IRS Tax Audit

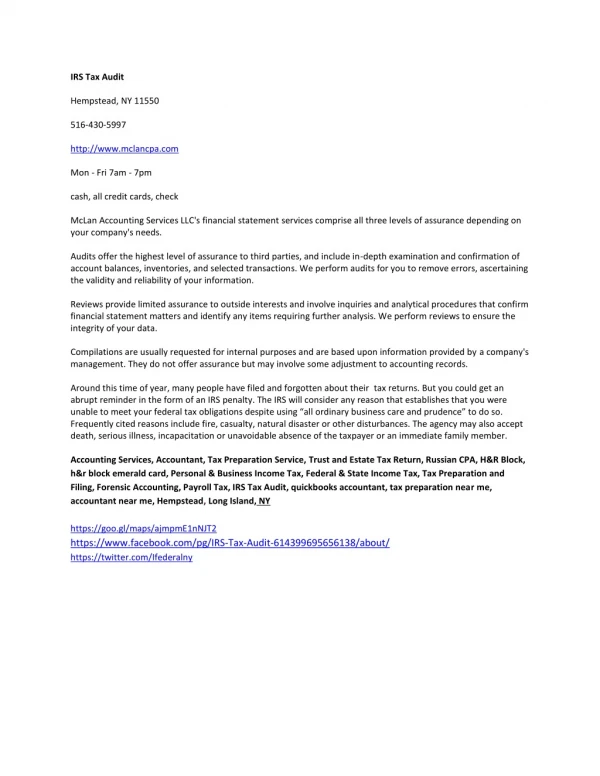

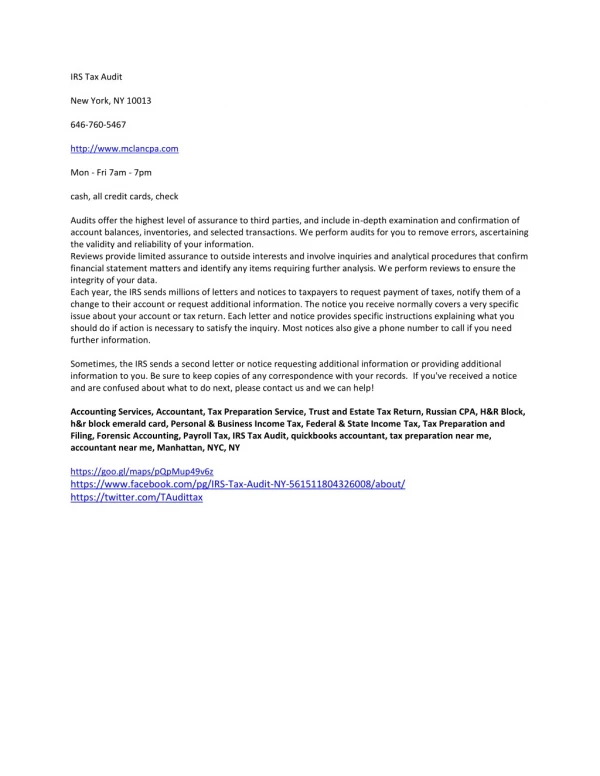

Address: 4121 18th Ave, suite 109 Brooklyn, NY 11218 Phone: (347) 560-5953 Website: www.mclancpa.com Category: Accounting Services Hours: Mon - Fri 7am - 7pm Payment: cash, all credit cards, check Description: Around this time of year, many people have filed and forgotten about their tax returns. But you could get an abrupt reminder in the form of an IRS penalty. The IRS will consider any reason that establishes that you were unable to meet your federal tax obligations despite using u201call ordinary business care and prudenceu201d to do so. Frequently cited reasons include fire, casualty, natural disaster or other disturbances. The agency may also accept death, serious illness, incapacitation or unavoidable absence of the taxpayer or an immediate family member. Each year, the IRS sends millions of letters and notices to taxpayers to request payment of taxes, notify them of a change to their account or request additional information. The notice you receive normally covers a very specific issue about your account or tax return. Each letter and notice provides specific instructions explaining what you should do if action is necessary to satisfy the inquiry. Most notices also give a phone number to call if you need further information. Sometimes, the IRS sends a second letter or notice requesting additional information or providing additional information to you. Be sure to keep copies of any correspondence with your records. If you've received a notice and are confused about what to do next, please contact us and we can help! Audits offer the highest level of assurance to third parties, and include in-depth examination and confirmation of account balances, inventories, and selected transactions. We perform audits for you to remove errors, ascertaining the validity and reliability of your information. Keywords: Trust and Estate Tax Return, Russian CPA, H&R Block, h&r block emerald card, Personal & Business Income Tax, Federal & State Income Tax, Tax Preparation and Filing, Forensic Accounting, Payroll Tax, IRS Tax Audit, quickbooks accountant, tax preparation near me, accountant near me, Brooklyn, NY. social links: https://www.facebook.com/IRS-Tax-Audit-1233468800133974 https://twitter.com/audit_irs https://www.linkedin.com/in/tax-audit-8510b5182/ https://www.google.com/maps/place/IRS Tax Audit/@40.6315853,-73.9769615,17z/data=!3m1!4b1!4m5!3m4!1s0x0:0xb7129186656dceb2!8m2!3d40.6315853!4d-73.9747728

27 views • 2 slides