Download

1 / 26

270 likes | 386 Vues

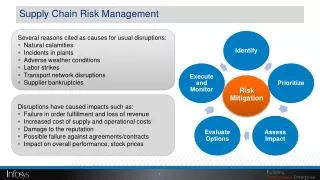

Risk Management in Guar Value Chain. - SiddHaRTH Surana. Agenda. Price risk management for value chain Practical issues in hedging Key Elements of a hedge program. Guar Value Chain. Farmer. Grow guar in hope of good prices but.. What if all the farmers think alike?

E N D

Risk Management in Guar Value Chain -SiddHaRTH Surana

Agenda Price risk management for value chain Practical issues in hedging Key Elements of a hedge program

Farmer Grow guar in hope of good prices but.. What if all the farmers think alike? How to protect against price fall?

Guar Marketing Options Sell in Cash (Spot) Market Enter a Forward sale contract Hedge in a futures Buy ‘Put’ options (Not really an option currently)

Sell in the Cash Market • Guess when the highest price will come • Sell when you need the cash • Sell a little bit throughout the year • Sell when price reaches a target • Sell by a certain date-whatever be the price • Aren’t all the above features of S..... ?

Forward Contracts • Fixed price contract for a set delivery location, date, quantity and quality • Contracts can be: • Pre-harvest (production unknown) • Post-harvest (production known) • Lock in a sure price (but give up a gain if the prices increases later) • Can contract for any quantity, quality, place and date-provided you find a buyer • Search cost, negotiation on specification • Can’t lift the hedge • Can’t sell your produce to anyone else • Counter-party risk?

Hedging with futures Sell futures contract on a commodity exchange When you sell the physical commodity, buy back the contract Alternatively deliver against futures position Loss/gain in the cash market is offset by the gain/loss in the futures Can lift the hedge any time Can sell the physicals anytime, to anyone Standardized specs (lack customization but no need for negotiation) Ready availability of buyers Need for Margin and MTM payments Counter-party risk is guaranteed*

Calculation • 1st Aug.: A farmer is expecting new crop to arrive in November • Prevalent price of Nov. contract: Rs 5,000 • Farmer wants to lock in the price for his 10MT expected production of guar • He sells 10MT Nov. expiry guar futures. • Scenarios on 20th Nov. • Spot price =4800=Nov. futures price • Gain on Futures position=Rs 200/Qtl • Realization from cash sale= Rs 4800 • Net price=4800+200=5000

Calculation • Scenario on 20th Nov. • Spot price =5200=Nov. futures price • Loss on Futures position=Rs 200/Qtl • Realization from cash sale= Rs 5200 • Net price=5200-200=5000 • Spot Price=5000=Nov. futures • Gain/Loss on Futures position=0 • Realization from cash sale= Rs 5,000 • Net price=5,000

Trader • Exposure to flat price movement • Inventory price risk • Can sell futures to the extent of guar stock • Keep rolling-over till the time of physical sale • Forward commitment • Go long on futures • Once physical is covered, lift the hedge

Processor/Exporter Exposed to both sides-RM prices and Finished goods Example: Split miller has committed a powder plant 50 MT of guar split to be supplied in January. Exposure to seed prices going up Hedge by buying seed futures Lift the hedge when physical is covered in spot market Alternatively, can stand for delivery in futures Have split/seed stocks- can go short in futures to hedge

Processor/Exporter Example: A Guar Powder manufacturer has committed an export shipment of 500MT by March 2014 Risk: Splits prices going up Hedge by splits (Guar Gum) futures Lift the hedge when physical is covered Alternatively, can stand for delivery in futures Risk to powder prices: No direct contract but can be hedged with gum futures (only if you have ready stocks).

End User/Importer • Risk: Guar gum prices going up • Domestic consumers can hedge by going long on guar gum futures • Foreign buyers? • No direct access • Fully owned resident subsidiaries can access Indian market

How much to hedge Rule Based Management decides to hedge up to a certain percentage of Price risk exposure. Example - 60% of monthly production Incremental hedge percentage based on achievement of various price targets/forecasts Statistical method Calculating hedge quantity using Historical Hedge Ratio method Hedge to the extent that cash prices is correlated with the futures’ price

How much to hedge Dynamic Hedge • Dynamic hedging is done on the basis of a price forecast • During periods when favorable price movement is expected, the hedge is held in abeyance • Hedge is entered into when adverse price movement is expected • Exposed to risk if price views turn out incorrect

Benefits of Hedging • Stability of earnings & secured minimum operating margin; • Monetise value of unused commodity • Reduced cost of borrowing from banks • Increased access to credit as confidence of repayment increases • Capacity building for improved risk management also strengthens marketing / financial knowledge

Practical Issues in Hedging No Hedge is perfect but all hedges cost money

Duration and Quantity mismatch Duration mismatch (Futures expiries are on standard dates) If timing of cash market exposure (buy/sell) is known in advance, use futures that most closely matches the same When timing of cash market exposure is not known, or if far month contracts are not sufficiently liquid, hedge in the near contract and keep rolling Quantity mismatch (Futures have standard lot size) Try to match futures and cash position as closely as possible

Basis The difference between the cash price and futures price of a commodity. Basis = Spot price – Futures price Basis is: Specific to time and place Less variable than overall price Relatively predictable, typically narrows, leading to conversion

Prices Cash Basis Futures Time Present Expiry Basis

Basis What causes basis? Local demand supply scenario Relative storage capacity Transportation availability and cost Time to expiration (cost of carry) Quality differential

Possible Solutions • Enter into Basis quoted contract with your supplier or buyer • If you have entered into a contract to supply, you can buy corresponding futures (and hope for the basis to remain favorable) • Basis forecasting methods • Current basis • Last year same time • Last 3 years' average • Current basis adjusted for cost of carry

Key Elements of a Hedge Program Identify, Analyze and Quantify Market Risk Develop a Hedge Policy Controls and Procedures Implementation of Hedge Program Monitoring, Analyzing and Reporting Risk Repeat

Happy to help Visit: www.commadwise.com Contact us: Phone: +91-22-2840 9155, 99209 09155Email: info@commadwise.com