Download

1 / 1

E N D

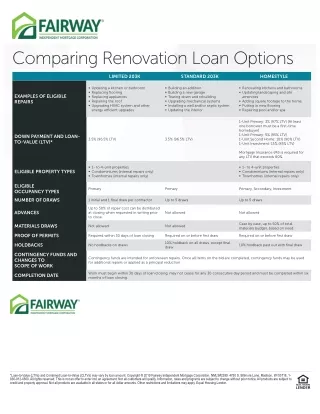

Comparing Renovation Loan Options LIMITED 203K STANDARD 203K HOMESTYLE • Updating a kitchen or bathroom • Replacing fl ooring • Replacing appliances • Repairing the roof • Upgrading HVAC system and other energy ef cient upgrades • Building an addition • Building a new garage • Tearing down and rebuilding • Upgrading mechanical systems • Installing a well and/or septic system • Updating the interior • Renovating kitchens and bathrooms • Updating landscaping and site amenities • Adding square footage to the home • Putting in new fl ooring • Repairing pool and/or spa EXAMPLES OF ELIGIBLE REPAIRS 1-Unit Primary: 3% (97% LTV) [At least one borrower must be a fi rst-time homebuyer] 1-Unit Primary: 5% (95% LTV) 1-Unit Second Home: 10% (90% LTV) 1-Unit Investment: 15% (85% LTV) DOWN PAYMENT AND LOAN- TO-VALUE (LTV)* 3.5% (96.5% LTV) 3.5% (96.5% LTV) Mortgage Insurance (MI) is required for any LTV that exceeds 80%. • 1- to 4-unit properties • Condominiums (internal repairs only) • Townhomes (internal repairs only) • 1- to 4-unit properties • Condominiums (internal repairs only) • Townhomes (internal repairs only) ELIGIBLE PROPERTY TYPES ELIGIBLE OCCUPANCY TYPES Primary Primary Primary, Secondary, Investment NUMBER OF DRAWS 1 initial and 1 fi nal draw per contractor Up to 5 draws Up to 5 draws Up to 50% of repair cost can be distributed at closing when requested in writing prior to close. ADVANCES Not allowed Not allowed Case by case, up to 50% of total materials budget, based on need MATERIALS DRAWS Not allowed Not allowed PROOF OF PERMITS Required within 30 days of loan closing Required on or before fi rst draw Required on or before fi rst draw 10% holdback on all draws, except fi nal draw HOLDBACKS No holdbacks on draws 10% holdback paid out with fi nal draw CONTINGENCY FUNDS AND CHANGES TO SCOPE OF WORK Contingency funds are intended for unforeseen repairs. Once all items on the bid are completed, contingency funds may be used for additional repairs or applied as a principal reduction. Work must begin within 30 days of loan closing, may not cease for any 30 consecutive day period and must be completed within six months of loan closing. COMPLETION DATE L * 8 V - o t - n a 4 - 2 1 9 - 6 6 a t i d e r c o a ) s V e v r e s e r s t h g i r l l A . 0 0 N . l a v o r p p a y t r e p o r p d u l a 8 T L ( e n C d o n i b m T . d o r p l l a t o e L d n s i s i h o V - o t - n a a t o a l i a v a e r a s t c u d u l a e o t r e f f o n C ( e T L o l y b y r a v y a m a n a o t n i r e t n d l l a r o f r o s e t a t s l l a n i e l b ) s V a C . t n u o t s u c l l a t o N . t n e a r a l l o a n m o g i r y p o 2 © t h q l l i w s r e m o i t c i r t s e r r e h t O . s t n u 0 1 F 9 w r i a r o f n I . y f i l a u n I y a e a s e t a r , n o i t a m o i t a t i m i l d n d e p n d t n e g t r o M n a y a m s n a C e a r g E . y l p p g p r o m o i t a r o u s e r a s q N . n h c o t t c e j b L g n i s u o H l a u M L S # 2 4 . 9 8 g n a . r e d 2 7 5 t l i B . S 0 L e r o m o r p l l A . e c i t o n r o i r p t u o a , e n M o s i d a u s e r a s t c u d , n W 5 I 3 - 1 , 8 1 o t t c e j b 7 e r g e m o r p d h t i w e n m o a s n e n