Download

1 / 10

110 likes | 306 Vues

PRINCIPIOS DE COSTOS. CLASE 22 DE MARZO https://www.youtube.com/watch?v=QDEU-7PyOJk. INTRODUCCIÓN. CONTABILIDAD DE EMPRESAS COMERCIALIZADORAS: CONTABILIDAD DE EMPRESAS MANUFACTURERAS:. ESTADOS FINANCIEROS.

E N D

PRINCIPIOS DE COSTOS CLASE 22 DE MARZO https://www.youtube.com/watch?v=QDEU-7PyOJk

INTRODUCCIÓN • CONTABILIDAD DE EMPRESAS COMERCIALIZADORAS: • CONTABILIDAD DE EMPRESAS MANUFACTURERAS:

ESTADOS FINANCIEROS • Son la base para la toma de decisiones, de allí la importancia de calcular el costo de la forma mas apropiada ya una gestión eficiente de los recursos genera mayores ingresos para la empresa. Veamos el estado de resultados de la empresa Colceramica, revisemos porcentualmente cuanto representan los costos en los ingresos para el año 2012

Compañía Colombiana de cerámica Colceramica S.A Podemos observar que en este estado de resultados que el costo representa el 61% de los ingresos. Por esta razón el comportamiento de los costos es tan decisivo para una empresa, de allí su importancia para la toma de decisiones.

EMPRESA COMERCIALIZADORA MERCANCIA NO FABRICADA POR LA EMPRESA PRINCIPAL COSTO ES VR MCIA Y EL FLETE

EMPRESA MANUFACTURERA • CALIZAS MATERIA PRIMA • CLINKER PROD. EN PROCESO • CEMENTO PROD. TERMINADO

EL COSTO EL PROTAGONISTA • SON EROGACIONES RELACIONADAS CON MOTIVO DE LA PRODUCCIÓN DE BIENES, EL OBJETIVO ES CALCULAR EL COSTO UNITARIO DEL BIEN.

COSTO Y GASTO • PLANTA OFICINAS

ELEMENTOS DEL COSTO ¿Qué SE REQUIERE? • MATERIALES • MANO DE OBRA DIRECTA • COSTOS INDIRECTOS DE FABRICACIÓN

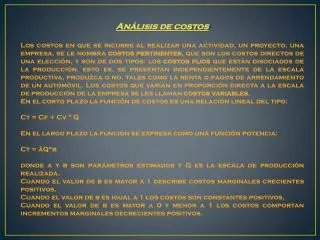

COSTO EN RELACIÓN CON EL PRODUCTO • Directos • Indirectos LA PRODUCCIÓN • Variable • Fijo • Mixto