Download

1 / 10

100 likes | 182 Vues

Chapter 36: Other Security Devices. Suretyship vs. Guaranty. Suretyship and guaranty undertakings both promise to answer for the debt or default of another, but are not the same. A surety is equally liable for the debtor’s debt.

E N D

Suretyship vs. Guaranty • Suretyship and guaranty undertakings both promise to answer for the debt or default of another, but are not the same. • A surety is equally liable for the debtor’s debt. • A guarantor of collection is ordinarily only secondarily liable, which means that the guarantor does not pay until the creditor has exhausted all avenues of recovery.

Absolute Guaranty • If the guarantor has made an absolute guaranty, then its status is the same as that of a surety. • Both are liable for the debt in the event the debtor defaults, regardless of what avenues of collection, if any, the creditor has pursued.

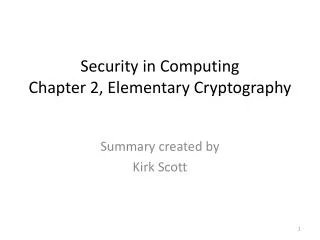

Creditor Creditor Debtor/Principal Absolute Guaranty Debtor/Principal Surety Creditor Debtor/Principal Guaranty Suretyship and Guaranty Surety and Absolute Guaranty are both liable to the creditor immediately upon the debtor’s default. A (non-absolute) Guaranty is liable only after the creditor has exhausted all options for collecting from the debtor.

Rights and Defenses of Sureties • Sureties have a number of rights to protect them. They are: • Exoneration, • Subrogation, • Indemnity, and • Contribution. • Sureties also have certain defenses: • Ordinary contractdefenses • Some defenses peculiar to suretyship, such as release of collateral, change in loan terms, substitution of debtor, and fraud by the creditor.

1. Fraud by Debtor 2. Misrepresentation by Debtor 3. Changes in Loan Terms (e.g., extension of payment, compensated surety) 4. Release of principal Debtor 5. Bankruptcy of Principal Debtor 6. Insolvency of Principal Debtor 7. Death of Principal Debtor 8. Incapacity of Principal Debtor 9. Lack of Enforcement by Creditor 10. Creditor’s Failure to Give Notice of Default 11. Failure of Creditor to Resort to Collateral No Release of Surety

1. Proper Performance by Debtor 2. Release, Surrender, or Destruction of Collateral (to extent of value of collateral) 3. Substitution of Debtor 4. Fraud/Misrepresentation by Creditor 5. Refusal by Creditor to Accept Payment from Debtor 6. Change in Loan Terms (uncompensated surety only) 7. Statute of Frauds 8. Statute of Limitations Release of Surety

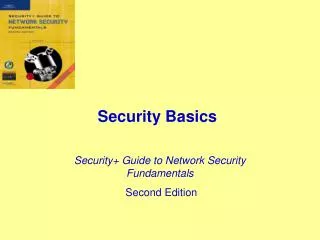

ABC Bank 2038 First Avenue Camden, NJ 08101 October 7 , 19 98 Issuer Letter #3133 For: John Hoskins 14 Smith Lane _ _ _ , _ _ By order of: Jan Kent Kent Products, Inc. 1503 Lee Blvd. Camden, NJ 08101 Beneficiary;Drawer of DraftsUnder the Letter of Credit Customer of Issuer ABC Bank has established in your favor an irrevocable letter of credit up to an amount of $400,000 (four hundred thousand dollars) available by your drafts on or before [date] accompanied by a bill of lading showing shipment of [identify goods] by you to [name and address of buyer] by [identify carrier], an invoice covering such shipment, and an insurance policy providing [state coverage] of the goods for the benefit of [name of insured]. ____________________________ ABC Bank Manager Letter of Credit

Letters of Credit • A letter of credit is a three-party agreement that the issuer (usually a bank) will pay drafts drawn by the beneficiary of the letter. • The parties to a letter of credit are the issuer, the customer who makes the arrangement with the issuer, and the beneficiary, who will be the drawer of the drafts. • The letter of credit continues for any time it specifies.

Letters of Credit (cont’d) • The letter of credit must be in writing and signed by the issuer. • Consideration is not required to establish or modify a letter of credit. • If the conditions in the letter of credit have been complied with, the issuer is obligated to honor drafts drawn under the letter of credit.