Download

1 / 3

30 likes | 35 Vues

An association must perceive the particular fraud risks that could compromise its monetary, operational and brand solidness. An organized extortion fraud risk helps the executives in understanding its specific fraud risks and empowers it to oversee them adequately.<br>

E N D

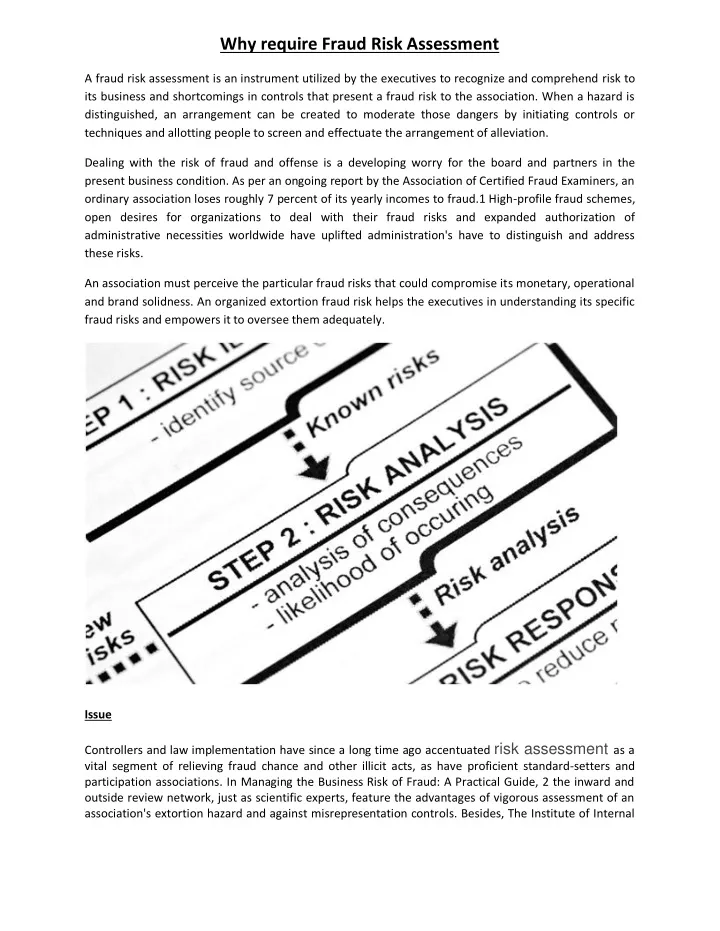

Why require Fraud Risk Assessment A fraud risk assessment is an instrument utilized by the executives to recognize and comprehend risk to its business and shortcomings in controls that present a fraud risk to the association. When a hazard is distinguished, an arrangement can be created to moderate those dangers by initiating controls or techniques and allotting people to screen and effectuate the arrangement of alleviation. Dealing with the risk of fraud and offense is a developing worry for the board and partners in the present business condition. As per an ongoing report by the Association of Certified Fraud Examiners, an ordinary association loses roughly 7 percent of its yearly incomes to fraud.1 High-profile fraud schemes, open desires for organizations to deal with their fraud risks and expanded authorization of administrative necessities worldwide have uplifted administration's have to distinguish and address these risks. An association must perceive the particular fraud risks that could compromise its monetary, operational and brand solidness. An organized extortion fraud risk helps the executives in understanding its specific fraud risks and empowers it to oversee them adequately. Issue Controllers and law implementation have since a long time ago accentuated risk assessment as a vital segment of relieving fraud chance and other illicit acts, as have proficient standard-setters and participation associations. In Managing the Business Risk of Fraud: A Practical Guide, 2 the inward and outside review network, just as scientific experts, feature the advantages of vigorous assessment of an association's extortion hazard and against misrepresentation controls. Besides, The Institute of Internal

Auditors' Standard 2120. A2 requires inside reviewers to assess the potential for the event of misrepresentation and how the association oversees fraud chance. Point of View Fraud risk assessment is a fundamental segment in helping associations to secure their kin, resources, notorieties and primary concerns. Notwithstanding meeting prescriptive direction, administrative prerequisites and investor desires, fraud risk evaluation gives a valuable and spending well disposed methods by which to all the more likely comprehend and address budgetary and operational weaknesses before they emerge into exorbitant fake or illicit acts. Risk Assessment Guidelines The evaluation ought to be performed or refreshed intermittently because of changes in: • Internal procedures and controls. • Organizational structure. • Segregation of obligations among different faculty. The extortion hazard appraisal should address: • Asset misappropriation. • Financial and non-budgetary announcing. • Regulatory consistence territories. • Illegal acts. Extortion Risk Assessment Components • Description of fraud or plans: Examples incorporate fake payment, undisclosed connections/related gatherings, robbery by digital misrepresentation, income acknowledgment, pay off, control of liabilities and costs, bogus worker capabilities or accreditation, consistence with government guidelines, wrong diary passages, inappropriate announcing and revelations, burglary of benefits or administrations • Identification of existing enemy of extortion controls: Internal controls in actuality, preventive or criminologist controls. • Likelihood of event: Based on recurrence – uncommon to extremely visit – or likelihood of event – far off to practically certain. • Significance to the association: Incidental to cataclysmic.

• Assessment of control viability: Ineffective to powerful. • Fraud hazard reaction: Additional controls or restorative activity exercises proposed to be executed. • Responsible individual: To execute controls and relief endeavours. • Monitoring exercises: To be occasionally directed and recurrence of event.