Things to Consider Before Buying a Home

140 likes | 441 Vues

Read Haylen Group buying a house checklist, which includes important factors to considered before buying a home.

Things to Consider Before Buying a Home

E N D

Presentation Transcript

Things to Consider Before Buying a Home Haylen Group Inc. http://www.haylengroup.com/

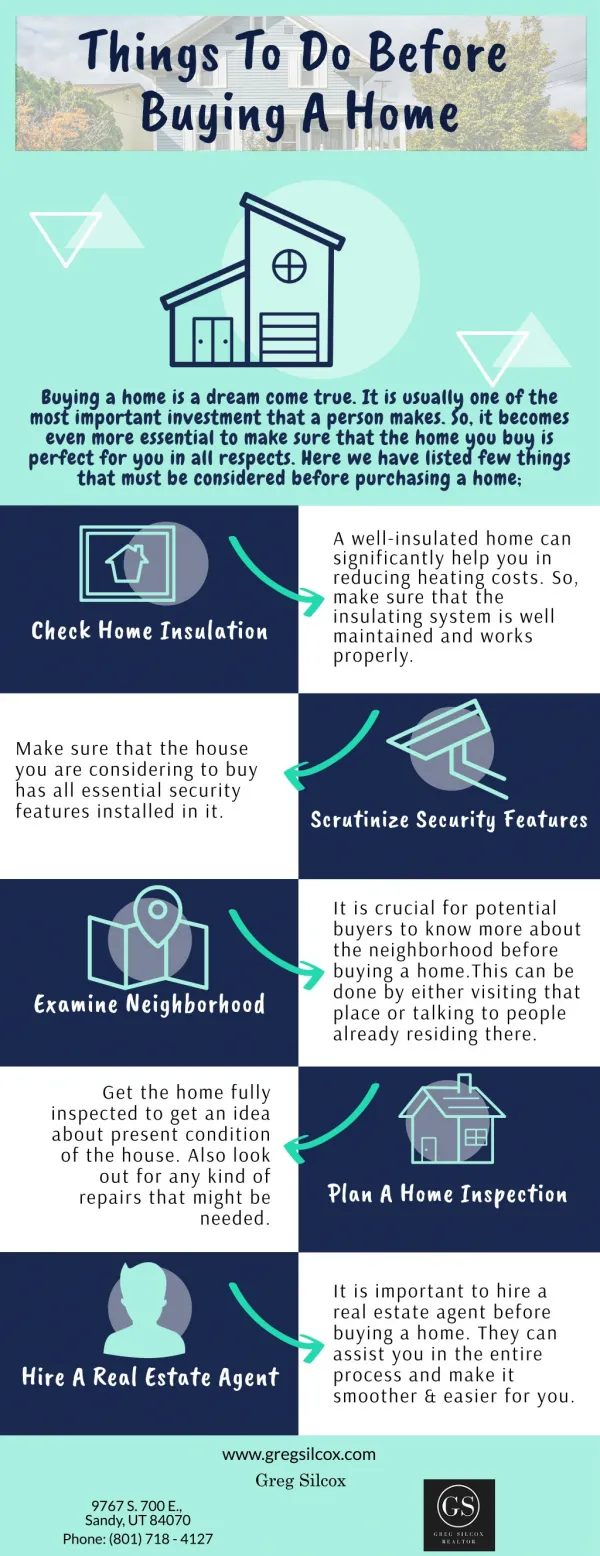

Decide Whether Buying a Home Is Worth • Although it’s more than just a matter of dollars and cents, right now, in most major cities, buying a home is 35% cheaper than renting. There’s no right or wrong answer for everyone, though—home buying comes with a number of benefits (and headaches), but so does renting—so you’ll have to weigh the pros and cons for yourself.

Figure out what you can afford • Buying a house will have a significant impact on your finances, so make sure you can handle it. • Housing is more affordable than ever and incentives like low interest rates and the new expanded tax credit are enticing buyers to enter the market. But purchasing property involves a lot of upfront costs: closing costs, down payment, new furniture, moving expenses. Do you have enough cash?

How much you can spend on a monthly basis? • Your monthly payment will consist of PITI: principal and interest (determined by the home’s purchase price and your interest rate), property taxes and home insurance. Your monthly homeownership budget should also include utilities, cable/TV/Internet and general maintenance costs. • When buying a condo or townhome, factor in the homeowners association fees and any special assessments.

Schedule a home inspection • Your purchase offer should include a home inspection so you know what repairs must be made and about how they will cost. You may or may not be able to negotiate for the seller to pay for home improvements, but it’s always better to go into a house with full knowledge of its condition.

Search for neighborhood information online. • If you already live in the community, you may be able to skip this step, but it’s always worthwhile to search local newspaper websites, local government sites, community sites and blogs to find out what’s happening in terms of upcoming development or other issues.

Check the Crime Report • Your local police station will have statistics on crime and you can also go to www[dot]crimereports[dot]com to find information according to a particular address or ZIP code.

Juggle Difficult Buying Situations • Buying and selling a home at the same time can be tricky. You have two options: focus on selling first or on buying first. Here are the pros and cons of each method. If you’re self-employed, qualifying for a mortgage requires more work than if you’re an employee. Make sure you have your paperwork in order.

Talk to the sellers • If the sellers are willing to share information with you, they’re the best resource of all to learn about the community and the house. You can ask the sellers about renovations they’ve done and even talk to them about whether your plans for the house are possible.

Negotiate as much as you can • You can use an agent to do the negotiating for you, but you can't be sure how hard they will push for you. As a buyer, you should feel in control and as though you have nothing to lose through robust negotiation.

Finding the Right Mortgage • After you have determined how much home you can afford, it is time to shop for the right mortgage. Since you are likely to be financing a loan for hundreds of thousands of dollars, it is crucial that you make a smart decision. A bad mortgage can significantly affect your finances over time. • The good news is that there is a type of mortgage available for almost every situation. The bad news is that choosing the wrong one can cost you tens of thousands of dollars in interest over the term of the loan. The most common loans come in two styles: fixed and adjustable interest rate loans.

The Down Payment • Although it’s possible to buy a home without a down payment, you’ll get a better rate, smaller mortgage payments, and be able to qualify for more loans if you can put 20% down. Start saving for the down payment as soon as you are thinking about buying a home. And don’t forget you’ll have hefty closing costs to save up for and cover as well. • When you are unable to put twenty percent down, the lender generally requires that you also pay the PMI premium, which can be anywhere from twenty dollars to a few hundred dollars each month. When shopping for a mortgage, take this into consideration and ask if there are alternatives to paying PMI if you will be unable to come up with the full down payment.

Contact US • Haylen Group Inc. • Silicon Valley (Santana Row Location) • 560 S Winchester Blvd • Suite 500, San Jose, • CA 95128 • http://www.haylengroup.com/