Download

1 / 3

0 likes | 5 Vues

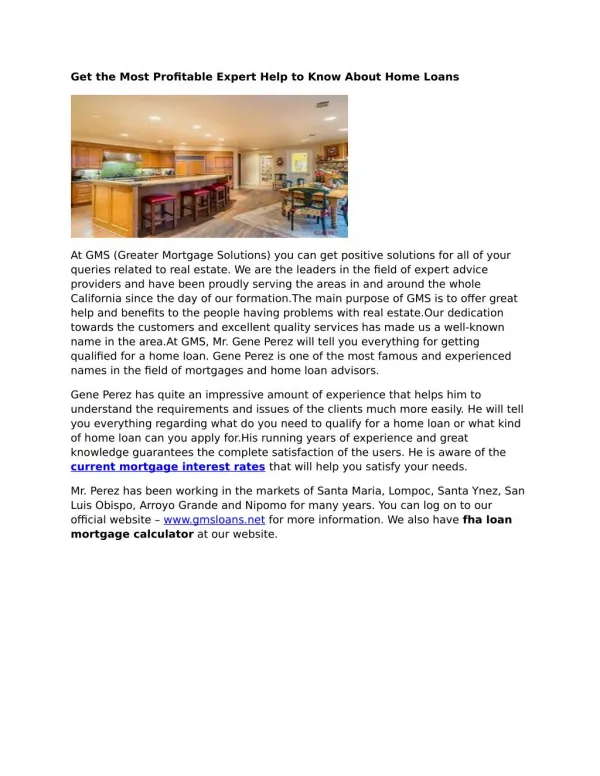

Buying a property in the UAE is an exciting yet significant financial decision. Securing a mortgage involves careful planning and understanding your financial obligations. This is where a UAE mortgage calculator becomes your invaluable guide, offering a glimpse into your monthly payments and overall loan cost. But before diving headfirst into calculations, it's crucial to understand the key factors that influence your mortgage journey and how the calculator considers them.<br>

E N D

Factors to consider when using a UAE mortgage calculator: Down payment, loan term, interest rates, and more. Buying a property in the UAE is an exciting yet significant financial decision. Securing a mortgage involves careful planning and understanding your financial obligations. This is where a UAE mortgage calculator becomes your invaluable guide, offering a glimpse into your monthly payments and overall loan cost. But before diving headfirst into calculations, it's crucial to understand the key factors that influence your mortgage journey and how the calculator considers them. 1. Down Payment: Building Your Foundation ● Minimum Requirements: In the UAE, the minimum down payment for UAE nationals is 15% and 20% for expats. This initial investment significantly impacts your loan amount and monthly payments. ● Impact on Interest Rates: A larger down payment reduces your loan amount, potentially securing a lower interest rate from lenders. Explore different down

payment scenarios using the calculator to see how it affects your interest rate and monthly payments. ● Consider Additional Costs: Remember, the down payment isn't your only expense. Factor in closing costs, registration fees, and other associated charges when planning your finances. 2. Loan Term: Stretching Out Your Repayment Journey ● Longer Terms, Lower Payments: Choosing a longer loan term (up to 25 years in the UAE) results in lower monthly payments, making them more manageable. However, this extends the repayment period, ultimately increasing the total interest paid. ● Shorter Terms, Faster Payoff: Opting for a shorter term, say 10 years, means higher monthly payments but quicker debt elimination and reduced overall interest costs. Use the UAE mortgage calculator to compare different loan terms and find the balance between affordability and faster payoff. ● Early Repayment Flexibility: Check if your mortgage allows early repayments without penalties. This flexibility can help you pay off your loan faster and save on interest, even with a longer loan term. 3. Interest Rates: The Cost of Borrowing ● Fixed vs. Variable Rates: UAE mortgages typically offer fixed or variable interest rates. Fixed rates provide stability, while variable rates can fluctuate based on market conditions. The calculator allows you to compare both options and see how changes in interest rates affect your payments. ● Negotiation Power: Your credit score, employment status, and salary can influence your eligibility for lower interest rates. Shop around and negotiate with different lenders to secure the best possible rate. ● Promotional Offers: Some lenders offer promotional interest rates for a limited period. While attractive, factor in the long-term implications of the rate reverting to a higher level after the promotion ends.

4. Beyond the Basics: Additional Factors to Consider ● Salary and Debt-to-Income Ratio: Lenders assess your affordability based on your income and existing debts. The UAE Central Bank sets a maximum debt-to-income ratio of 50%, ensuring your monthly payments remain manageable. ● Property Location and Type: Property prices vary significantly across different emirates and even within the same city. The calculator allows you to adjust the property value based on your chosen location and type (apartment, villa, etc.). ● Additional Fees and Insurance: Factor in homeowners' insurance, property service charges, and other recurring expenses when using the calculator. These add to your monthly outgoings and impact your overall budget. 5. Using the UAE Mortgage Calculator Effectively ● Accuracy of Information: The calculator's accuracy depends on the information you provide. Ensure you enter accurate details about your income, expenses, and desired loan terms. ● Multiple Scenarios: Don't limit yourself to one calculation. Play around with different down payments, loan terms, and interest rates to see how they impact your monthly payments and overall costs. ● Seek Professional Advice: While the calculator is a valuable tool, it cannot replace personalized financial advice. Consult a mortgage broker or financial advisor to discuss your specific situation and explore tailored options. Conclusion: A UAE mortgage broker is your gateway to understanding the financial implications of buying a property. By carefully considering the factors discussed above, you can use it to make informed decisions, compare options, and ultimately choose the mortgage that best suits your financial goals and aspirations. Remember, the calculator is a tool, but your financial journey requires careful planning and a personalized approach.