Download

1 / 9

90 likes | 202 Vues

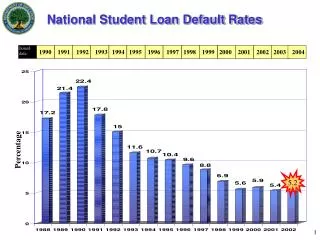

According to the New York Federal Reserve, nearly 10 years out of college the 2005 cohort of study loan borrowers has paid down only 38 percent of its original student debt. Those are numbers that could impact us all if they stunt our economic recovery.

E N D

High Balance Study Loan Borrowers Skirt Default, Still Struggle

It’s true that borrowers with less student debt actually default in higher numbers. Borrowers who drop out of college rack up less debt because they’re not in school for as long. • Without a degree or certificate, these borrowers are less likely to earn the income needed to retire the debt and, therefore, are at a higher risk for default. • The Federal Reserve numbers show that more than 30 percent of borrowers who left school in 2009 owing less than $5,000 in student loans experienced a default. • On the other hand, that same study shows only about 15 to 20 percent of the high-balance borrowers of the 2009 cohort have defaulted.

In fact, according to the Federal Reserve, "borrowers who start out owing more than $50,000 are at risk for bad outcomes almost to the same extent as small-balance borrowers owing less than $5,000." • That’s because default, which doesn’t officially occur for federal student loans until 270 days of nonpayment, isn’t the only bad outcome.

That’s not always a worst-case scenario for the borrower. • More and more high-balance borrowers are beginning to take advantage of income-based repayment programs that require only small payments tied to income and forgive any outstanding balance after 10, 20 or 25 years. • Taking advantage of income-based repayment plans can help borrowers more effectively balance education debt payments with other financial priorities. • It’s definitely better than letting student loans slip into delinquency and default. But it can also mean holding an increasing load of debt on your credit record, which could diminish your chances of securing other types of credit.

The use of deferments and forbearances to postpone payment of a federal student Deferments and forbearances can be lifelines to borrowers facing imminent– the process whereby accrued interest is added to the principal balance and interest is then charged on the new larger balance.

According to the New York Federal Reserve, nearly 10 years out of college the 2005 cohort of study loan borrowers has paid down only 38 percent of its original student debt. • Those are numbers that could impact us all if they stunt our economic recovery. • Source: (http://bit.ly/1keq4W1)

Follow us on https://www.facebook.com/AvanseEducationLoan https://www.linkedin.com/company/avanse-financial-services https://twitter.com/avanseeduloan https://plus.google.com/+AvanseFinancialServicesLtdMumbai https://www.youtube.com/channel/UCcsuUx1EH1C08XmX2embpug

Read more on Education Loans : http://www.avanse.com/avanse-education-loans/ • Thank You..!!!