Download

1 / 37

370 likes | 498 Vues

Sovereign, Bank, and Insurance Credit Spreads: Connectedness and System Networks. M. Billio, M. Getmansky , D. Gray A.W. Lo, R.C. Merton, L. Pelizzon University of Massachusetts, Amherst March, 2014

E N D

Sovereign, Bank, and Insurance Credit Spreads: Connectedness and System Networks M. Billio, M. Getmansky, D. Gray A.W. Lo, R.C. Merton, L. Pelizzon University of Massachusetts, Amherst March, 2014 The research leading to these results has received funding from the European Union, Inquire Europe, and Seventh Framework Programme FP7/2007-2013 under grant agreement SYRTO-SSH-2012-320270.

Objectives • The risks of the banking and insurance systems have become increasingly interconnected with sovereign risk • Highlight interconnections: • Among countries and financial institutions • Consider both explicit and implicit connections

Methodology • We propose to measure and analyze interactions between banks, insurers, and sovereigns using: • Contingent claims analysis (CCA) • Network approach

Background • Existing methods of measuring financial stability have been heavily criticized by Cihak (2007) and Segoviano and Goodhart (2009): • A good measure of systemic stability has to incorporate two fundamental components: • The probability of individual financial institution or country defaults • The probability and speed of possible shocks spreading throughout the financial industry and countries

Background • Most policy efforts have not focused in a comprehensive way on: • Assessing network externalities • Interconnectedness between financial institutions, financial markets, and sovereign countries • Effect of network and interconnectedness on systemic risk

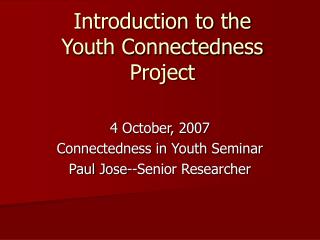

Background: Feedback Loops of Risk from Explicit and Implicit Guarantees 6 Source: IMF GFSR 2010, October Dale Gray

Background • The size, interconnectedness, and complexity of individual financial institutions and their inter-relationships with sovereign risk create vulnerabilitiesto systemic risk • We use Expected Loss Ratios (based on CCA) and network measures to analyze financial system interactions and systemic risk

Core Concept of CCA: Merton Model Expected Loss Ratio (ELR) = Cost of Guar/RF Debt = PUT/B exp[-rT] Fair Value CDS Spread = -log (1 – ELR)/ T

Moody’s KMV CreditEdge for Banks and Insurers • MKMV uses equity and equity volatility and default barrier (from accounting information) to get “distance-to- distress” which it maps to a default probability (EDF) using a pool of 30 years of default information • It then converts the EDF to a risk neutral default probability (RNDP) using the market price of risk, then using the sector loss given default (LGD) it calculates the Expected Loss Ratio (ELR) for banks and Insurers: • EL Ratio = RNDP*LGD=PUT/B exp[-rT]

Why EL Values? • EL Values are used because they do not have the distortions which affect observed CDS spreads • For banks and some other financial institutions: • The fair-value CDS spreads (implied credit spreads derived from CCA models, i.e. derived from equity information) are frequently > than the observed market CDS • This is due to implicit and explicit government guarantees

Why EL Values? • In other cases, e.g. in the Euro area periphery countries, CDS of banks and insurers appear to be affected by spillover from large sovereign spreads (observed CDS > FVCDS). • For these reasons we use the EL associated with the FVCDS spreads for banks and insurers which do not contain the distortions of sovereign guarantees or sovereign credit risk spillovers.

Sovereign Expected Loss Ratio • For this study the formula for estimating sovereign EL is simply derived from sovereign CDS EL Ratio Sovereign = 1-exp(-(Sovereign CDS/10000)*T) • EL ratios for both banks and sovereigns have a horizon of 5 years (5-year CDS most liquid)

Linear Granger Causality Tests ELRk(t) = ak + bkELRk(t-1) + bjkELRj(t-1) + Ɛt ELRj(t) = aj+ bjELRj(t-1) + bkjELRk(t-1) + ζt If bjk is significantly > 0, then j influences k If bkj is significantly > 0, then k influences j If both are significantly > 0, then there is feedback, mutual influence, between j and k.

Data • Sample: Jan 01-Mar12 • Monthly frequency • Entities: • 17 Sovereigns (10 EMU, 4 EU, CH, US, JA) • 59 Banks (31EMU, 11EU, 2CH, 12US, 4JA) • 42 Insurers (12EMU, 6EU, 16US, 2CH, 5CA) • CCA - Moody’s KMV CreditEdge: • Expected Loss Ratios (ELR)

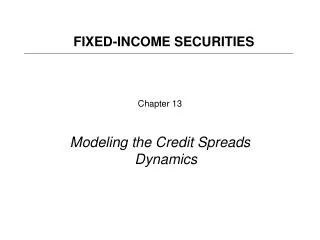

Mar 12 Blue Insurance Black Sovereign Red Bank Blue Insurance Black Sovereign Red Bank

Mar 12 Blue Insurance Black Sovereign Red Bank Blue Insurance Black Sovereign Red Bank

Network Measures • Indegree (IN): number of incoming connections • Outdegree (FROM): number of outgoing • connections • Totdegree: Indegree + Outdegree • Number of node connected: Number of nodes reachable following the directed path • Average Shortest Path: The average number of steps required to reach the connected nodes • Eigenvector Centrality (EC): The more the node is connected to central nodes (nodes with high EC) the more is central (higher EC) • Degrees • Connectivity • Centrality

Network Measures: FROM and TO Sovereign 17 X 102= 1734 potential connections FROM (idem for TO)

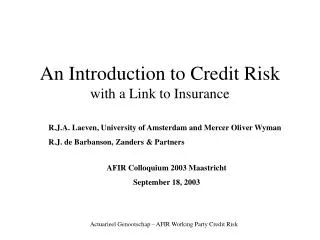

June 07 Blue Insurance Black Sovereign Red Bank

March 08 Blue Insurance Black Sovereign Red Bank

August 08 Blue Insurance Black Sovereign Red Bank Greece

December 11 Spain Blue Insurance Black Sovereign Red Bank

March 12 US Blue Insurance Black Sovereign Red Bank IT

March 12 Blue Insurance Black Sovereign Red Bank

Early Warning Signals t=March 2008; t+1=March 2009; t= Jul 2011; t+1= Feb 2012 Cumulated Exp. Loss Ratio ≡ Expected Loss Ratio of institution i + Expected Loss Ratios of institutions caused by i

CDS: Dec 11 Spain Blue Insurance Black Sovereign Red Bank

Dec 11 : EL-KMV Spain Blue Insurance Black Sovereign Red Bank

CDS:Mar 12 Blue Insurance Black Sovereign Red Bank IT

US Mar 12:EL-KMV Blue Insurance Black Sovereign Red Bank IT

Conclusion The system of banks, insurance companies, and countries in our sample is highly dynamically connected We show how one sovereign/financial institution is spreading risk to another sovereign/financial institution Network measures allow for early warnings and assessment of the system complexity

Implications The decision to bail out a bank or sovereign affects not only the sovereign and its own banks but also other sovereigns and foreign banks in a significant way Stress tests are not adequate. Need to account for interconnectedness and non-linearity in exposures