Download

1 / 17

180 likes | 419 Vues

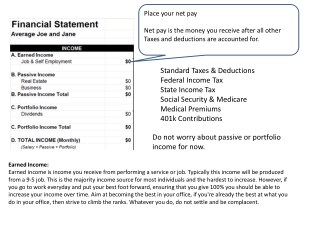

What is a 401k Plan?. A 401k is a company/employer sponsored retirement plan that allows workers to take out a portion of money from their paychecks, store it on a retirement plan account and earn interest tax-deferred. Tax-deferred means money is taxed on withdrawal.

E N D

What is a 401k Plan? • A 401k is a company/employer sponsored retirement plan that allows workers to take out a portion of money from their paychecks, store it on a retirement plan account and earn interest tax-deferred. • Tax-deferred means money is taxed on withdrawal. • A 401k retirement plan must be sponsored by an employer or an organization. • The actual work of administration and monitoring of accounts is usually outsourced to independent banks, mutual fund companies, financial service enterprises and more. • As soon as an employee gets a paycheck he/she can transfer a portion of it (there are annual limits) to the 401k account. In fact, most of the time direct deposit is used to transfer funds. • Types of investments available include mutual funds, stocks, bonds, money market instruments (both short and long term).

What is the difference between a 40lk and a 403b? • 403(b) plans are very similar but there are differences… • 403(b) plans don't necessarily require substantial administration and involvement by the employer. Usually available to public employees or nonprofits. • While 401(k) plans must follow sophisticated regulations under the laws governing retirement plans, known as ERISA, 403(b) plans are not necessarily subject to ERISA. • In many instances, employers don't make any contributions to 403(b) plans on behalf of their employees; employees may therefore miss out on employer matches, but the lack of employer contributions makes administration much simpler. • Also, 403(b) plans that include employer contributions often have more favorable vesting provisions than private employers offer in 401(k) plans. Typically it could take an employee up to three years or longer to be fully vested. • 403(b) plans often have immediate vesting. All employee contributions are immediately vested.

What is the big deal with tax deferred? Let me break it down: An individual is in the 25% tax bracket. That means 25% of all their earnings go to taxes. Tax-deferred contributions allow an employee to avoid paying taxes on the contributions made to a 40lk or 403b and reduce their taxable income. What is the tax savings for Employee B?

What is the big deal with tax deferred? • Employee B made a $6,000 contribution to their 40lk • However, their net income was only reduced by $4,500 • They got a $1,500 tax break. • That means their paycheck was only reduced by $187.50, but they were able to make a $250.00 contribution to their 40lk every paycheck. ( It is like stealing money… but LEGAL!!) • In addition that $1,500 gets put to work in the market for the next 40 years compounding many times and earning far more interest.

What are my investment choices? • What is the number one rule of investing? • Diversification!!! • What does it mean to be diversified? • Money is spread out over many different assets. • Why is diversification so important? • This way if one investment does not work out, you do not lose everything.

Traditional IRA Simplified Definition: A Traditional IRA is a tax deferred retirement vehicle. Like a 40lk. Income limits: Everyone is eligible to contribute to a Traditional IRA, but not everyone will get the benefit of a tax deduction. Withdrawals: Traditional IRA holders are eligible to withdraw from their IRA at age 59 ½, at which point their withdrawals are taxed as ordinary income. There are stiff penalties for early withdrawal (with certain exceptions). Required Minimum Distributions: Owners of Traditional IRAs are subjected to Required Minimum Distributions, which begin at age 70 ½. This means Traditional IRA holders are required to make a minimum withdrawal every year regardless of whether or not they need the money. Advantages of a Traditional IRA: Similar to a 40lk or 403b qualified deposits are made tax deferred, which could lead to a significant tax break. Disadvantages of a Traditional IRA: The minimum required distribution is a disadvantage because it requires IRA holders to withdraw a certain portion of their funds – whether they want to or not. It is also difficult to determine what your tax rate will be in retirement.

Roth IRA Simplified Definition: A Roth IRA is a tax exempt retirement vehicle. Contributions to Roth IRAs are not tax deductible when they are made; however, qualified distributions made during retirement years are tax free. Income limits: A person filing their taxes as single cannot earn over $122,000. Married couples are limited to an annual maximum income level of $179,000. Withdrawals:The minimum withdrawal age is 59 ½. When the money is withdrawn, none of it is taxed. The principal can also be withdrawn at any time without penalty, however, the earnings must remain in the IRA or they will be subject to taxes and penalties if withdrawn early. Required Minimum Distributions: There is no minimum distribution for Roth IRA accounts. Advantages of a Roth IRA: The biggest advantage of a Roth IRA is tax free withdrawals on the principal and all earnings. The other advantage is the absence of minimum withdrawal requirements. Disadvantages of a Roth IRA:Not everyone qualifies for a Roth IRA because of the income limits.

How should I invest in my retirement plan ? Think about risk… How much risk should you take when you are younger and further away from retirement? The further away from retirement the more risk you should take. How should you adjust your risk tolerance as you approach your retirement? You should take less risk as you approach retirement. Why should investors move to safer investments as they get closer to retirment? If you are in very high risk investments too close to retirement and the market takes a turn for the worse your entire retirement could be in jeopardy. Unfortunately, many Americans have recently found this out the hard way.

How much am I allowed to invest for retirement? 2011 Limitations and Restrictions 2011 IRA Contribution Limits – Age 49 & Below - $5,000 Age 50 & Above - $6,000 ROTH IRA Phase-Out Range & Limits Single - $107,000 - $122,000 Married Filing Jointly - $168,000 - $179,000 40lk Contribution Limits (403b) Age 49 & Below - $16,500 Age 50 & Above - $22,000 Defined Contribution Plans, basic limits Max Dollar Allocation - $49,000 Max Considered Compensation - $245,000

BIG IDEA!!!Save small and early rather than big and late.Remember… You can never say that you never new that you needed to save for your retirement or nobody every told me how to save for my retirement, cause….