 months, at which time this coverage will end.

COLA for Retirement Annuity • To get the full COLA, a retiree or survivor annuity must have begun no later than December 31, 2006. If not, the increase is prorated under both plans. Prorated accounts receive one-twelfth of the increase for each month they received benefits. For example, if the benefit commenced November 30, 2007, the prorated COLA would be one-twelfth of the full COLA.

Medicare Part B • Q. Do I Have to Take Part B Coverage? • A. You don't have to take Part B coverage if you don't want it, and your FEHB plan can't require you to take it. There are some advantages to enrolling in Part B: • You have the advantage of coordination of benefits (described later) between Medicare and your FEHB plan, reducing your out-of-pocket costs. • Your FEHB plan may waive its copayments, coinsurance, and deductibles for Part B services. • Some services covered under Part B might not be covered or only partially covered by your plan, such as orthopedic and prosthetic devices, durable medical equipment, home health care, and medical supplies (check your plan brochure for details). • You may go outside of the plan's network for Part B services and receive reimbursement by

Medicare Part B • Q. How Much Does Part B Coverage Cost? • A. The standard monthly premium for Medicare Part B in 2007 increased to $93.50 from $88.50. Effective January 1, 2007, the government started determining the Medicare Part B premium based on a person’s income. Higher-income beneficiaries for the first time will pay a higher monthly premium than other beneficiaries, as ordered by a provision in the 2003 Medicare law.

Medicare Part B • Q. What Happens If I Don't Take Part B as Soon as I'm Eligible? • A. You must wait for the general enrollment period (January 1 - March 31 of each year) to enroll, and Part B coverage will begin the following July 1. Your Part B premiums will go up 10 percent for each 12 months you could have had Part B but didn't take it. • If you didn't take Part B at age 65 because you were covered under FEHB as an active employee (or you were covered under your spouse's group health insurance plan and he/she was an active employee), you may sign up for Part B (generally without increased premiums) within 8 months from the time you or your spouse stop working or are no longer covered by the group plan. You also can sign up at any time while you are covered by the group plan.

Helpful websites • Medicare • http://www.opm.gov/insure/HEALTH/medicare/index.asp • http://www.opm.gov/insure/HEALTH/medicare/medicare02.asp • http://www.medicare.gov/ • http://www.csrees.usda.gov/about/human_res/cesguide/medicare.html • Social Security • http://www.ssa.gov • Other issues for Former Schedule A appointees • http://www.csrees.usda.gov/about/human_res/cesguide/ceshr_index.html

VEBA – some states have this • Voluntary Employees’ Beneficiary Association • Authorized by Internal Revenue Code Section 501(c)(9) • Your sick leave payout goes into your account, tax-free • You use this pre-tax account to pay for out-of-pocket medical expenses • Internal Revenue Code Section 213(d)

What to do with Annual Leave Payout • May be able to go to any of several providers’ plans for tax exemption • Aetna, MetLife, TIAA-CREF, T. Rowe Price, Valic- AIG (403(b) plans), State Deferred Comp (457 plan), etc. • Election MUST be done prior to last day • Tax-defers annual leave payout • Can get lump sum payout – tax implications

Who to contact with ANY questions • HR people • ###-#### • you@podunk.edu • HR people • ###-#### • you2@podunk.edu