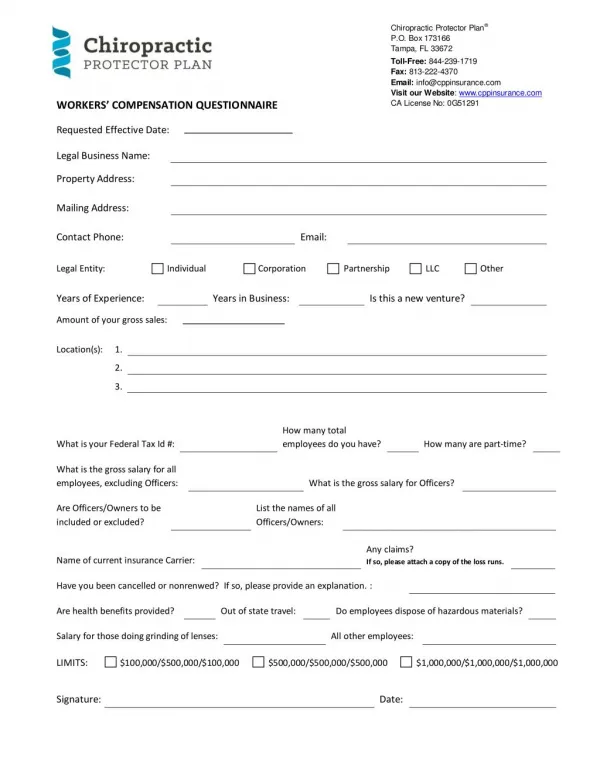

Download

1 / 6

0 likes | 14 Vues

we provide best Workers Compensation Insurance For Roofers

E N D

CALL FOR CONSULTATION fadi@coastalworkcomp. com 1-800-411-0733 Call for consultation Workers Compensation Insurance For Roofers Call Now Looking for a?ordable workers comp for roofers? Here’s a way you can lower your premiums by up to 30-40 percent. You never know when you may need workers comp for roofers. Employees put their lives on the line each time they climb up on a roof, and your company could be one accident away from bankruptcy. A single misstep could cause one of your workers to fall and severely injure themselves. In the worst-case scenarios, these falls prove fatal. It’s no wonder why roo?ng is one of the top ?ve deadliest jobs. Every roo?ng company should carry workers’ comp insurance to protect their employees. But, companies often ?nd it di?cult to obtain coverage outside of the State Fund because roo?ng is a high-risk industry. However, if you have between 5-500 employees, you may qualify for a pay-as-you-go plan with Coastal Work Comp . Here’s what you need to know before you send anyone on a roof without proper coverage again. Contact us protected by reCAPTCHA The Value of Workers’ Compensation in the Roo?ng Industry ✉ - → Privacy - Terms Contact Us As previously stated, roo?ng is a dangerous job. Workers climb multiple stories using ladders, scaffolding, and other rickety lifts. They often walk across unstable shingles that could give way in the blink of an eye. And if Mother Nature has her way, a gust of wind or sudden rainstorm can make things even more treacherous. It’s no wonder why on-the-job injuries are so common in the industry. Even the most skilled roofers can lose

their footing in the blink of an eye. Carrying roo?ng insurance for your employees is a must. This coverage will ensure you can pay for any medical bills your workers may have after sustaining a work- related injury. It will also pay for rehabilitation costs and lost wages while your employee heals. Too many companies, however, don’t see the value of purchasing coverage. They view it as an added expense they don’t need. This belief, while cost-e?cient at the time, could end up costing you more than you bargained. Besides, most states require roo?ng companies to carry workers’ comp coverage. And if you reside in one that doesn’t, there is a good chance you’ll need to prove you have a policy before anyone hires your roofers. Added Protection with a Workers’ Comp Policy Workers’ compensation insurance protects both your roofers and your company. In the event of an accident, both you and your employee will know you have the coverage needed to pay for care. Neither side will lose sleep worrying about accumulating debt from medical bills. As long as you keep your policy active, the Workers Compensation insurance for Roofers company will jump in and cover these unexpected expenses. What you may not realize, however, is the protection that workers’ comp also provides your business. Once a claim settles, your employee will no longer be able to bring any more litigation against you for the injury. In a high-risk job like roo?ng, this protection may mean the difference between quickly settling a case or ?ling for bankruptcy. How Are Workers Comp Settlements Calculated? Any worker injured while performing their job may be able to collect workers’ compensation. The total amount of money an employee receives depends on several factors. These include the extent of the injury, amount of time away from work, rehabilitation needed, and disability. Each state has different rules when it comes to calculating settlements. On average, employees should expect to receive two-thirds of their income while they are unable to work. Others may receive a lump sum payment. The goal of a settlement is to agree on an amount that satis?es both parties. While insurance providers try to reach an agreement with the injured employee as quickly as possible, many of these cases do go to court. In these instances, your workers’ compensation insurance will also cover any legal costs or court fees. In order to qualify for a settlement, the worker must have: Been an employee of your company. Sustained the injury at work or while performing job-related duties. If you cannot prove these two key items, the insurance company will deny the claim. In the roo?ng industry, most workers’ comp injuries are the result of a fall, faulty equipment, or hazardous materials. Broken bones, head injuries, heatstroke, puncture wounds, paralysis, and death are some of the most common injuries.

Construction Workers Compensation Solar Installer Workers Compensation Insurance Workers Compensation Insurance For Roofers Manufacturing Worker Compensation Insurance Framers Workers Compensation Insurance Tree Service Workers Compensation Workers Trucking Workers Compensation Insurance Home Health Care Workers Compensation Insurance Compensation For Sta?ng Agencies

Workers Comp For Non-Emergency Medical Transportation Cannabis Workers Compensation Insurance Janitorial Workers Compensation Insurance Hospitality Workers Compensation Insurance Workers Compensation Insurance For Restaurants Carpenters Workers Compensation Insurance Is Workers Comp Expensive? How Much Is Roo?ng Workers Comp? Yes, the rumors are true—workers’ comp can get Insurance companies base workers’ expensive. Cost is the number one reason compensation premiums on a simple equation: roo?ng companies don’t buy a workers’ Payroll (times) Classi?cation Rate (times) compensation policy. Experience Mod (equals) Premium. Unfortunately, this is a fatal error for many The payroll ?gure is the estimated annual businesses. No matter the size of your payroll for your company. The classi?cation rate company, it’s best to protect your employees is a number assigned by the National Council on with adequate coverage. Compensation Insurance (NCCI). No two businesses, even in the same industry, This predetermined number represents the risk have the same insurance needs. That’s why we factor of a particular industry. offer a range of workers’ comp policies here at For example, your roo?ng workers comp class Coastal Work Comp. Our brokers will take a look code is most likely either 5551 or 5545. at your portfolio to help you select a plan that However, a gardening farm (considered a safer ticks all the right boxes for your company. industry) has a class code of only 8. The experience modi?cation rate (EMR) starts at 1 and increases each time you have an on- the-job accident. As a rule of thumb, the higher the number for each ?gure, the more your premium. And since roo?ng ranks as one of the more dangerous industries, companies tend to pay more than

“safe” industries. As you can expect, this perceived—and very real—danger means you’ll pay higher rates. How Do I Set up Workers Compensation? How Do I Save on Workers Comp Insurance? Roo?ng companies can buy a workers’ Roo?ng companies want to protect their compensation policy through either an employees, but they also want to save some insurance company or a broker. But before you money at the same time. There’s no reason buy the ?rst plan you ?nd, you need to make your company has to pay a small fortune for sure it’s the best match for your company. workers’ comp protection. Since the roo?ng industry is high-risk, many Coastal Work Comp Brokers may be the private insurance companies will quote you an right choice for your roo?ng company if exorbitant rate. They can also decide to either you ?t any of the following criteria: accept or decline your application. For this Want to lower your premiums reason, many roo?ng companies choose the Currently insured through the State Fund State Fund route. Work in a high-risk industry, such as roo?ng Regardless of your type of business, state- Facing non-renewal by your current carrier funded programs will cover you, but you’ll most Have any losses likely end up paying more than if you went the Dealing with a lapse in coverage private route. Have a high experience modi?cation rating Coastal Work Comp Brokers believes all Tired of annual audits roo?ng companies should be able to buy What you really want is an insurance company dependable and affordable workers’ comp that will be your partner at all times. plans. At Coastal Work Comp, we will be there to lead We specialize in high-risk industries, and we can you through any workers’ comp claim to help ?nd you a policy that gives you the coverage you your business avoid getting sued. You never need at a price that ?ts your budget. know when you’ll face an on-the-job accident. But if one does occur, we’ll be there to lead you through every step of the process. How Can I Reduce My Workers Comp Costs? Are you looking for an insurance policy you can afford? You need workers’ compensation insurance to protect your business and your employees, but you don’t want to break the bank buying a policy. Here at Coastal Work Comp, we can help you choose a plan that could lower your premiums by 30-40 percent! We specialize in matching high-risk industries, such as roo?ng, with cost-effective insurance plans. Our team also handles multi-state risk coverage and new ventures. Also, because you’re in roo?ng, you might be interested in:

Construction workers comp Solar workers comp Pay-as-you-go-workers comp High Modi?cation Why PEO plans are becoming more popular Even if you were non-renewed by your current carrier, facing a gap in coverage, or have a high-mod business, we have a solution. We provide a wide range of workers’ comp policies for nearly every niche industry. Our pay-as-you-go plans are affordable and will also help you avoid an audit. Whether you have a high-premium plan or a lapsed policy, now is the time to ?nd better coverage that suits your roo?ng company . When you need the best workers comp for roofers, let our team at Coastal Work Comp Brokers lend a hand. Call 1800-411-0733 for expert help in ?nding the best option for you. GET A FREE QUOTE NOW Our Services Latest News 1-800-411-0733 APRIL 27, 2023 Workers compensation for sta?ng agencies Importance of fadi@coastalworkcomp.com Trucking Workers Workers compensation for Solar About us APRIL 1, 2023 Construction workers compensation How PEOs can Help Blog Insure Sta?ng Industries Served Agencies