Download

1 / 140

1.4k likes | 1.52k Vues

ACA Update Focused on the Employer Mandate Final Regulations. Shenandoah University Business Symposium March 25, 2014 John M. Peterson Kaufman & Canoles, P.C. jmpeterson@kaufcan.com (757) 624-3003. Disclosures.

E N D

ACA Update Focused on the Employer Mandate Final Regulations • Shenandoah University Business Symposium • March 25, 2014 • John M. Peterson • Kaufman & Canoles, P.C. • jmpeterson@kaufcan.com • (757) 624-3003

Disclosures The following disclosure is required pursuant to IRS Circular 230 and applicable state and local tax provisions, the regulations that govern the practice of tax advisors. Any advice concerning Federal, state and local tax issues contained in this written communication (and any attachments) has not been written nor is it intended by the author or Kaufman & Canoles, PC to be used, and cannot be used, for the purpose of (i) avoiding federal, state or local tax penalties that may be imposed by the Internal Revenue Service or applicable state or local tax provisions, or (ii) promoting, marketing, or recommending to another party any transaction or matter addressed herein. If a formal covered opinion intended to provide such protection is desired, please contact us to discuss the issues and costs involved in preparation of such a covered opinion. Kaufman & Canoles is providing general education and not specific legal advice at this presentation.

Topics PPACA Overview & Timeline Health Insurance Reforms Individual Mandate Health Insurance Marketplace & Subsidies Large Employer Mandate

The 4 Patient Protection &Affordable Care Act Principles • Health insurance reform (no medical rating) • Begets requirement that everyone have coverage or purchase insurance (individual mandate) • But health insurance is expensive so provide Federal financial assistance towards the cost (Marketplace subsidies) • But to control government subsidies have to require that large employers continue to subsidize their employees health insurance (employer mandate)

ACA Key Events- Past • March 23, 2010- PPACA enacted • June 28, 2012- Supreme Court validates • November 6, 2012- election, no change • December 28, 2012- employer mandate proposed Regs • January 1, 2013- .9% & 3.8% “pay for” taxes began • March 2013- “Exchange” became “Marketplace”

ACA Key Events- Past • July 1, 2013- original deadline to start tracking employee hours (large vs. small, look-back measurement period) • July 9, 2013- employer mandate delayed until 2015 • October 1, 2013- distribution of Marketplace notice, first Marketplace open enrollment period began (HealthCare.gov website rough opening)

ACA Key Events- Past • January 1, 2014 • Health insurance reforms began (or at 2014 insurance renewal) • Health insurance Marketplace coverage and subsidies began (if purchased by 12/23/13) • Individual mandate & penalties began (subject to exceptions, exemptions)

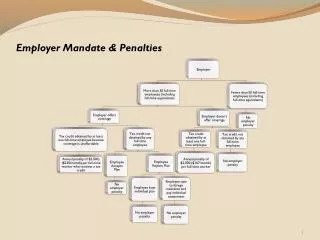

ACA Key Events- Recent/Soon • February 10, 2014- IRS issued final regulations on the employer mandate (4980H) • New 1 year delay for 50-99 employees • Other transitional relief & clarifications • March 6, 2014- IRS issued final regulations on the large employer information reporting requirements and processes associated with determining liability for the employer mandate • March 31, 2014- Initial Marketplace open enrollment period ends (applications made by this date avoid individual mandate penalty for 2014)

ACA Key Events- Future • July 1, 2014- new deadline to start tracking employee hours (large vs. small, look-back measurement period) • November 15, 2014 - February 15, 2015- Marketplace open enrollment period for 2015 coverage • Maybe in 2014? – IRS issues Regulations preventing discrimination in how employer provided group health insurance is offered/utilized

ACA Key Events- Future • January 1, 2015 (or first day of 2015 health plan year)- large (>99) employer mandate & penalties begin • January 1, 2016 (or first day of 2016 health plan year)- large (50-99) employer mandate & penalties begin • January 31, 2016- Large (>49) employers file 2015 forms (1094-C full time count and 1095-C offer of minimum essential coverage by employee/month) • ?? Regulations on auto-enrollment >200 employees • 2018- 40% “Cadillac” coverage excise tax begins

4 Health Insurance Markets • Individual (on and off exchange/Marketplace) • Small Group (<50 in 2014 and 2015, <100 in 2016, possibly larger in 2017 and future) • Large Group • Self-funded/self-insured (Grandfathered plans enjoy some exceptions)

Major Insurance Reforms • No health based ratings/underwriting (community rating) • Guaranteed issue & renewability • No annual dollar limits on essential health benefits • No lifetime dollar limits on essential health benefits

Major Reforms/Mandates • No-cost preventive care (no co-pays or deductibles) • Includes contraception for women • Cover dependent children through month turn 26 (includes step and foster children)

Major Reforms/Mandates • Maximum 90 day waiting period from date of eligibility • Eligibility based on lapse of time = 90 days from hire • Eligibility based on orientation period not > 1 month + 90 days • Eligibility based on average hours per period can measure for 1 year then offer within 1 month • Eligibility based on cumulative hours (1,200 max)

Major Reforms/Mandates • Deliver new Summary of Benefits and Coverage (SBC) • Expanded claims and appeals procedures • No rescission of coverage (except fraud or misrepresentation) • Non-discrimination requirements (when guidance issued)

Individual and Small Group Reforms • Premiums established by geographic rating area (not health of individual or group) • Premium age banding at maximum 3 to 1 disparity (age 64 vs. age 21) • No sex based ratings

Age Banding 0-20 0.635 21 1.000 25 1.004 30 1.135 35 1.222 40 1.278 45 1.444 46 1.500 48 1.635 50 1.786 53 2.040 55 2.230 60 2.714 65 3.000

Individual and Small Groups Must Cover 10 Essential Health Benefits • Ambulatory patient services • Emergency services • Hospitalization • Maternity and newborn care • Mental health & substance abuse • Prescription drugs • Rehabilitative & habilitative services • Laboratory services • Preventive & wellness services & chronic disease management • Pediatric care, including dental & vision

Comments on EHB • Notable medical services not EHB: • Cosmetic surgery • Adult dental and eye exams • Acupuncture • Routine foot care • Infertility • Weight loss programs & surgery • Long term care • Private nursing

Comments on EHB • Level of EHB benefits set by “benchmark” plan (example types of prescriptions) • Virginia benchmark plan requires coverage for: • Adult eye exams • Routine foot care • Infertility

No Individual Policy Delay in Virginia • Responding to angst over cancellation of non-ACA compliant individual policies a 1 year (now 3 year) grandfathering is allowed if authorized at state level and carriers agree • Virginia Board of Insurance has rejected and insurance carriers are not willing to extend non-compliant policies- no delay in Virginia

Health Reforms Enforcement- The Forgotten $100/day Penalty • Section 4980D excise/penalty tax • $100/day per affected employee ($36,500/year) • Applies to all size employers • Not delayed, already in effect in 2014 • Self report on IRS form 8928 • Self-correct within 30 days = no penalty • “Reasonable cause” cap at 10% of health costs

Health Reforms Enforcement- The Forgotten $100/day Penalty • Most reforms baked into health insurance contract, little employer concern • Employer concerns: • Failure to distribute SBC • Exceeding maximum 90 day wait • Deny free contraception (litigation)

Individual Mandate 2014 • Beginning with the month of January, 2014, everyone must have “minimum essential coverage” (MEC) or be penalized for each full month without coverage (unless exception/exemption applies) • Includes you, your spouse (if filing jointly) and your dependents (all individuals included on the tax return) • Coverage can be purchased from your or your spouse’s employer (if offered), on the individual market, from the Marketplace or provided by Medicare, Medicaid, Tricare, CHIP or other government programs

Individual Mandate • Penalty = greater of flat dollar amount per person or specified percentage of household income in excess of income tax filing threshold: • 2014 $95 or 1% of excess • 2015 $325 or 2% of excess • 2016 $695 or 2.5% of excess • Household income is Adjusted Gross Income (AGI) with the following add backs: • Foreign income excluded from AGI • Tax exempt or excluded interest • Any Social Security benefits not already included in AGI

Individual Mandate • Income tax filing thresholds (2013) • Single $10,000 • Married filing joint $20,000 • Dependent income included if dependent required to file an income tax return (parent can elect to include) • Dollar penalty for dependents under 18 is 50% of regular amount • Maximum dollar penalty for any household is 3 times the dollar amount

Individual Mandate • 2014 Example: • 5 person household (2 parents, adult child >17 and 2 children <18), none insured • Household income $50,000, assume filing threshold $20,000 • Dollar penalty before limitation = $380 (3 adults and 2 children @ 50% = 4 x $95) • Capped dollar penalty $285 ($95 x 3) • % penalty $300 ($50,000 - $20,000 x 1%) • Pro-rate $300 penalty for # of months without coverage

Individual Mandate • 2016 Example (same facts): • 5 person household (2 parents, adult child >17 and 2 children <18), none insured • Household income $50,000, assume filing threshold still $20,000 • Dollar penalty before limitation = $2,780 (3 adults and 2 children @ 50% = 4 x $695) • Capped dollar penalty $2,085 ($695 x 3) • % penalty $750 ($50,000 - $20,000 x 2.5%) • Pro-rate $2,085 penalty for # of months without coverage

Individual Mandate • Exceptions/exemptions from individual penalty: • Income below the tax filing threshold • Premiums for lowest cost plan available from employer or marketplace (Bronze) exceeds 8% of household adjusted gross income (net of marketplace subsidies) • Gap in coverage for less than 3 calendar months • Low income individuals in states not expanding Medicaid • Apply by 3/31/14 even if coverage not effective until 5/1/14 (4 month transition)

Individual Mandate • Hardship exemptions (apply through HHS/Marketplace) • Eviction & homelessness • Death of close family member • Casualty to residence • Bankruptcy • Recent unpaid medical expenses • Estimated 24 million excepted/exempt • IRS can charge interest on unpaid penalty tax but prevented from collecting via tax liens and levies • Essentially can only collect from refunds

Health Insurance Marketplace • What it is: a government operated online “storefront” in each state for residents to shop for and purchase individual health insurance • Had been called the “exchange” until spring 2013 • Marketplace offers private insurer Qualified Health Plans (QHP), no government insurance involved • 14 states operating their own, 36 states operated my federal government (Federally Facilitated Marketplace)

Health Insurance Marketplace • All individuals lawfully present in the US and not incarcerated can shop for and purchase health insurance through the new health insurance Marketplace • Healthcare.gov • Everyone can “comparison shop” • Only factors determining Marketplace rates are geographic location (“rating area”), age and smoker status • Virginia divided into 12 rating areas (see next slide) • 3 to 1 maximum age banding between ages 21 and 64 • No rate difference due to sex or medical condition • Smokers (4 or more per week) = up to 50% rate hike

Health Insurance Marketplace • All policies graded based on “actuarial value” • Measure of relative generosity • What % of standard medical costs will policy cover • 4 “metal” tier insurance options • Bronze 60% actuarial value (AV) • Silver 70% AV • Gold 80% AV • Platinum 90% AV

Catastrophic Plan • In addition to the 4 metallic tiers the Marketplace will offer a high deductible catastrophic plan to certain individuals • Younger than age 30; or • No other coverage “affordable”; or • Obtained “hardship” exemption • Meets individual mandate but not eligible for subsidies • Covers 3 primary care visits and no-cost preventive care

12 Virginia Rating Areas • Blacksburg • Charlottesville • Danville • Harrisonburg • Bristol • Lynchburg 7. Richmond 8. Roanoke 9. Virginia Beach-Norfolk 10. Arlington/Alexandria 11. Winchester 12. All other non-MSA

Lowest Monthly Virginia RatesBronze Coverage, Area 9 Age 21 Age 64+ $384.00 $498.60 $633.00 $637.44 $774.00 N/A Catastrophic $128.00 Bronze $166.20 Silver $211.00 2nd Lowest Silver $212.48 Gold $258.00 Platinum N/A Note exact 3 to 1 ratio

Marketplace Enrollment Periods • 2014 open enrollment 10/1/2013 – 3/31/2014 • 2015 open enrollment 11/15/2014 – 2/15/2015 • Special enrollment opportunities: • Marriage • Birth or adoption of a child • Permanent move to different rating area • Losing coverage other than by voluntary quit or failure to pay premium

SHOP Marketplace • For small employers to purchase group coverage • Small means < 50 (< 100 in 2016) • Must use SHOP to claim Small Business Health Care Tax Credit • Direct enrollment via broker in 2014 • Online enrollment promised for 2015

2 Marketplace Subsidies • APTC- Individuals and families with household income between 100% and 400% of Federal Poverty Level who purchase through the Marketplace will be potentially eligible for “advance premium tax credits” paid directly by the Marketplace to their selected insurer • CSR- Those between 100% and 250% of FPL will receive “cost-sharing reductions” (reduced deductibles and co-pays) if they purchase at least “Silver” coverage (70% actuarial value) • Collectively = Marketplace “subsidies”

Advance Premium Tax Credit (APTC) • Individuals and households 100% to 400% FPL • Available to 47% of US households • 20% are below 100% • 33% are above 400% • Marketplace (HHS) pays APTC directly to selected insurer “in advance” based on representations of households estimated 2014 income • Individual/household pays a % of INCOME, government pays the balance

Advance Premium Tax Credits • APTC operates by capping the individual/household share of the premium for 2nd lowest cost Silver plan at between 2% and 9.5% of household income • NOTE: APTC caps individual/household share of premium at a % of household income, not a % of the actual premium • Actual premium irrelevant to the individual/household • 100%-133% FPL pays 2% of household income for 2nd lowest cost Silver plan, government pays the balance • 300%-400% FPL pays 9.5% of household income for 2nd lowest cost Silver plan, government pays the balance

Sample 2014 Federal PovertyLevels/Lines (FPL) • One person household • 100% FPL $11,670 • 400% FPL $46,680 • Two person household • 100% FPL $15,730 • 400% FPL $62,920 • Three person household • 100% FPL $19,790 • 400% FPL $79,160 • Four person household • 100% FPL $23.850 • 400% FPL $95,400

APTC Table • Percentage of household income contribution towards 2nd lowest cost Silver (70%) coverage in Marketplace: • 100% to 133% FPL 2% • From 133% to 150% 3% to 4% • From 150% to 200% 4% to 6.3% • From 200% to 250% 6.3 % to 8.05% • From 250% to 300% 8.05% to 9.5% • From 300% to 400% 9.5% • Between bands use inverse linear sliding scale • 225% FPL is half way between 200%-250% band • Household income contribution half way between 6.3% and 8.05% = 7.04% • See K&C detailed APTC chart

K&C APTC Chart • Example: $30,000 family of 4 falls at 125% FPL, pays 2% of income ($50/month) towards 2nd lowest cost Silver • Below 100% FPL no subsidy (Medicaid non- expansion gap) • Above 400% FPL no subsidy