Download

1 / 3

0 likes | 4 Vues

In the UK, retirement at 66 with a life expectancy of 78.8 for men and 82.7 for women highlights the importance of early retirement planning. Pension funds may fall short due to living costs, prompting consideration of property portfolios. House Manage offers guidance on building such portfolios as an alternative to traditional pensions. UK pension statistics reveal a retirement period of 20-30 years, recommending saving at least 10 times one's annual salary. With a median savings gender gap, only 65% have workplace pensions. Property investment, aided by a property management company like Hou

E N D

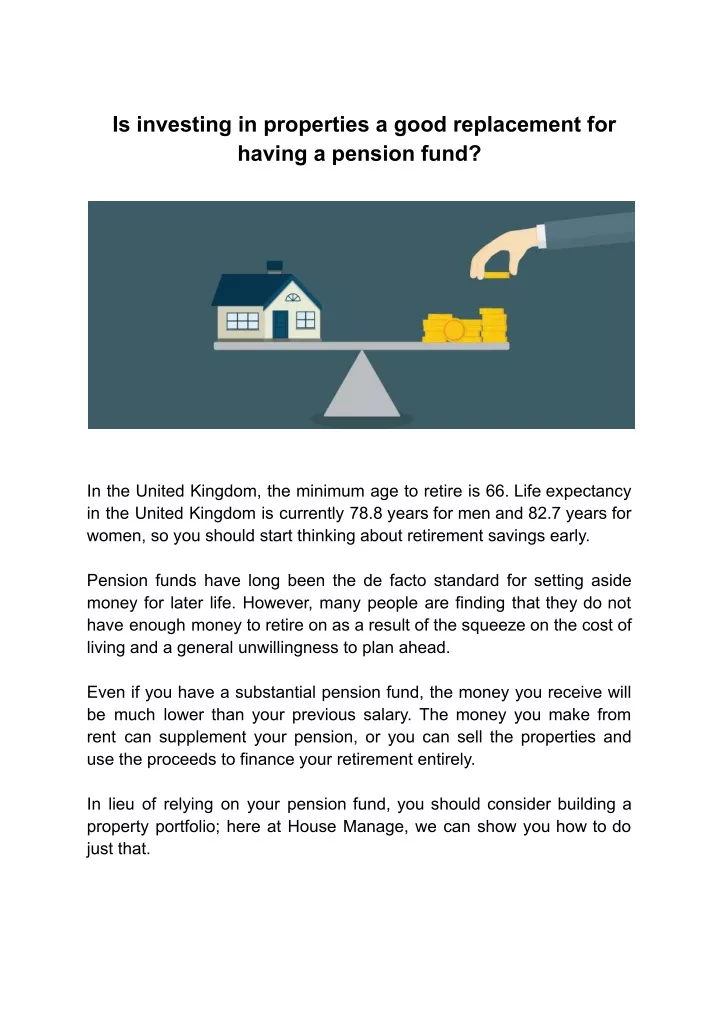

Is investing in properties a good replacement for having a pension fund? In the United Kingdom, the minimum age to retire is 66. Life expectancy in the United Kingdom is currently 78.8 years for men and 82.7 years for women, so you should start thinking about retirement savings early. Pension funds have long been the de facto standard for setting aside money for later life. However, many people are finding that they do not have enough money to retire on as a result of the squeeze on the cost of living and a general unwillingness to plan ahead. Even if you have a substantial pension fund, the money you receive will be much lower than your previous salary. The money you make from rent can supplement your pension, or you can sell the properties and use the proceeds to finance your retirement entirely. In lieu of relying on your pension fund, you should consider building a property portfolio; here at House Manage, we can show you how to do just that.

UK Pension Statistics Between twenty and thirty years is the typical retirement period. Financial advisors advise putting away at least 10 times your annual salary for retirement. The median savings for men age 50 is £112,000, while the median savings for women is only £56,000. Only about two-thirds of Brits (65%) have a workplace pension. Can I Get By With My Pension? When it comes to retirement income, no two people will have the same requirements. Expenses to think about include rent or mortgage payments, utilities, repairs, vacations, gifts for grandchildren, and end-of-life care. There is a lot to consider, and many people arrive at the conclusion that their savings won't be enough to maintain their current standard of living. The first thing to do is to calculate how much money you can expect to have in your various pension plans by the time you retire. If you've had several pension schemes over your career, you may not be fully aware of your financial position. Since you still have time to act, now is the time to get clarity by consulting a pension or financial advisor. You can buy a property to get monthly rent. For this, you can hire a property management company. Developing A Property Portfolio As Opposed To A Pension Fund Pupils would have ideally commenced contributing to their pension at the age of 18, as advised by pension specialists, who suggest allocating 12% of their monthly salary to the pension pot.

Yet, despite the fact that employers are obligated to contribute to a workplace pension if employees do the same and the pension itself provides tax advantages, a mere 65% of the population in the United Kingdom possesses one. The existing full state pension for eligible individuals (i.e., those without gaps in their national insurance records) is worth £179.60 per week. In the absence of a workplace pension, one may find themselves financially precarious during retirement. Nevertheless, if you are able to save enough money to cover a house deposit (10% of the total value if you are an existing homeowner), property investment could be among your most lucrative options. Hire a property manager who can help you with the management process. The available alternatives consist of purchasing a property in retirement and either renovating it to generate a healthy return on your investment or becoming a buy-to-let landlord with the intention of selling the property in retirement, or investing in property while you are still young. Developing Astute Real Estate Investments Investing in real estate with the intention of financing one's retirement is predicated on the property generating a steady income. This may be accomplished through monthly rental payments that offset the mortgage balance, or through the proceeds generated from the sale of the property. All of this is feasible but requires thorough research, particularly with regard to the financial investment required to achieve the highest possible return. House Manage is the best property management company who can look after your property and also provide necessary guidance. Resources Link:- https://shorturl.at/mpy26