GST Return

Periodic reporting of GST collected and paid to the GST system is known as GST return filing. Every taxpayer needs to file GST Return as part of his statutory obligation and to keep the compliance rating and collect GST refunds. Periodic reporting differs with taxpayers, say monthly for regular taxpayers and quarterly for composition tax payers.

GST Return

E N D

Presentation Transcript

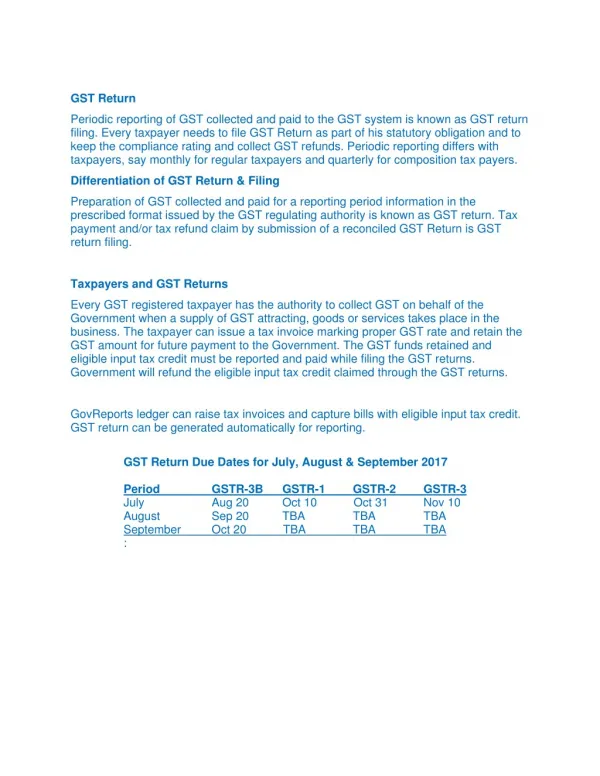

GST Return Periodic reporting of GST collected and paid to the GST system is known as GST return filing. Every taxpayer needs to file GST Return as part of his statutory obligation and to keep the compliance rating and collect GST refunds. Periodic reporting differs with taxpayers, say monthly for regular taxpayers and quarterly for composition tax payers. Differentiation of GST Return & Filing Preparation of GST collected and paid for a reporting period information in the prescribed format issued by the GST regulating authority is known as GST return. Tax payment and/or tax refund claim by submission of a reconciled GST Return is GST return filing. Taxpayers and GST Returns Every GST registered taxpayer has the authority to collect GST on behalf of the Government when a supply of GST attracting, goods or services takes place in the business. The taxpayer can issue a tax invoice marking proper GST rate and retain the GST amount for future payment to the Government. The GST funds retained and eligible input tax credit must be reported and paid while filing the GST returns. Government will refund the eligible input tax credit claimed through the GST returns. GovReports ledger can raise tax invoices and capture bills with eligible input tax credit. GST return can be generated automatically for reporting. GST Return Due Dates for July, August & September 2017 Period July August September : GSTR-3B Aug 20 Sep 20 Oct 20 TBA GSTR-1 Oct 10 Oct 31 TBA GSTR-2 GSTR-3 Nov 10 TBA TBA TBA TBA

Various types of GST Returns Taxpayer depending on the registration category, permitted to collect GST as well as claim eligible input tax credit. There are different types of GST reports for different taxpayers available as follows: FOR REGULAR TAXPAYER GST Form Description Period Due On 20th day of the following month GSTR-3B Summary details of Outward and Inward Supplies and GST Invoice level details of Outward Supplies Monthly 10th day of the following month GSTR-1 Monthly 15th day of the following month GSTR-2 Invoice level details of Inward Supplies Monthly 20th day of the following month GSTR-3 Summary details of reconciled Outward/Inward Supplies Audited GST reports for full year Monthly 31st December of the next financial year GSTR-9 Annual FOR COMPOSITION TAXPAYER GST Form Description Period Due On 18th day of the following month GSTR-4 Summary details of Outward Supplies Quarterly 31st December of the next financial year GSTR-9A Audited GST reports for full year Annual

FOR OTHER TYPE OF TAXPAYERS GST Form GSTR-5 Non Resident Foreign Taxpayer Summary details of reconciled Outward/Inward Supplies GSTR-6 Input Service Distributor Input Tax Distribution Description Period Due On 20th day of the following month Monthly 13th day of the following month Monthly 10th day of the following month GSTR-7 Tax Deductor Tax deducted at source Monthly 10th day of the following month GSTR-8 E-Commerce Operator Tax collected on supplies Monthly GSTR-10 GSTIN Cancelled/Surrendered GSTIN Cancelled/Surrendered Within 3 months of cancellation or cancellation order whichever is later 28th day of the following month GSTR-11 UIN Holder Inward supplies Monthly

Consequences of failure to file Failure to file GST return on due date will result in, Penalty of Rs.200 per day from due date up to a maximum of Rs.5,000 Interest at the rate of 18% pa on tax payable item from due date to the date of payment Rating with GSTN portal will be downgraded, which may have an impact amongst your business clients and suppliers. http://www.govreports.co.in