Download

1 / 28

440 likes | 1.28k Vues

The American Options. Chapter 4: ADVANCED OPTION PRICING MODEL. The American Options.

E N D

The American Options Chapter 4: ADVANCED OPTION PRICING MODEL

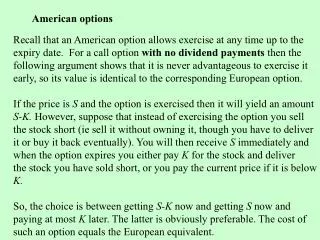

The American Options • Apart from the European options, the second group of options classified as vanilla options are American options. These options allow the holder of the option the ability to exercise the option at any point in time up to maturity. • American options are the most commonly traded options in the market. • However, the only case in which a closed-form solution to pricing an American option exists, is in the case where we are valuing an American call option with no dividends throughout its life. Exact pricing only exists for cases when a single known dividend exists via a pseudo-American formula.

American Calls with No Dividends • We can price American calls on a non-dividend paying stock because of an important attribute - it is never beneficial to exercise the option prior to expiry. We can briefly look at two primary reasons for this: • Firstly, holding the call option instead of exercising it and holding the stock is an insurance factor. An adverse stock movement (fall) would result in losses for the stock holder, but holding the call would enable the holder of the call to insure against any falls. • Secondly, there is the concept of time value of money. Paying the strike price earlier rather than later means that the holder of option loses out on the time value the money can achieve for the remainder of the option. • The attribute of non-exercise means that the American option can be priced via the standard Black-Scholes European call option formula and forcing dividends to 0.

American Options with a Single Dividend

American Calls with a Single Dividend (Roll, Geske & Whaley) • An American call option can be considered to be a series of call options which expire at the ex-dividend dates, and this case becomes a compound option or (an option on an option) with a closed-form solution as follows: S, t D1, t1 X, T

American Calls with a Single Dividend (Roll, Geske & Whaley) • With the variables are defined as: N2(a; b; ) is the is bivariate cumulative normal distribution function and S* is the critical stock price for which the following equation is satisfied: The critical stock price can be solved iteratively via the Bisectional method.

American Call Approximation (Barone-Adesi, Whaley) 1987 • Barone-Adesi and Whaley (1987) gave a quadratic approximation to price American Options based on a quadratic approximation method proposed by MacMillan (1986), and the pricing of the option is essentially a European option adjusted for an early exercise premium. and

American Call Approximation (Barone-Adesi, Whaley) 1987 • The European call option c is valued using the Black-Scholes-Merton European formula. Defining the variables as: where • The critical value of S* is defined as: and can be solved using the Newton-Raphson method and specifying appropriate seed values.

American Put Approximation (Barone-Adesi, Whaley) 1987 • . and • The European put option p is valued using the Black-Scholes-Merton European formula. Defining the variables as: where • The critical value of S* is defined as: and can be solved using the Newton-Raphson method and specifying appropriate seed values.

Binomial Trees (Cox, Ross & Rubinstein) 1979 • Binomial trees are widely used within finance to price American type options as it is easy to implement and handles American options relatively well. The binomial method constructs a tree lattice which represents the movements of the stock under geometric Brownian motion and prices the option relative to the stock price through means of backwards induction. • It effectively assigns a probability of an up movement and a down movement in the stock price based on the following: The terms for the up and down movement are: • Where d can be simplified to:

Binomial Trees (Cox, Ross & Rubinstein) 1979 • The probability of the stock price increasing at the next time period (node) is given as. And conversely, the probability of a down movement is given as 1-p. • We can now, via backwards induction, determine the price of an American call or put through the following: • Option values found at C0,0 and P0,0. • Even though implementation of the binomial model for American options and beyond is fairly simple, the major disadvantage of using the model is that it often requires a large number of nodes to achieve a decent accuracy.

Finite Differences Method (Brennan & Schwartz) 1977 • The finite difference method detailed under the European Options section can be applied to the case of American options as well. By incorporating an early exercise 'test' within an algorithm, we can determine the value of an American option as given by the PDE and its initial and boundary conditions using explicit, implicit and Crank-Nicholson schemes. • Similar to tree models, the finite differences method(s) are commonly used in practice because of two reasons; they are relatively easy to implement computationally and generally converge to a solution (albeit with more timesteps).

Monte Carlo Simulation and American Options (Longstaff and Schwartz) 2001 • Two approaches: 1. The least squares approach 2. The exercise boundary parameterization approach • Consider a 3-year put option where the initial asset price is 1.00, the strike price is 1.10, the risk-free rate is 6%, and there is no income

The Least Squares Approach • We work back from the end using a least squares approach to calculate the continuation value at each time • Consider year 2. The option is in the money for five paths for paths 1, 3, 4, 6, 7. These give observations on S of 1.08, 1.07, 0.97, 0.77, and 0.84. The continuation values are 0.00, 0.07e-0.06, 0.18e-0.06, 0.20e-0.06, and 0.09e-0.06

The Least Squares Approach (Cont’d) • Based on the previous continuation values and S, we fit a model of the form V=a+bS+cS2. We get a best fit relation V=-1.070+2.983S-1.813S2 for the continuation value V. • This defines the early exercise decision at t=2. We carry out a similar analysis at t=1 • In practice more complex functional forms can be used for the continuation value and many more paths are sampled

Exercise Paths at 2-Year Point • Continuing at the 2-year point for paths 1,3,4,6 and 7 with V =0.0369, 0.0461, 0.1176, 0.1520 and 0.1565. Corresponding exercise values: 0.02, 0.03, 0.13, 0.33 and 0.26. This means we should exercise at 2-year point for paths 4, 6 and 7.

1-Year Point • Consider year 1. The option is in the money for paths 1,4,6,7 and 8. These give observations on S of 1.09, 0.93, 0.76, 0.92, and 0.88. The continuation values Vi are 0.00, 0.13e-0.06, 0.33e-0.06, 0.26e-0.06, and 0.00. • Fitting a model of the form V=a+bS+cS2 we get a best fit relation V=2.038-3.335S+1.356S2 for the continuation value V

1-Year Point (Cont’d) • Continuing at the 1-year point for paths 1,4,6,7 and 8 with V =0.0139, 0.1092, 0.2866, 0.1175 and 0.1533. Corresponding exercise values: 0.01, 0.17, 0.34, 0.18 and 0.22. This means we should exercise at 1-year point for paths 4, 6, 7 and 8.

Value of Options • Determined by discounting each cash flow back to time zero at the risk-free rate and calculating the mean. • Therefore, Because the result is greater than 0.10, it is not optimal to exercise the option immediately.

The Early Exercise Boundary Parametrization Approach • We assume that the early exercise boundary can be parameterized in some way • We carry out a first Monte Carlo simulation and work back from the end calculating the optimal parameter values • We then discard the paths from the first Monte Carlo simulation and carry out a new Monte Carlo simulation using the early exercise boundary defined by the parameter values.

Application to Example – Monte Carlo for Exercise Boundary Parametrization • We parameterize the early exercise boundary by specifying a critical asset price, S*, below which the option is exercised. • At t=3 the optimal S* is 1.10. • At t=2 the values of the option for the eight paths are 0.00, 0.00, 0.07e-0.06x1, 0.18e-0.06x1, 0.00, 0.20e-0.06x1, 0.09e-0.06x1, and 0.00, respectively. The average is 0.0636 • Suppose S*(2) = 0.77. After exercise, 0.00, 0.00, 0.07e-0.06x1, 0.18e-0.06x1, 0.00, 0.33, 0.09e-0.06x1, and 0.00. The average is 0.0813 • Choosing S*(2) = 0.84, 0.97, 1.07, 1.08, the averages after exercise are: 0.1032, 0.0982, 0.0938 and 0.0963. • Therefore the optimal S*(2) = 0.84 or 0.84 S*(2) <0.97.

Application to Example (Cont’d) • When S*(2) = 0.84, the eight paths are: 0.00, 0.00, 0.0659, 0.1695, 0.00, 0.33, 0.26, and 0.00. The average is 0.1032. • Similar to the analysis at t=2, for S*(1) = 0.76, 0.88, 0.92, 0.93, and 1.09, the averages after exercise are 0.1008, 0.1283, 0.1202, 0.1215, and 0.1228 • At t=1 the optimal S* for the eight paths is 0.88 or 0.88 S*(1) <0.92. • In practice we would use many more paths to calculate the S*