Download

1 / 27

280 likes | 670 Vues

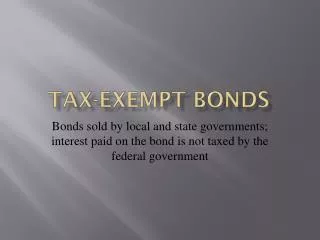

Tax-Exempt Bonds and Low-Income Housing Tax Credits. Dan Smith, CPA. CALIFORNIA. REPUBLIC. Bondholders. Bondholders. Bondholders. BIG BOX. Tax-exempt bonds (Lower interest payments). Public/Government Sector. Private Activity “Volume Cap” Tax-exempt bonds

E N D

Tax-Exempt Bonds and Low-Income Housing Tax Credits Dan Smith, CPA

CALIFORNIA REPUBLIC Bondholders Bondholders Bondholders BIG BOX Tax-exempt bonds (Lower interest payments) Public/Government Sector PrivateActivity “Volume Cap” Tax-exempt bonds (Lower interest payments) Multi-Family Housing Taxable bonds (Higher interest payments) Private Sector

Two examples: Volume Cap for 2008 Additional Bonds* California Volume Cap (2008) California Florida Nevada New York Ohio Texas $3,107,023,275 1,551,355,655 262,095,000 1,640,306,965 974,687,945 2,031,872,300 $1,144,564,324 571,487,942 96,550,479 604,255,799 359,055,260 748,500,523 CALIFORNIA REPUBLIC Indiana Volume Cap (2008) *IRS Notice 2008-79 Student Loans Single-Family Housing Docks and Wharves Multi-Family Housing Industrial Development Airports State “Volume Cap” Tax-exempt Bonds Greater of $90/person or $273,270,000 for 2009

Tax Credit Application Bond Application “Volume Cap” Tax-exempt Bonds 9% Credits! 4% Credits!

CALIFORNIA REPUBLIC Inducement Resolution ! Borrower (City/County) Bond Issuer Public hearing or “TEFRA” requirement

Credit Enhancer Underwriter Bond Purchase Agreement Bonds CALIFORNIA REPUBLIC Trust Indenture Purchasers $ $ RegulatoryAgreement Loan Agreement Mortgage Note Lender DRAW Req Invoices Borrower “AAA” “Aaa” (City/County) ? Bond Issuer $ Bond Proceeds Interest Payments $ Trustee Bond Proceeds $ Interest Payments $ Project

50% Test Land plus Depreciable Basis $8.2 mil E.B. = $7.6 mil Eligible Basis Tax Credit % Annual Tax Credits $7.6 mil 4% 304k “Aggregate Basis”

50% Test $ Bonds Land plus Depreciable Basis Tax-exempt bonds + Interest Earned ≥50% “Aggregate Basis” $8.2 mil E.B. = $7.6 mil 50% Tax-exempt bonds plus Interest Earned “Aggregate Basis”

50% Test Eligible Basis Tax Credit % Annual Tax Credits $7.6 mil 4% $304k $ Land plus Depreciable Basis Tax-exempt bonds + Interest Earned $5 mil ≥50% =61% = “Aggregate Basis” $8.2 mil $8.2 mil E.B. = $7.6 mil $5 mil 50% Bonds Tax-exempt bonds plus Interest Earned “Aggregate Basis”

50% Test $ Land plus Depreciable Basis $5 mil =50% =61% = $10 mil $8.2 mil 49.999995% $10 mil $10,000,001 E.B. = $9.4 mil $8.2 mil E.B. = $7.6 mil $4.7 mil Eligible Basis Tax Credit % Annual Tax Credits $7.6 mil 4% $304k $9.4 mil $376k $5 mil 50% 50% $188k! Bonds Tax-exempt bonds plus Interest Earned “Aggregate Basis”

States are asking developers to find other sources of financing in order to stretch the bond cap! 50% Tax-exempt bonds plus Interest Earned “Aggregate Basis”

Additional Requirements of Private Activity Bonds 15% rehab requirement on acquisition Additional Requirements of Private Activity Bonds Portion of acquisition financed with bonds = $10 mil 15% Rehab ≥ $1.5 million

($5 mil x 2%) Additional Requirements of Private Activity Bonds 2% “Cost of Issuance Limitation” BIC paid from bond proceeds ≤ $100k $5 mil Tax-exempt bonds plus Interest Earned

Good Costs Land and depreciable costs for income tax purposes …paid or incurred after the date of the Inducement Resolution Additional Requirements of Private Activity Bonds “Good Costs/Bad Costs” 95% of proceeds must be used for “good costs” $5 mil $4.75 mil Tax-exempt bonds plus Interest Earned “Aggregate Basis” This 95% in 95-5 test is slightly different than the “good cost/bad cost” 95%, correct?

Bad Costs Costs incurred prior to Inducement Resolution Intangible assets Bond issuance costs and underwriting Loan origination fees amortized over the perm loan period Additional Requirements of Private Activity Bonds “Good Costs/Bad Costs” 95% of proceeds must be used for “good costs” $5 mil $4.75 mil Tax-exempt bonds plus Interest Earned “Aggregate Basis” This 95% in 95-5 test is slightly different than the “good cost/bad cost” 95%, correct?

Inducement Resolution Bonds Additional Requirements of Private Activity Bonds Inducement Resolution 95% “Good Costs” 60 days 5% “Bad Costs” • Three dates and items: • Bond Issuance • “Intent” • Inducement Resolution • Reimbursement Resolution • What’s the whole 60 days thing? • (see p. 43 of Orrick booklet) • I think I’d be fine if we were just talking about Reimbursement Resolution • P. 10 of Orrick says 20% of bonds could be used to reimb certain “soft costs”…see 18 months rule on p. 11

Construction Method Financing Method

Construction Method Financing Method

Eligible Basis x DDA/QCT EB adj. for DDA/QCT x Applicable Fraction Qualified Basis x Applicable Percentage Annual LIHTC Project X Project Y 10,000,000 100% 10,000,000 100% 10,000,000 3.50% 350,000 10,000,000 100% 10,000,000 100% 10,000,000 8.00% 800,000

Financing LIHTC Projects $ $ $ CREDITS 9%Credits Investors $ Higher Interest Debt Fund / Upper tier Limited Partnership Equity Needed Sources Lower Tier Operating Limited Partnership

Financing LIHTC Projects $ $ $ 9%Credits Investors Fund / Upper tier Limited Partnership Needed Sources Lower Tier Operating Limited Partnership

Financing LIHTC Projects $ $ $ CREDITS 4%Credits Investors $ Lower Interest Fund / Upper tier Limited Partnership Debt Equity Needed Sources Lower Tier Operating Limited Partnership

Dan Smith 303 W. Third Street Dover, OH 44622 dan.smith@novoco.com Tel: 330.602.4600 www.novoco.com Fax: 330.602.4601