Download

1 / 5

0 likes | 1 Vues

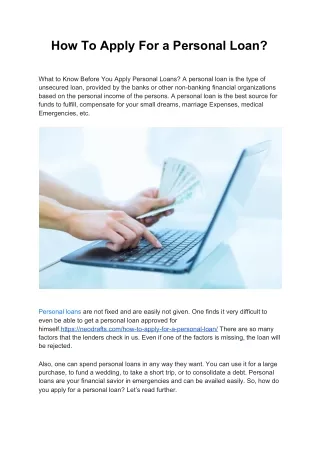

Understanding the difference between a personal loan and a personal line of credit is essential when deciding how to borrow money. A personal loan provides a one-time lump sum of money that you repay in fixed monthly installments over a set period, usually with a fixed interest rate. Itu2019s ideal for specific expenses like medical bills, home renovations, or consolidating debt.<br><br>In contrast, a personal line of credit offers a flexible borrowing option. You get access to a revolving credit limit, and you only pay interest on the amount you use. Once you repay the borrowed funds, the credit become

E N D

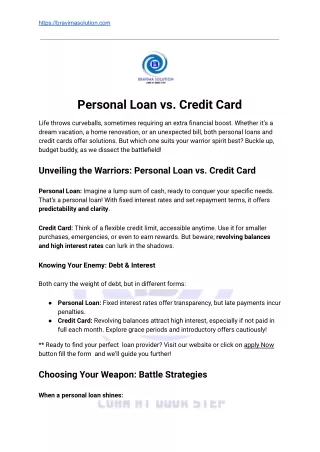

When it comes to borrowing money, two of the most common options are personal loans and personal lines of credit. Both are unsecured forms of borrowing, meaning they don't require collateral, and both can help you cover a wide range of expenses from home improvements to medical bills, emergency repairs, or even a vacation. However, the way they work is quite different, and choosing the right one depends on your specific financial situation and goals. What Is a Personal Loan? A personal loan is a lump sum of money you borrow from a bank, credit union, or online lender and repay in fixed monthly installments over a set period, usually between one and seven years. These loans often come with fixed interest rates, which means your monthly payments will remain the same throughout the life of the loan. Key Features of a Personal Loan: ● Lump sum disbursed upfront ● Fixed repayment term ● Fixed or variable interest rate ● Monthly payments are consistent ● Ideal for one-time expenses Common Uses: ● Debt consolidation

● Home renovations ● Medical expenses ● Large purchases ● Wedding or travel costs What Is a Personal Line of Credit? A personal line of credit, on the other hand, works more like a credit card. You're approved for a maximum credit limit and can borrow from it as needed. You only pay interest on the amount you actually use, not the full limit. Once you repay the borrowed amount, those funds become available again. This makes a line of credit revolving, meaning you can continue to use it as long as the account remains open and in good standing. Key Features of a Personal Line of Credit: ● Flexible access to funds ● Only pay interest on what you borrow ● Credit becomes available again once repaid ● May have variable interest rates ● Minimum monthly payments based on usage Common Uses: ● Emergency expenses ● Irregular income or cash flow management ● Home maintenance over time ● Medical treatments with unpredictable costs Personal Loan vs. Personal Line of Credit: Key Differences

Personal Line of Credit Feature Personal Loan Borrow as needed, up to a limit Disbursement Lump sum upfront Flexible payments, based on usage Repayment Fixed monthly payments Interest Fixed or variable Usually variable Best for one-time, planned expenses Best for ongoing or unexpected needs Use of Funds Revolving credit; funds replenish Credit Reuse One-time loan Based on credit score, income, DTI Similar criteria, sometimes stricter Approval Criteria Structured debt repayment Flexible, on-demand access to funds Best For Pros and Cons Personal Loan Pros: ● Predictable payments make budgeting easier ● Often lower interest rates than credit cards ● Helpful for consolidating high-interest debt ● Clear payoff date Personal Loan Cons: ● Less flexible if you need more funds later ● Interest starts accruing on the full amount immediately ● Prepayment penalties may apply Personal Line of Credit Pros:

● Flexibility to borrow only what you need ● Pay interest only on what you use ● Can be used multiple times without reapplying Personal Line of Credit Cons: ● Variable interest rates can increase over time ● Harder to budget due to inconsistent payments ● Temptation to overspend due to ongoing access Which Should You Choose? Choose a Personal Loan if: ● You know exactly how much money you need ● You prefer fixed payments and a clear payoff schedule ● You’re consolidating debt or financing a one-time purchase Choose a Personal Line of Credit if: ● You need access to funds over time ● You want flexibility to borrow as needed ● You have unpredictable or variable expenses For example, if you’re planning a kitchen renovation and have received a quote of $10,000, a personal loan makes sense. You get the funds upfront and repay in predictable monthly installments. However, if you’re managing a business with irregular cash flow or facing potential medical treatments with unclear costs, a personal line of credit can offer the flexibility you need without committing to a large debt all at once. Credit and Qualification

Both products are typically unsecured, so lenders will rely heavily on your credit score, income, and debt-to-income (DTI) ratio to determine your eligibility and interest rate. A higher credit score will improve your chances of getting approved and may help secure lower interest rates. Conclusion Understanding the difference between a personal loan vs personal line of credit is crucial when planning your finances. A personal loan provides structure and is ideal for planned expenses or debt consolidation, while a personal line of credit offers flexibility for ongoing or emergency costs. Before choosing, consider your borrowing needs, repayment preferences, and overall financial situation. Comparing terms, fees, and interest rates from multiple lenders can help you find the most cost-effective and convenient option for your goals. Whether you're looking for predictability or flexibility, knowing the pros and cons of each option puts you in control of your financial future. For more information visit our website :- https://lendingpalm.com/personal-loan-vs-personal-line-of-credit/