Download

1 / 1

0 likes | 3 Vues

Tax savings are a significant motivator for NPS subscribers. The structure of the NPS allows individuals to enjoy deductions that can significantly reduce their taxable income. <br><br>To Know more, <br>Visit - https://www.utipension.com/open-nps-account

E N D

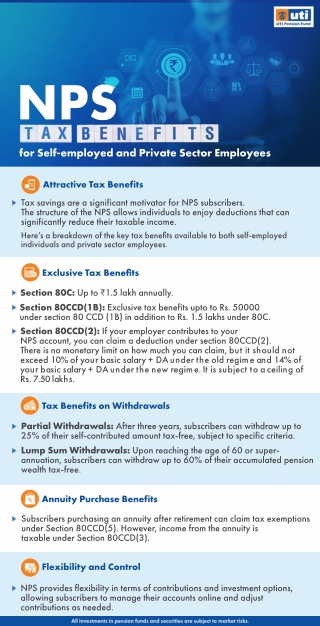

NPS for Self-employed and Private Sector Employees Attractive Tax Benefits Tax savings are a significant motivator for NPS subscribers. The structure of the NPS allows individuals to enjoy deductions that can significantly reduce their taxable income. Here’s a breakdown of the key tax benefits available to both self-employed individuals and private sector employees. Exclusive Tax Benefits Section 80C: Up to ₹1.5 lakh annually. Section 80CCD(1B): Exclusive tax benefits upto to Rs. 50000 under section 80 CCD (1B) in addition to Rs. 1.5 lakhs under 80C. Section 80CCD(2): If your employer contributes to your NPS account, you can claim a deduction under section 80CCD(2). There is no monetary limit on how much you can claim, but it should not exceed 10% of your basic salary + DA under the old regime and 14% of your basic salary + DA under the new regime. It is subject to a ceiling of Rs. 7.50 lakhs. Tax Benefits on Withdrawals Partial Withdrawals: After three years, subscribers can withdraw up to 25% of their self-contributed amount tax-free, subject to specific criteria. Lump Sum Withdrawals: Upon reaching the age of 60 or super- annuation, subscribers can withdraw up to 60% of their accumulated pension wealth tax-free. Annuity Purchase Benefits Subscribers purchasing an annuity after retirement can claim tax exemptions under Section 80CCD(5). However, income from the annuity is taxable under Section 80CCD(3). Flexibility and Control NPS provides flexibility in terms of contributions and investment options, allowing subscribers to manage their accounts online and adjust contributions as needed.