Download

1 / 7

70 likes | 167 Vues

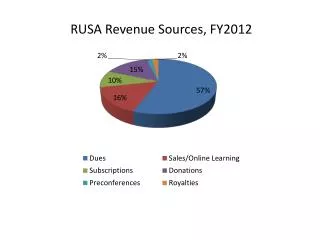

Accounting Updates for FY2012. THECB. Overview. AFR Manual Updates Supplemental Schedules MD&A: three years of comparative data Bad debt related to student receivables New Accounting Statements, #s 63-65 Questions/Issues. Supplemental Schedules.

E N D

Overview • AFR Manual Updates • Supplemental Schedules • MD&A: three years of comparative data • Bad debt related to student receivables • New Accounting Statements, #s 63-65 • Questions/Issues TACCBO 2012, Slide 2

Supplemental Schedules No longer required unless you present basic financial statements within a CAFR. Reference: GASB Stmt 44, summary. Districts can voluntarily include them. The guidance will remain the same. Good to include for GFOA, credit analysts, etc. TACCBO 2012, Slide 3

MD&A; Three Years of Data Three years’ worth of comparative data is required. The goal being to provide enough data in a comparative setting so that each of the two years presented can be compared to its prior year. Reference: Question 7.5.4, GASB implementation guide. TACCBO 2012, Slide 4

Bad Debt for Student Receivables Guidance in manual was incorrect. Guidance is in GASB S34, footnote 41 and FARM 703.92. For receivables that affect revenue, record the provision for bad debt against revenues. For receivables that do not affect revenue (i.e. student loans), record the provision as an expense under institutional support. TACCBO 2012, Slide 5

New GASB Statements Stmt 63 – Concerns the financial reporting of deferred elements in the statements including deferred outflows of resources, deferred inflows of resources and net position. Concerns mainly derivative positions and service concession arrangements (SCAs). Stmt 64 – an amendment of statement 53 which concerns the application of hedge accounting termination provisions for derivative instruments. TACCBO 2012, Slide 6

New GASB Statements(continued) No changes as a result of the new statements. However, with stmt 65 expanding the list of required elements considered deferred, we will include changes next year. And those changes will probably require prior year restatement. For example, debt issue costs (previously reported as assets) will now be expensed as an outflow of resources in the period in which they are incurred. TACCBO 2012, Slide 7