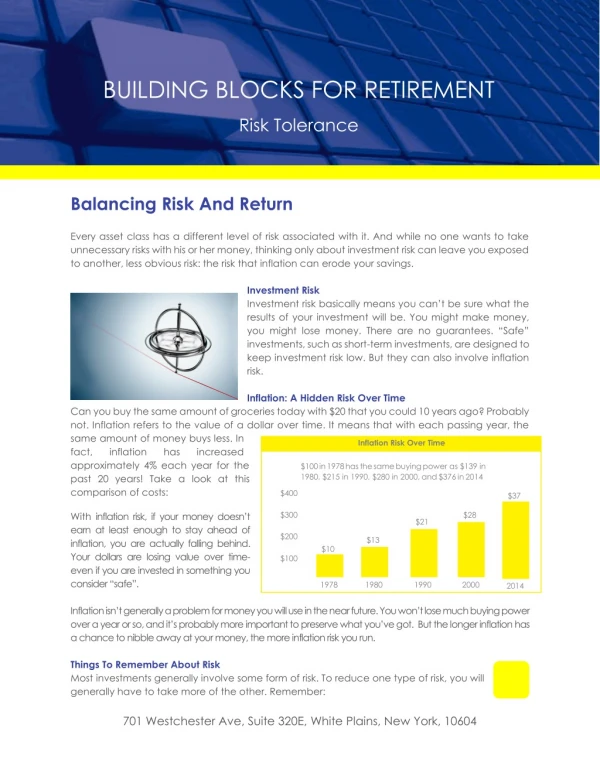

Balancing SOX with Risk Based Audit Planning

320 likes | 828 Vues

Balancing SOX with Risk Based Audit Planning. The Institute of Internal Auditors March 9, 2004. Dave Richards, CIA, CPA Director, Internal Auditing FirstEnergy Corporation. Balancing SOX with Risk Based Audit Planning. Introduction & Overview Dave Richards, FirstEnergy

Balancing SOX with Risk Based Audit Planning

E N D

Presentation Transcript

Balancing SOX with Risk Based Audit Planning The Institute of Internal AuditorsMarch 9, 2004 Dave Richards, CIA, CPADirector, Internal AuditingFirstEnergy Corporation

Balancing SOX with Risk Based Audit Planning • Introduction & Overview • Dave Richards, FirstEnergy • Finding the Balance • Brian Appleton, National Penn Bancshares • Year 2 Audit Planning • Carl Balderson, Pinnacle West Capital • Balancing Issues for Large Shops • Peg Weir, United States Postal Service • Break • Q & A

Key Balancing Issues 1. Involvement in SOX 404 Work 2. Expectations of AC & Sr. Mgt 3. Risk Model Impacts 4. Emphasis on Financial Audits 5. Increased IT General Controls Topics 6. Using 404 Results to Drive Audits 7. Dealing with SOX Issues 8. Impact on External Auditor Relationship & Work Support

Key Balancing Issues 9. Using 404 Model for Operational & Compliance Topics 10. Staff Productivity Enhancements 11. IAD Tools for Control Assessments 12. Rotation of Audit Topics??? 13. Building on SOX 404 Work 14. IAD Customer Relationships 15. Impact on Audit Contingency 16. Internal Control Opinions in Audits

Finding the Balance Brian T. Appleton, CIA, MBA,CDP Executive Vice President Director of Internal Audit National Penn Bancshares

Overview of Company • Company Size • Audit Division • Client Focused Philosophy • Process Owner Class

Status of 404 • Tone at the top • How 404 is implemented makes a difference • High level risk-assessment completed • Documentation phase in progress

Balance • Identify the coordinating scheme • Complement, not supplement • Be flexible and creative • Focus your scope • Standardize the documentation • Take a closer look at opportunities • Management • Audit

Impact on Internal Clients • Creates a more sophisticated clientele • Fosters uniformity in structure • Increases accountability for results • Promotes process ownership by management

Impact on Audit Approach • Enhance auditor knowledge • Career growth opportunity • Role of auditors as facilitators • Expansion of skill set to educator • Springboard effect • Operational and compliance audits • Control Self Assessment • Enterprise Risk Management

Benefit to Audit Committee • Stronger assurance of controls • Create new metrics • Published accountability through sign-offs

Summary • Identify the changes, find a balance • Allocate resources early • Sell the benefit to the company • Find and publish the positives • Think of SOX 404 as complementing audit coverage

Year 2 Audit Planning Carl Balderson, CIA, CPA, CFEDirector of Audit Services Pinnacle West Capital Corporation

Re-balancing is continued evolution Changed audit committee expectations Changed management expectations Driving Change

Increase management awareness of internal controls Audit customer responsiveness Greater emphasis on IT auditing Verify quarterly review for IC changes Impacts of SOX

Risk based planning with pre-SOX methodology What we Think is needed for SOX Follow-up open issues Test changed process documentation Test Key controls Integrate to avoid duplication Alternate depth of efforts with future years Allocate available resources Planning Steps

Automated Work Papers Productive Time Targets Emphasize Project Budgets In-house and Local Training Productivity Initiatives

Small number of hours unallocated Renewed emphasis on “Stop & Go” auditing Administrative assistant/secretary vs. para-professional auditor Be more selective in what we address Contingency Planning

Integrate SOX compliance and risk management processes Examine risk management processes for efficiency Documentation of new systems Integrate SOX documentation with business resumption plans Utilize documentation for training Driving Long-Term Value

Balancing Issues for Large Shops Margaret (Peg) Weir Manager, Internal Control Group United States Postal Service

Independent government entity Self-sustaining Annual operating revenue +/- $70B Second largest civilian employer 38,000 Post Offices Office of Inspector General United States Postal Service

Internal Control Group • CFO vision • Established ICG organization • Complements OIG function • “End-to-end” process • Looks for efficiencies and risks of inefficiencies

Internal Audit-Internal Control“Policy vs. Process” • Internal Audit - Financial Statements fairly represent operations • Monies • Expenses • Work hours • Assets • Internal Control - Reasonable Assurance – achievement of fundamental business goals • Reliability • Exist, effective, efficient • Compliance with laws/regulations

Internal Control Group • Identify risk through data and process analysis • Partner with process owner to mitigate prioritized risk • Analyze trends and indicators • Conduct internal control reviews • Develop improved controls to meet goals and objectives

Sarbanes-Oxley Act • Voluntarily adopting parts of Section 404 • Makes good business sense

Internal Control Group • Senior management provides direction and oversight • Focus based on: • Guidance • Risk analysis • Risk prioritization • Resources support mandate

Internal Control Group • Enterprise-wide from corporate to local • Interdependencies vs. stovepipes • Partnership with process owners • Data driven • Targeted reviews • Standardized approach using COSO framework • Root causes • Meaningful recommendations to improve controls • Reasonable assurance goals & objectives will be met

Internal Control Group Status • Implemented preliminary activities of COSO framework • Adjusted as lessons learned • Developing additional training • Enhancing the analytical & reporting tool

Internal Control Group • Internal Control Group complements internal audit process • Internal Control Group supports performance-based culture • Internal Control Group establishes foundation for long-term enterprise-wide improvements and efficiencies • Internal Control Group is dynamic & evolving

Conclusions • SOX 404 WILL IMPACT what we do • What impact it has must be managed • Upfront drivers for impact must be understood • Changes in approach, scope, & results expectations must be communicated • AC, Sr. Mgt. & IAD Customers must recognize the impact on identifying & performing work • IAD must be more productive to meet this challenge • External Auditor relationship must be managed

Next Webcast April 13, 2004 “Strategies for Internal & External Relationships” See you at our next webcast!