What is financial statement preparation

0 likes | 12 Vues

Preparing financial statements is perhaps one of the most important steps of the accounting cycle. These statements represent the end purpose of the financial reporting and the accounting system.<br>Preparing financial statements can be a simple or a very sophisticated process based on the company size and its requirements. Some financial statements might need footnotes and disclosures as well. Financial statements are prepared using the individual account balances listed in the adjusted trial balance in the preceding step.<br>

What is financial statement preparation

E N D

Presentation Transcript

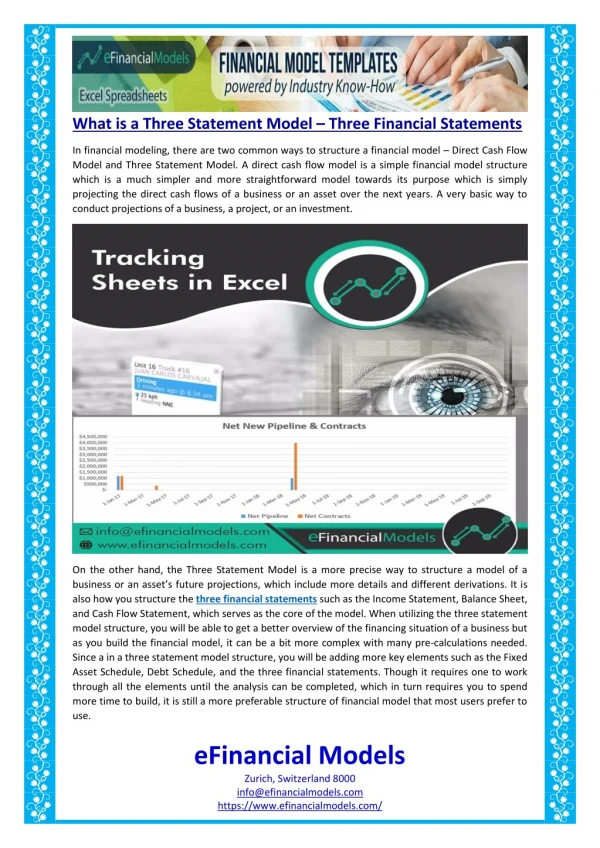

Preparing financial statements is perhaps one of the most important steps of the accounting cycle. These statements represent the end purpose of the financial reporting and the accounting system. Preparing financial statements can be a simple or a very sophisticated process based on the company size and its requirements. Some financial statements might need footnotes and disclosures as well. Financial statements are prepared using the individual account balances listed in the adjusted trial balance in the preceding step. The three financial statements are: 1. Income statement 2. Balance sheet 3. Cash flow statement (statement of cash flows) The Income Statement The income statement will show the company’s performance for each period. It will start with sales revenue and then deduct the cost of goods sold from it to arrive at the gross

profit. After that, the operating expenses are deducted to arrive at the “bottom line” – net profit. Key features ● Topline includes the net sales (sales revenues minus returns by customers) ● Operating costs include cost of goods sold (beginning inventory plus purchases minus closing inventory) ● Accounting principles of matching and accrual accounting used ● Operating expenses for the year could include rent expense, insurance, utility expense, etc. ● Net profit shows the bottom line of the business ● Income statement can be used to assess the profitability The Balance Sheet The balance sheet reflects the financial position of the company at a given point in time. It includes assets, liabilities and equity. The accounting equation comes into play here again as assets should equal liabilities plus equity. The balance sheet begins with the assets section which would include both fixed assets and the current assets of a company. Net fixed assets can be calculated by subtracting the accumulated depreciation expense from the gross fixed assets. The current assets are all those items that are either cash or can be converted to cash within one year. These include cash and cash equivalents, Accounts Receivable Processing in New York , inventory, prepayments, etc. The liabilities section of the balance sheet will include both current liabilities and non-current liabilities. Current liabilities are those obligations that must be repaid within one year and can include accounts payable, current portion of long-term debt, accrued expense, bank overdraft, current lease payable etc. The long-term liabilities are obligations that go beyond one year and include bonds payable, long-term loans, capital leases, pension liabilities, etc. The equity side of the balance shows the position of capital raised by the shareholders. It should, therefore, be equal to assets minus liabilities. The equity side of the balance

sheet would include components like commons stock, preferred stock, additional paid-in capital, retained earnings, treasury stock, etc. Key features ● Shows the financial position of a company ● Snapshot at a given time in point ● Consists of three section – assets, liabilities and equity ● Can be used for purposes of various ratio analysis The Cash Flow Statement The cash flow statement is sometimes very important in running the operational day to day of a business. This statement will give a fair idea of how much cash has been generated by the company from operations and if that cash has been used in financing or any investing activities. The cash flow statement is prepared by taking the net income figure from the income statement and adjusting it for all non-cash expenses such as depreciation. Changes in working capital are also adjusted to arrive at net cash flow from operations. Then follows the sections related to investing activities such as investment in a new property, plant or equipment. After that, the financing section includes components such as the issuance of new common stock, repayment of debt, issuance of debt etc. Key features ● Shows changes in overall cash levels of a company ● Follows the cash accounting principle ● Consists of three segments – cash flow from operations, cash flow from investing activities and cash flow from financing activities ● Expressed for a given time period

How to Prepare Financial Statements The preparation of Financial Statement Preparation in Chicago involves the process of aggregating accounting information into a standardized set of financials. The completed financial statements are then distributed to management, lenders, creditors, and investors, who use them to evaluate the performance, liquidity, and cash flows of a business. The preparation of financial statements includes the following steps (the exact order may vary by company). Step 1: Verify Receipt of Supplier Invoices Compare the receiving log to accounts payable to ensure that all supplier invoices have been received. Accrue the expense for any invoices that have not been received. Step 2: Verify Issuance of Customer Invoices Compare the shipping log to accounts receivable to ensure that all customer invoices have been issued. Issue any invoices that have not yet been prepared. Step 3: Accrue Unpaid Wages Accrue an expense for any wages earned but not yet paid as of the end of the reporting period . Step 4: Calculate Depreciation Calculate depreciation expense and amortization expense for all fixed assets in the accounting records. Step 5: Value Inventory

Conduct an ending physical inventory count, or use an alternative method to estimate the ending inventory balance. Use this information to derive the cost of goods sold, and record the amount in the accounting records. Step 6: Reconcile Bank Accounts Conduct a bank reconciliation, and create journal entries to record all adjustments required to match the accounting records to the bank statement. Step 7: Post Account Balances Post all subsidiary ledger balances to the general ledger. Step 8: Review Accounts Review the balance sheet accounts, and use journal entries to adjust account balances to match the supporting detail. Step 9: Review Financials Print a preliminary version of the financial statements and review them for errors. There will likely be several errors, so create journal entries to correct them, and print the financial statements again. Repeat until all errors have been corrected. Step 10: Accrue Income Taxes Accrue an income tax expense, based on the corrected income statement. Step 11: Close Accounts Close all subsidiary ledgers for the period, and open them for the following reporting period.

Step I2: Issue Financial Statements Print a final version of the Financial Accounting Services in New York . Based on this information, write footnotes to accompany the statements. Finally, prepare a cover letter that explains key points in the financial statements. Then assemble this information into packets and distribute them to the standard list of recipients. Additional reading : Tax Consulting Agency in New York .