Download

1 / 21

250 likes | 588 Vues

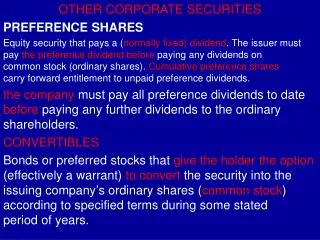

Redemption of Preference Shares. Redeemable Preference Shares: Equity OR Liability FRS 132 and Co Act 1965. Definitions. Financial assets : FRS 132 (11) a) cash b) an equity instrument of another entity c) a contractual rights (i) to receive cash

E N D

Redemption of Preference Shares Redeemable Preference Shares: Equity OR Liability FRS 132 and Co Act 1965

Definitions • Financial assets : FRS 132 (11) a) cash b) an equity instrument of another entity c) a contractual rights (i) to receive cash or another financial asset from another entity

Definitions • Financial liability : FRS 132 (11) a) contractual obligation: i) to deliver cash or another financial asset to another entity ii) to exchange financial instrument … under condition that are potentially unfavourable

Definitions • Equity instrument : FRS 132 (11) … any contract that evidences a residual interest in the assets of an entity after deducting all of its liability A - L = E

Definitions • Financial instrument : FRS 132 (11) …any contract that gives rise to financial assetof one entity and… (at the same time) gives rise to … a financial liability or equity instrument of another entity.

Presentation of instrument FRS 132 (15) : The issuer…shall classify the instrument …on initial recognition as a financial liability, financial asset or an equity instrument in accordance with the substance of the contractual arrangement and the definitions…

More … FRS 132 (35): Interest, dividend, losses and gains related to … financial liability should be reported in the income statement as expense or income. Distribution to holder of …equity instrument should be debited …directly to equity.

Preference shares Equity or liability: • obligations to deliver cash or financial assets? Or to exchange? • interest in residual assets? [profit = increase in equity]

“Redeemable” Redeem : exchange or buy back issuer has a contractual obligation to redeem : a) fixed / determinable future amount b) at a fixed / determinable future time [known at the point of contract]

Redeemable preference shares RM50m 10% RPS of RM1 each and redeemable in 5 years at a premium of RM0.50 each VS RM50m 10% coupon Bond

R P S • legal form of equity but are liabilities in substance i – mandatory redemption ii – fixed / determinable future amount iii – fixed /determinable future date iv – put option by holder

PS with option to redeem • equity • put option by holder : liability • option by issuer, voluntarily : liability if terms and condition is such that issuer may have no choice but to redeem it at some point in the future e.g. accelerating dividend

Conflicts Co Act : 9th Schedule …different classes of shares be disclosed separately as part of the share capital … …dividend is treated as an appropriation of profits, not expense… Sect 166A(6) and notwithstanding Sect 169(14) … true and fair view

Consequences : disclosure & treatment of dividend Equity : • disclose under Equity • dividend : directly charged to Equity (deduction to earnings/profits) Liability : • dividend : charged to Income Statement (expense) • disclose under Long-Term Liability (unless redemption is known to be less than one year)

Consequences : issue of the shares Equity : Dt Cash Cr Preference Share (R) Cr Share Premium Liability : Dt Cash Cr RPS [par + premium/discount]

Bond Price / Value at issue date: PVn = nΣt=1 Int + M . (i + r)n (i + r)n

RPS Price / Value at issue date: PVn = nΣt=1 Div + Red . (i + r)n (i + r)n

Consequences : dividend payments Equity: Dt Retained Profits Cr. Dividend Payable Dt Dividend Payable Cr. Cash/Bank

Consequences : dividend payments Liability: Dt. Dividend Exp Cr. Cash/Bank Cr. RPS OR Dt. Dividend Exp Dt. RPS Cr. Cash/Bank

Consequences : on redemption Equity: Dt. PS(R) Dt. Premium on Redemption Cr. Cash / Bank Liability: Dt. RPS Cr. Cash / Bank

Consequences : premium on redemption Equity: Dt. Share Premium Cr. Premium on Red. Liability: Dt..Share Premium Cr. Retained Profits