Download

1 / 1

0 likes | 9 Vues

Corporate NPS is an excellent retirement savings scheme that benefits both employers and employees. For employees, it gain access to a flexible, portable, and tax-saving retirement plan. <br><br>To know more, <br>Visit - https://www.utipension.com/blog/corporate-nps-why-should-you-consider

E N D

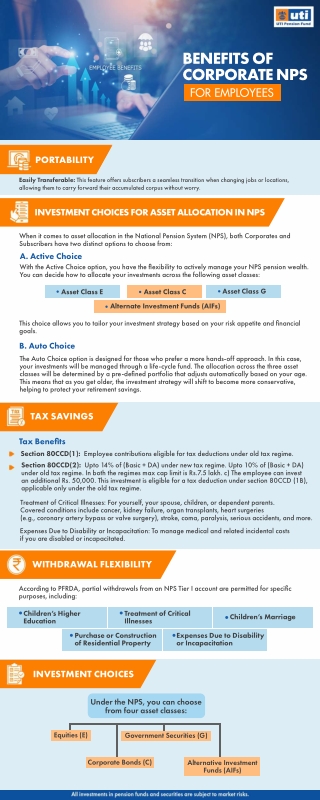

BENEFITS OF CORPORATE NPS FOR EMPLOYEES PORTABILITY Easily Transferable: This feature offers subscribers a seamless transition when changing jobs or locations, allowing them to carry forward their accumulated corpus without worry. INVESTMENT CHOICES FOR ASSET ALLOCATION IN NPS When it comes to asset allocation in the National Pension System (NPS), both Corporates and Subscribers have two distinct options to choose from: A. Active Choice With the Active Choice option, you have the flexibility to actively manage your NPS pension wealth. You can decide how to allocate your investments across the following asset classes: Asset Class G Asset Class E Asset Class C Alternate Investment Funds (AIFs) This choice allows you to tailor your investment strategy based on your risk appetite and financial goals. B. Auto Choice The Auto Choice option is designed for those who prefer a more hands-off approach. In this case, your investments will be managed through a life-cycle fund. The allocation across the three asset classes will be determined by a pre-defined portfolio that adjusts automatically based on your age. This means that as you get older, the investment strategy will shift to become more conservative, helping to protect your retirement savings. TAX SAVINGS Tax Benefits Section 80CCD(1): Employee contributions eligible for tax deductions under old tax regime. Section 80CCD(2): Upto 14% of (Basic + DA) under new tax regime. Upto 10% of (Basic + DA) under old tax regime. In both the regimes max cap limit is Rs.7.5 lakh. c) The employee can invest an additional Rs. 50,000. This investment is eligible for a tax deduction under section 80CCD (1B), applicable only under the old tax regime. Treatment of Critical Illnesses: For yourself, your spouse, children, or dependent parents. Covered conditions include cancer, kidney failure, organ transplants, heart surgeries (e.g., coronary artery bypass or valve surgery), stroke, coma, paralysis, serious accidents, and more. Expenses Due to Disability or Incapacitation: To manage medical and related incidental costs if you are disabled or incapacitated. WITHDRAWAL FLEXIBILITY According to PFRDA, partial withdrawals from an NPS Tier I account are permitted for specific purposes, including: Treatment of Critical Illnesses Children’s Higher Education Children’s Marriage Purchase or Construction of Residential Property Expenses Due to Disability or Incapacitation INVESTMENT CHOICES Under the NPS, you can choose from four asset classes: Equities (E) Government Securities (G) Corporate Bonds (C) Alternative Investment Funds (AIFs)